The desperate hunt for yield is getting way out of hand—and it’s setting up a terrific buying opportunity for you and me.

How out of hand?

Consider that some investors are so income starved they’re piling into sovereign bonds from Iraq—a country that’s still a war zone!

The latest issuance of five-year bonds by the Iraqi government was slated for $1 billion. But investors spied the 7% yield on offer here and crashed the doors, racking up nearly $7 billion in orders.

It’s sad, and totally unnecessary.

A Secure Portfolio With a Life-Changing 8% Yield

The worst thing is, in their scramble for income, the herd is charging right past yields that are even bigger—and far safer—here in the U.S.A., like the ones you get in my new “8% No-Withdrawal Retirement Portfolio.”

If you’ve been reading my column over the past two Mondays, you know I’ve been giving you a hands-on tour of this portfolio, which I’ve crafted to hand you $40,000 of income on a $500,000 nest egg.

Two weeks ago, we looked at the first of the three pillars that make up this stout collection of high-yield investments: closed-end funds. I also revealed one CEF with a gaudy 9% dividend yield that’s ripe for buying now.

Last week we looked at pillar No. 2, real estate investment trusts, and I named 2 REITs with 5%+ yields and big upside thanks to the recent—and way overdone—REIT selloff. One of these picks even pays dividends monthly!

Which brings us to the third pillar of this unique crash-proof portfolio, which demands a spot in every investor’s retirement plan—and a safe 7.2% payout you’ll want to put on your buy list now.

The Best of Stocks and Bonds—With a High-Yield Kick

I’m talking about preferred shares.

If you’re not familiar with them, don’t worry. You’re not alone.

Most investors only consider “common” stocks when they look for income. These are the shares in a company you get when you place an order with your broker, such as stock in blue chips like Johnson & Johnson (JNJ) and McDonald’s (MCD).

Preferreds are wonderful hybrids that offer aspects of both stocks and bonds. They can trade on an exchange just like any common stock, but they trade around a par value and dole out a fixed regular payment, just like a bond.

They’re called “preferred” because preferred stockholders have rights ahead of common stockholders if a company crashes into a financial wall: their dividends must be paid before dividends on common stock, and management can’t cut the dividends on preferred shares before it slices the payout on common ones.

Their biggest appeal, of course, is their excellent payouts. Many preferreds yield in the 6% to 7% range.

Problem is, unless you want to spend your time poring over credit ratings or digging out preferreds with cumulative dividends (a benefit that binds a company to pay you in the future if it misses a dividend payout)—you’re in for some work here.

That makes funds the best way to buy in … but not type of funds you’re probably thinking of.

A 7.2% “Preferred” Yield That’s a Bargain in Disguise

The massive popularity of ETFs has trained many folks to zero in on fees ahead of almost everything else.

That works when you’re buying a fund that tracks an index, but it’s a mistake with preferreds, where a great manager with a solid track record is a must. This kind of expertise doesn’t come cheap, of course, but it’s well worth it.

Case in point: the preferred fund we’ll discuss today: the Cohen & Steers Limited Duration Preferred & Income Fund (LDP).

It’s a closed-end fund with a 1.72% expense ratio, a number that would make your average investor holding, say, the SPDR S&P 500 ETF (SPY), with its microscopic 0.0945% expense ratio, choke on their cereal!

But that fee has more than paid for itself: LDP has pummeled two of the most popular preferred-stock ETFs—the PowerShares Preferred Portfolio (PGX) and the iShares S&P U.S. Preferred Stock Index Fund (PFF)—over just about any time period, including the last five years:

“Pricey” Management Earns Its Keep—and Then Some

Even if the competition had been closer, I’d still go with LDP because it yields 7.2%—just above what our risk-happy Iraqi-bond investors are getting! That also trounces the 5.6% and 6.2% PGX and PFF are paying, respectively, so you’re getting more of this return in cash.

And keep in mind the yields I give you are always net of fees. So don’t make the mistake of subtracting management expenses from the yield—that’s already accounted for.

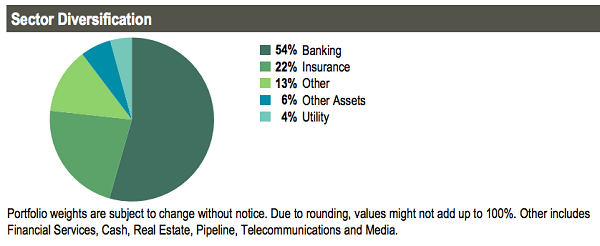

Financial stocks are the main issuers of preferreds, and that’s reflected in LDP’s portfolio:

Source: Cohen & Steers

You won’t have to worry about your money heading off to wobbly corners of the earth here, either: stable countries like the US (47% of assets), the UK, Japan, France, Switzerland and Canada dominate LDP’s portfolio.

The Human Edge

Cohen & Steers executive vice-president William Scapell and senior vice-president Elaine Zaharis-Nikas manage LDP, a duo with 44 years of experience between them.

They put that expertise to good use: to juice LDP’s payout further, they use a modest amount of leverage (around 29% of the portfolio), borrowing cheaply to buy preferreds with higher returns. The difference heads out to investors as dividends.

Which brings me to LDP’s valuation. The currently trades at a 3.38% discount to NAV, down from 1.3% just a few weeks ago and right around the 3.75% it’s averaged in the last 12 months. That gives you some nice downside protection while you collect the fund’s gaudy 7.2% payout.

2 Screaming Buys for 8% Yields and “Crash Insurance”

LDP is a powerful example of what it means to have a seasoned pro at the helm.

And that value doubles in a market collapse, because a savvy veteran can make quick moves to keep your cash safe while you’re collecting those mighty CEF yields.

Here’s the best news: I’ve found a way for you to get the same top-flight management LDP offers plus dial your portfolio’s yield all the way up to a square 8.0%! AND you’ll give yourself another margin of safety to boot!

It’s all thanks to two other preferred-share CEFs that both hold pride of place in my “8% No-Withdrawal Retirement Portfolio.”

Like LDP, their discounts have widened recently. That’s is an insult to their savvy management teams—but a great opportunity for us!

Together with the 4 other cash machines (REITs and CEFs) in my “8% No-Withdrawal Retirement Portfolio,” these incredible investments hand you a rock-solid 8.0% yield— enough to let many folks live on dividends alone, without having to sell a single stock in retirement!

Most investors know this is the right approach to retirement. Problem is, they don’t know how to find 8% yields to fund their lives.

That’s why I specialize in finding safe, under-the-radar high-income options like these.