The key reports this week are January Housing Starts, Retail sales and Existing Home sales.

For manufacturing, the January Industrial Production report, and the February NY and Philly Fed manufacturing surveys will be released this week.

All US markets will be closed in observance of Washington’s Birthday.

8:30 AM: The New York Fed Empire State manufacturing survey for February. The consensus is for a reading of 6.1, up from 3.5.

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

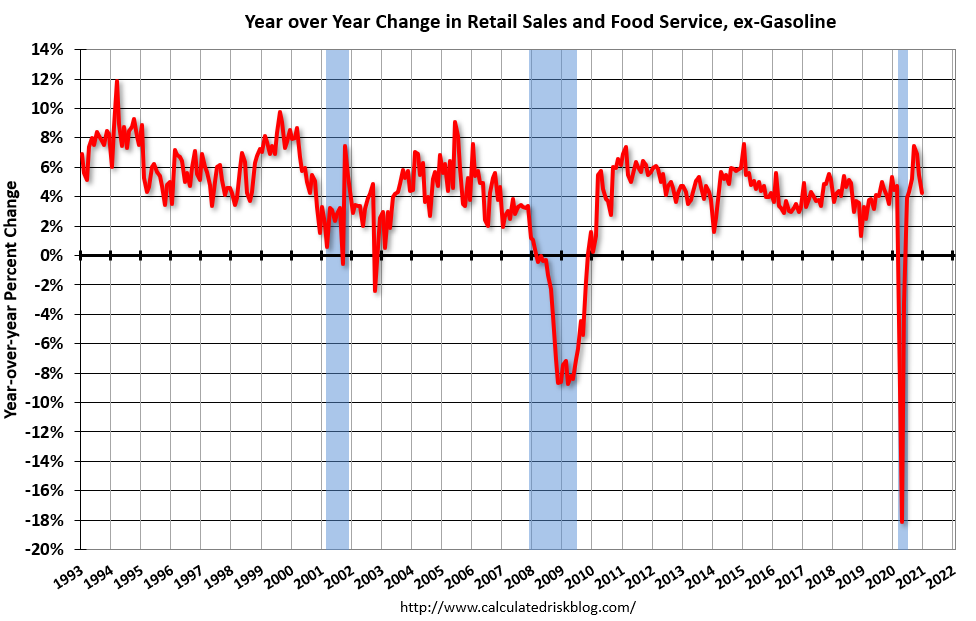

8:30 AM: Retail sales for January is scheduled to be released. The consensus is for a 1.0% increase in retail sales.

8:30 AM: Retail sales for January is scheduled to be released. The consensus is for a 1.0% increase in retail sales.

This graph shows the year-over-year change in retail sales and food service (ex-gasoline) since 1993. In December, Retail and Food service sales, ex-gasoline, increased by 4.2% on a YoY basis.

8:30 AM ET: The Producer Price Index for December from the BLS. The consensus is for a 0.4% increase in PPI, and a 0.3% increase in core PPI.

