From the NY Fed: Household Debt Continues to Climb in Third Quarter as Mortgage and Auto Loan Originations Grow

The Federal Reserve Bank of New York’s Center for Microeconomic Data today issued its Quarterly Report on Household Debt and Credit, which shows that total household debt increased by $92 billion (0.7%) to $13.95 trillion in the third quarter of 2019.

This marks the 21st consecutive quarter with an increase, and the total is now $1.3 trillion higher, in nominal terms, than the previous peak of $12.68 trillion in the third quarter of 2008. The Report is based on data from the New York Fed’s Consumer Credit Panel, a nationally representative sample of individual- and household-level debt and credit records drawn from anonymized Equifax credit data.

“New credit extensions were strong in the third quarter of 2019, with auto loan originations reaching near-record highs and mortgage originations increasing significantly year-over-year ”, said Donghoon Lee, research officer at the New York Fed. “The data suggest that households are taking advantage of a low-interest rate environment to secure credit.”

Click on graph for larger image.

Here are two graphs from the report:

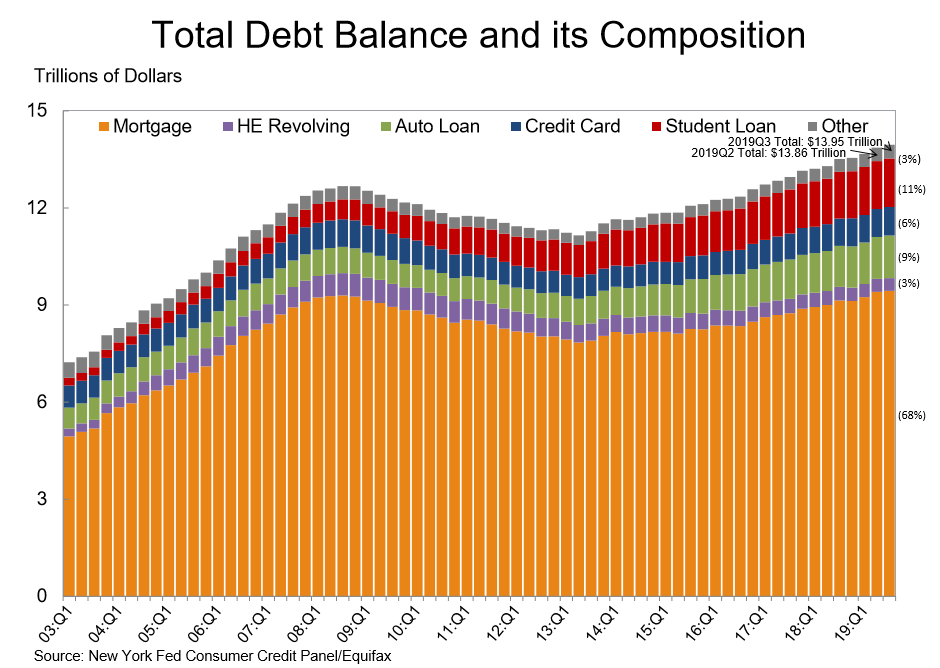

The first graph shows aggregate consumer debt increased in Q3.Household debt previously peaked in 2008, and bottomed in Q2 2013.

From the NY Fed:

Mortgage balances shown on consumer credit reports on September 30 stood at $9.44 trillion, a $31 billion increase from 2019Q2. Balances on home equity lines of credit (HELOC) have been declining since 2009, and this quarter’s decline of $3 billion brings the outstanding balance to $396 billion. Non-housing balances increased by 64 billion in the third quarter, with increases across the board, including $18 billion in auto loans, $13 billion in credit card balances, and $20 billion in student loans.

New extensions of credit were strong for the third quarter. Auto loan originations, which include both newly opened loans and leases, remained high in the third quarter, at $159 billion, a small increase from the last quarter’s volume but the second highest ever observed. Mortgage originations, which we measure as appearances of new mortgage balances on consumer credit reports and which include refinances, were at $528 billion, a notable jump from the $445 billion seen in the same quarter last year. Aggregate credit limits on credit cards also increased, by $27 billion, continuing a 10-year upward trend.

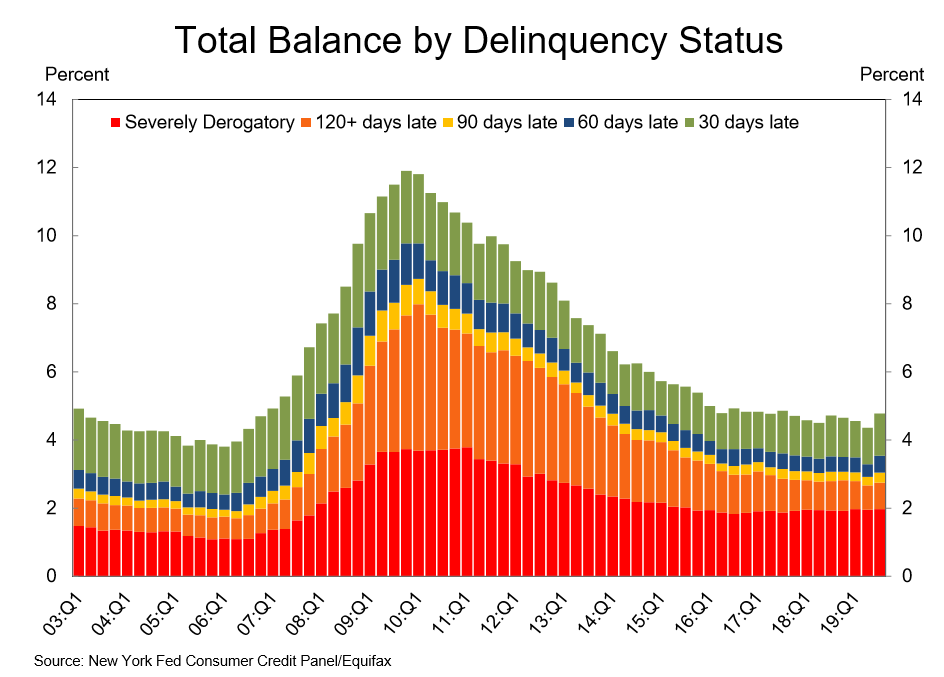

The second graph shows the percent of debt in delinquency.

The overall delinquency rate increased in Q3.

From the NY Fed:

Aggregate delinquency rates worsened in the third quarter of 2019. As of September 30, 4.8% of outstanding debt was in some stage of delinquency, a 0.4 percentage point increase from the second quarter due primarily to increases in early delinquency buckets. Of the $667 billion of debt that is delinquent, $424 billion is seriously delinquent (at least 90 days late or “severely derogatory”, which includes some debts that have previously been charged off that the lenders continue to attempt collection).

There is much more in the report.