After a long winter stuck indoors…

Some of us went a little crazy.

This week, we close in on half of the U.S. population receiving at least one dose of the vaccination.

And let’s just say EVERYONE is ready to get back to life.

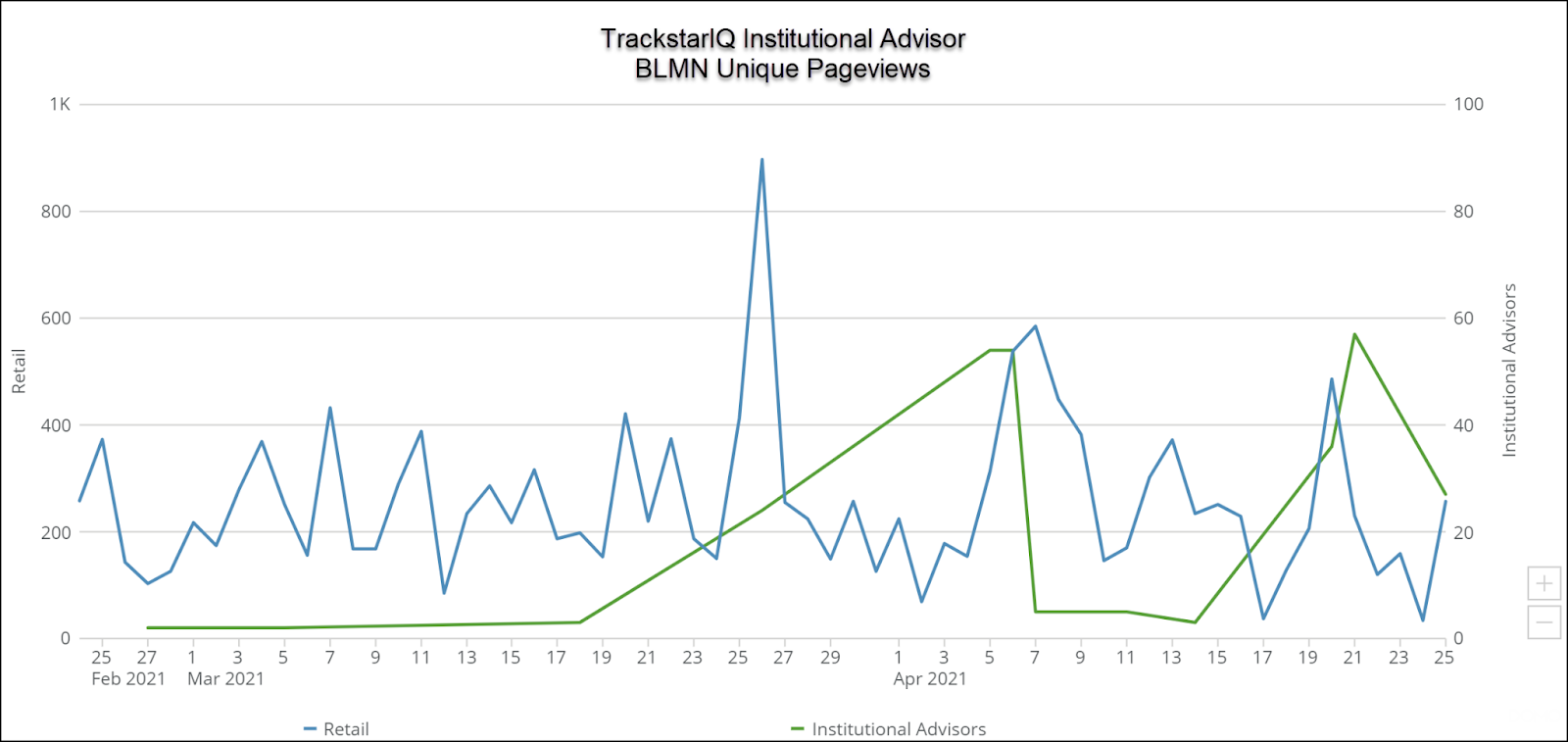

That’s why the surge in search volume for Bloomin Brands (BLMN) caught our attention.