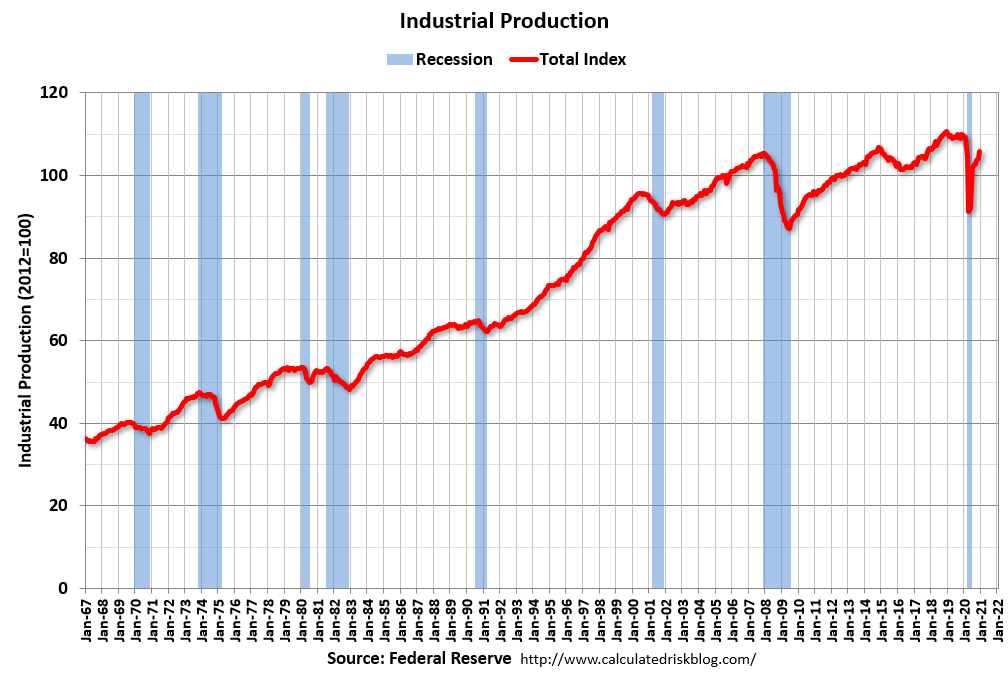

9:15 AM: The Fed will release Industrial Production and Capacity Utilization for January.

9:15 AM: The Fed will release Industrial Production and Capacity Utilization for January.

This graph shows industrial production since 1967.

The consensus is for a 0.4% increase in Industrial Production, and for Capacity Utilization to increase to 74.8%.

10:00 AM: The February NAHB homebuilder survey. The consensus is for a reading of 83, unchanged from 83. Any number above 50 indicates that more builders view sales conditions as good than poor.

11:00 AM: NY Fed: Q4 Quarterly Report on Household Debt and Credit

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for a decrease to 780 thousand from 793 thousand last week.

