Don’t take any dividends for granted today. Business disruption is accelerating as entire industries are being eaten alive.

Uber and Lyft? Killed cabs.

Amazon (AMZN)? It’s crushing retail, and starving their REIT landlords right before our very eyes.

And soon, they might team up to offer more same day deliveries – and make more rivals obsolete!

These types of disturbances have added a new layer to contrarian investing. Before, it was as simple as buying stocks when they were out-of-favor and holding them until they became back in vogue. The “Dogs of the Dow” strategy, for example, usually beat the market by banking the highest blue chip dividend yields – a sign that the tide was ready to turn back in the dogs favor.

But in 2017, it’s not good enough to buy what’s hated. In fact, it’s often dangerous. We income investors must decide whether there the light at the end of the tunnel is real hope, or the lights of an oncoming train filled with Amazon boxes!

Let’s call out three traps. If you own them, sell them – and buy the secure 5% payer I’m going to recommend at the end instead.

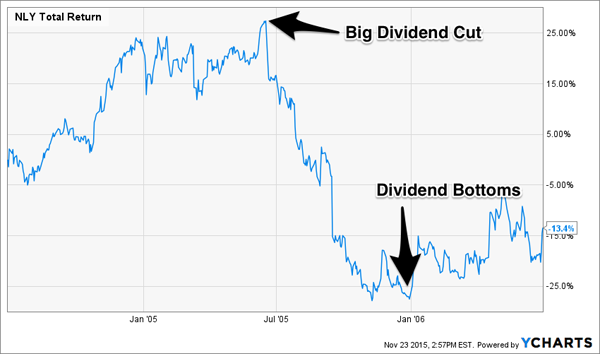

Sell: Annaly Capital and its Inevitable Dividend Cut

Back in the mid-2000s, Federal Reserve Chairman Alan Greenspan sent rates flying from 1% to 5.25%. The natural reaction should’ve been a selloff in Annaly Capital (NLY), a mortgage real estate investment trust (mREITs) that held fixed-rate securities that decline in price when rates rise.

Thing is, it didn’t. For as forward-looking as the market claims to be, NLY shares only headed higher in seeming defiance. Only once Annaly started chopping its payout in mid-2005 did the “original mortgage REIT” get the haircut it had coming, with the stock eventually bottoming at the same time its dividend did, in December 2005.

Investors were warned, and anyone who bought while rates soared higher did so in the face of logic. And Annaly’s dividend wasn’t there to cushion the blow when NLY shares cratered by nearly 50% in half a year.

If You Wait, It Might Be Too Late

You could say that mREITs weren’t a Wall Street niche, and not well-covered more than a decade ago. That’d still be no excuse for what happened in the telecom and retail industries this year.

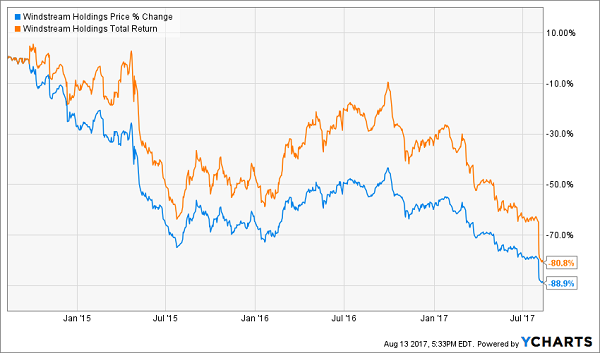

Sell: The “Shocking” Suspension of Windstream’s Dividend

Windstream (WIN) is a diversified provider of telecommunications services across all the U.S. states, offering everything from broadband internet to digital TV to even telephone services. It particularly focuses on underserved rural markets in the Midwest, South and Southeast.

Windstream has for years suffered steady declines in the top line while watching robust profits turn to deep net losses, including a $386 million deficit in 2016. In fact, the company hasn’t been able to cover its payout with earnings since 2013.

The dividend has long been a red flag. After being spun off from Alltel in 2006, Windstream delivered a robust 25-cent quarterly payout that never inched higher. WIN reduced its payout to 15 cents quarterly following the 2015 spinoff of its real estate holdings into Uniti Group (UNIT). Many analysts and other pundits had the right idea, decrying Windstream and its unsustainable dividend … but as shares sank, the yield ballooned.

And in a few corners, bad advice and gambling mentality took hold.

In early March 2017, Cowen & Co.’s Gregory Williams called Windstream a “compelling opportunity” and said “WIN’s fundamentals are far more stable and both the ability and willingness to pay its dividend still remain a non-issue.” This, amid years of business decay, mounting quarterly losses and dwindling operating cash flows!

At the time, shares yielded a robust 10%, and that ballooned to 25% as WIN continued down a path that would see it halved between Jan. 1 and Aug. 2.