The operating parent of Carraba’s Italian Grill, Bonefish Grill, Outback Steakouts, and Fleming’s Prime Steakhouse hasn’t been in the news lately.

Yet, institutional advisors dramatically expanded their search volume week over week according to our TrackstarIQ data.

It’s a stark contrast to retail searches that remained steady.

With earnings coming up on May 8th, we wanted to take a deeper look at the company.

And what we found was rather interesting to say the least.

A hedge fund take

One of our publisher partners put out an analysis on the stock today.

What’s interesting to note is their analysis of hedge fund activity.

While Bloomin Brands has seen a decrease in interest from large investors, it remains above average against a group of similar stocks.

That’s not entirely surprising given the strength of the stock lately. Shares touched an all-time high, which would be a natural place to take some profits.

Earnings expectations

Q1 earnings year-over-year comparisons won’t help investors make decisions. What’s more important is the rate of revenue growth quarter over quarter.

At the moment, analysts expect revenues to land at $954.62 million, down 5.3% from a year ago. However, that’s 17.3% above Q4.

In fact, revenues grew every quarter since they halved in Q2 last year.

That may not be a ton of comfort to folks. But considering they’ll probably be back to pre-pandemic levels in Q2 of this year, it’s a solid run.

Valuation

Trailing earnings per share are negative, so they don’t give us much insight.

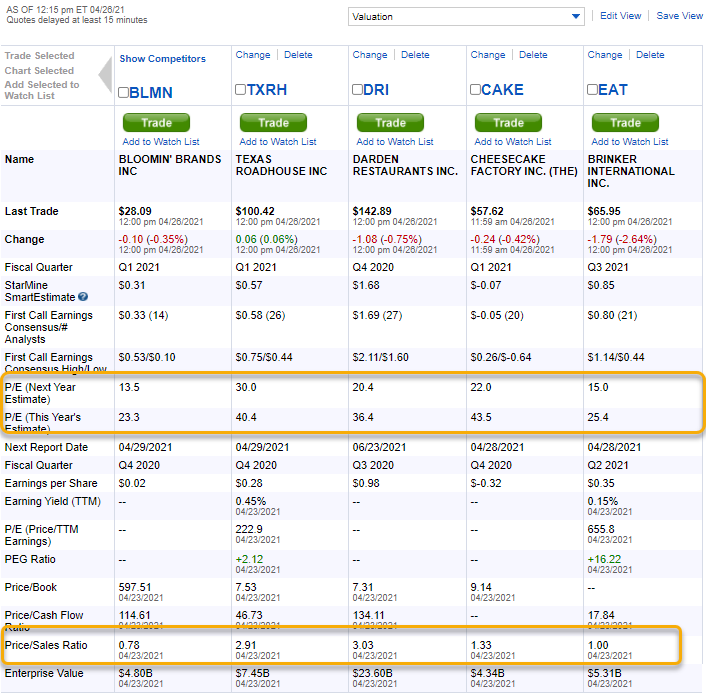

However, we can look at the pre-pandemic EPS which ranged from $1.14 – $1.45. With share prices around $28, that gives us a price-to-earnings (P/E) ratio of 19.3x – 24.56x.

Cheesecake Factory (CAKE) is a good comparison. Using similar assumptions, their P/E ratio would land 20.1x – 26.9x.

Growth just isn’t there

Here’s the problem.

Up until 2019, BLMN saw revenues decline every year since 2014. CAKE saw revenues grow every year since 2011.

Even Brinker International (EAT) and Darden Restaurants (DRI) saw consistent revenue growth.

You can see how the market values them lower than competitors on both a P/E ratio and a price to sales ratio.

The company also carries a much higher proportion of long-term liabilities than competitors. That makes it difficult to fund any initiatives or expansion.

One thing the stock has going for it is high short-interest. Shares sold short (bets on the stock heading lower) as a percentage of total shares available to trade at around 14%. While high, it’s not that much better than CAKE or other peers.

Our hot take

The restaurant category is relatively cheap. But BLMN isn’t the best of the bunch. Cheesecake Factory is a bit more appealing given its history of growth and better balance sheet.

Earnings for CAKE hit on April 28th, so let’s see which company fares better.