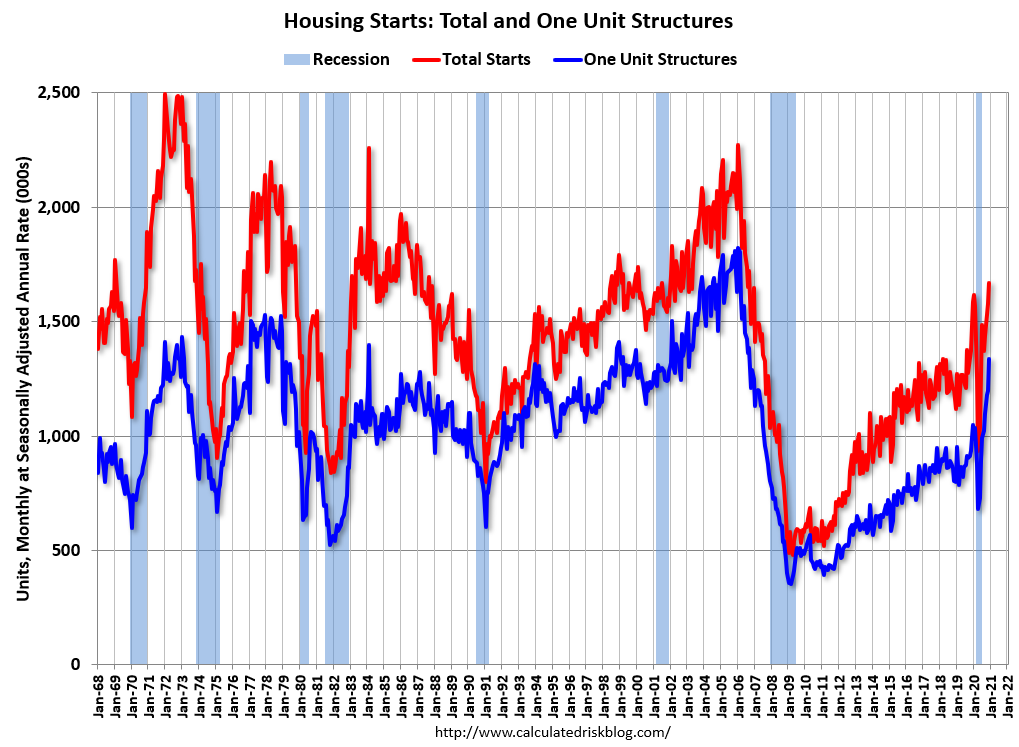

8:30 AM: Housing Starts for January.

8:30 AM: Housing Starts for January.

This graph shows single and total housing starts since 1968.

The consensus is for 1.655 million SAAR, down from 1.669 million SAAR.

8:30 AM: the Philly Fed manufacturing survey for February. The consensus is for a reading of 19.8, down from 26.5.

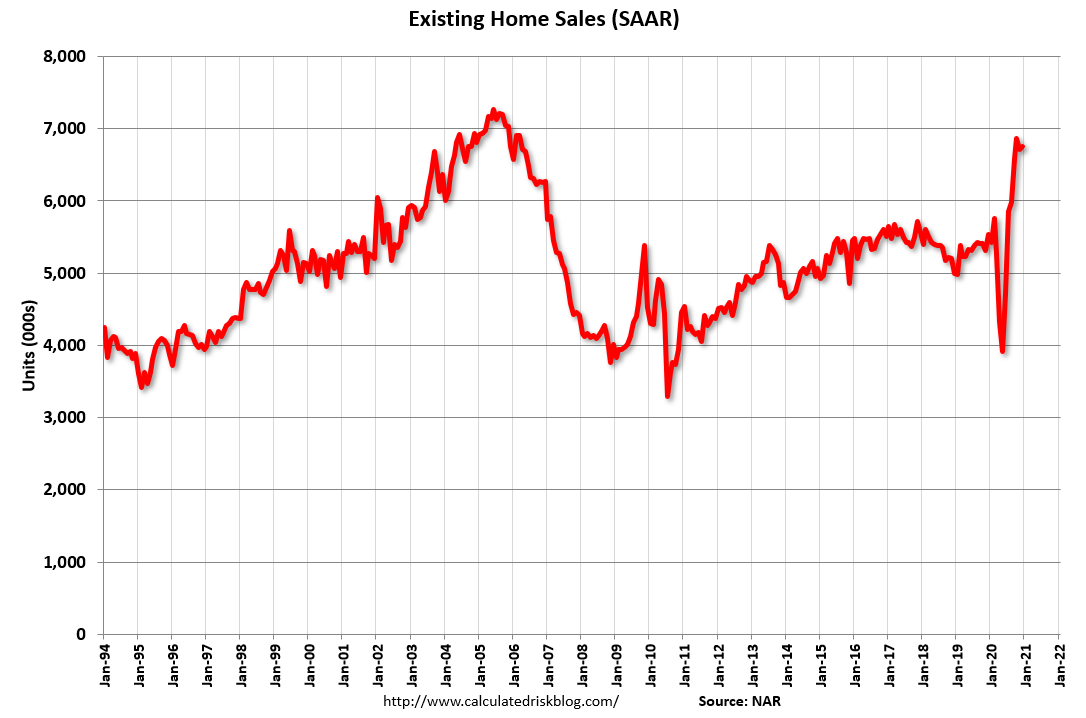

10:00 AM: Existing Home Sales for January from the National Association of Realtors (NAR). The consensus is for 6.60 million SAAR, down from 6.76 million.

10:00 AM: Existing Home Sales for January from the National Association of Realtors (NAR). The consensus is for 6.60 million SAAR, down from 6.76 million.

The graph shows existing home sales from 1994 through the report last month.