It would stand to reason that Wall Street had long priced in a dividend cut, and that Windstream’s announcement Aug. 3 to suspend its dividend would’ve caught nobody by surprise. Yet in the course of two days, Windstream plunged another 40% as speculators fled the stock. They gambled that a 25% yield would somehow be sustainable, then rolled snake eyes.

Windstream’s Problems Weren’t Exactly a Secret

Sell: They Didn’t See Mattel’s Cut Coming, Either?

Toymaker Mattel (MAT) in mid-June slashed its dividend by roughly 60%, from 38 cents per share quarterly to a meager 15 cents. What followed was a quick dip followed by slower but more consistent selling, adding up to a 20%-plus drop in just two months.

While that reaction sniffs of investors caught off-guard and trying to decide what to do with a suddenly smaller payout, the writing was on the wall for some time.

Rival Hasbro (HAS) in 2014 wrested control of the Disney line of princess dolls away from Mattel, which had been peddling Belles and Jasmines since the 1990s. Hasbro’s growing stockpile of toy families such as Marvel, Furby and Star Wars were resonating better than Mattel’s Barbie, Fisher-Price and Hot Wheels, and MAT’s fundamentals quickly came off the rails.

Mattel’s earnings plunged from $2.58 per share in 2013 to $1.45, $1.08 and 92 cents in the subsequent three years – all lower than the $1.58 per share it needed to pay out its annual dividend. Just a couple months before the cut, I warned investors about the perils of Mattel’s dividend. Even a 165% payout ratio wasn’t enough to keep some investors from stretching for a yield of around 7% before the bottom fell out.

Now, gamblers who jumped in even a year ago and haven’t yet bailed are sitting on a yield of less than 2% … not to mention a 50% decline in their original investment.

Buy: A 5% Yield with 586% Upside

Now check out these two dividends. Which would you rather buy today?

Dividend A: Plateauing

Dividend B: Accelerating

Of course you’re better off owning the second one. An accelerating dividend is a sign of business strength, while a slowing payout is a sign of trouble. And since stock prices follow their dividends over the long term, I’d much rather own the one that’s “hockey sticking” versus plateauing.

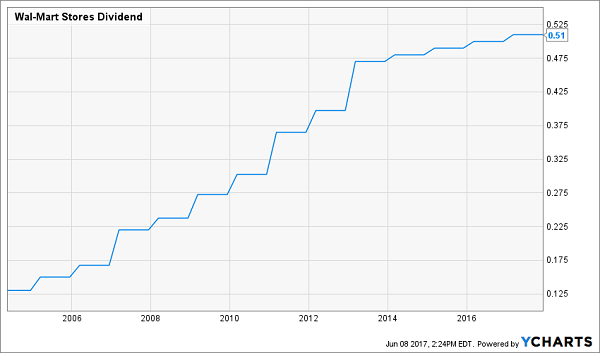

WalMart’s (WMT) business and dividend – the first example – are both plateauing. Amazon is consuming its brick-and-mortar business, and the retail giant has no clue how to actually compete in online e-commerce.

It violated our key rule for business survival in 2017: Avoid being run over by the tech trains!

My favorite tech company to buy today isn’t one of the Big 5. Nor does it play on their train tracks. In fact, this company makes a critical component that is included in every single electronic device on the planet today!

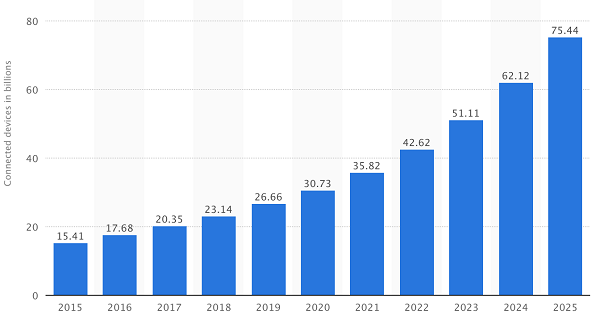

Since there are now more gadgets than humans on Planet Earth, we’re talking about a big market. We’re also talking about a booming one. The number of Internet connected devices alone is expected to top 75 billion in just eight years!

Connected Electronic Devices (in Billions)

Source: Statista

Anyone who buys this stock today is banking a 5% cash yield plus significant price upside in the years ahead – perhaps 586% or more, if history is any indication.

I’d like to email you my full analysis of this company right away – including the firm’s name, its ticker and my recommended buy-up-to price. This stock is a complete “no brainer” to return 12% or more annually for many, many years. Click here if you’d like to receive my report now, and I’ll send you another piece of research, my 7 Best Dividend Growth Stocks With 100%+ Upside right now.