As expected on this blog, existing home sales declined more in February than the consensus forecast.

Going forward, there are some economic reasons for some softness in existing home sales in certain areas. Low inventory is probably holding down sales in many areas, and there will be weakness in some oil producing areas (see: Houston has a problem).

It is important to remember that new home sales are more important for jobs and the economy than existing home sales. Since existing sales are existing stock, the only direct contribution to GDP is the broker’s commission. There is usually some additional spending with an existing home purchase – new furniture, etc – but overall the economic impact is small compared to a new home sale. So some slowing for existing home sales is not a big deal for the economy.

Earlier: Existing Home Sales decreased in February to 5.08 million SAAR

I expected some increase in inventory last year, but that didn’t happened. Inventory is still very low and falling year-over-year (down 1.1% year-over-year in February). More inventory would probably mean smaller price increases and slightly higher sales, and less inventory means lower sales and somewhat larger price increases.

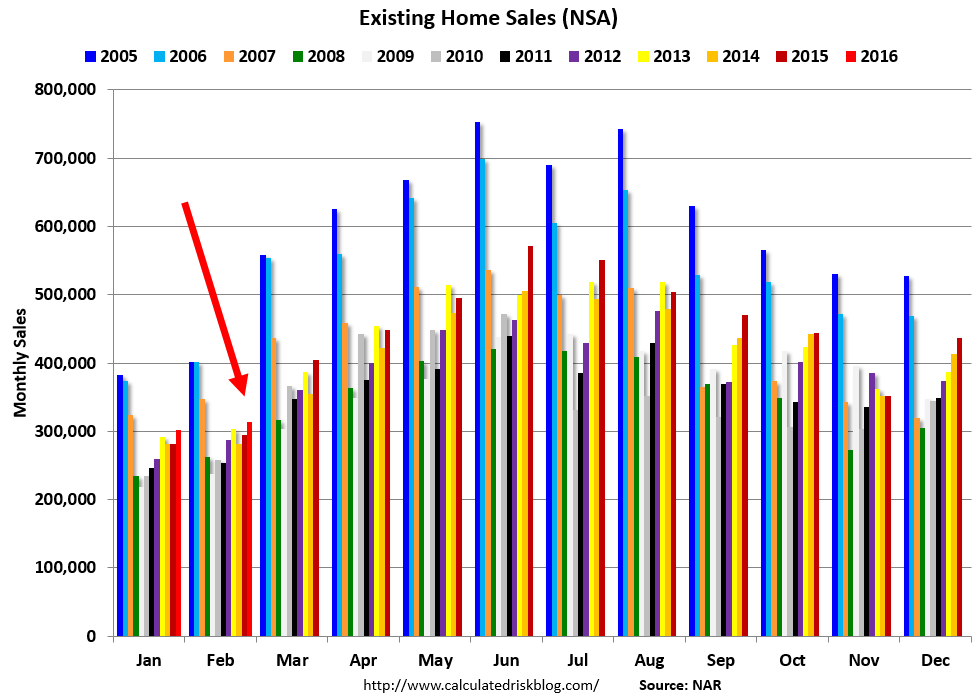

The following graph shows existing home sales Not Seasonally Adjusted (NSA).

Click on graph for larger image.

Click on graph for larger image.

Sales NSA in February (red column) were the highest since February 2007 (NSA).

Note that January and February are usually the slowest months of the year.