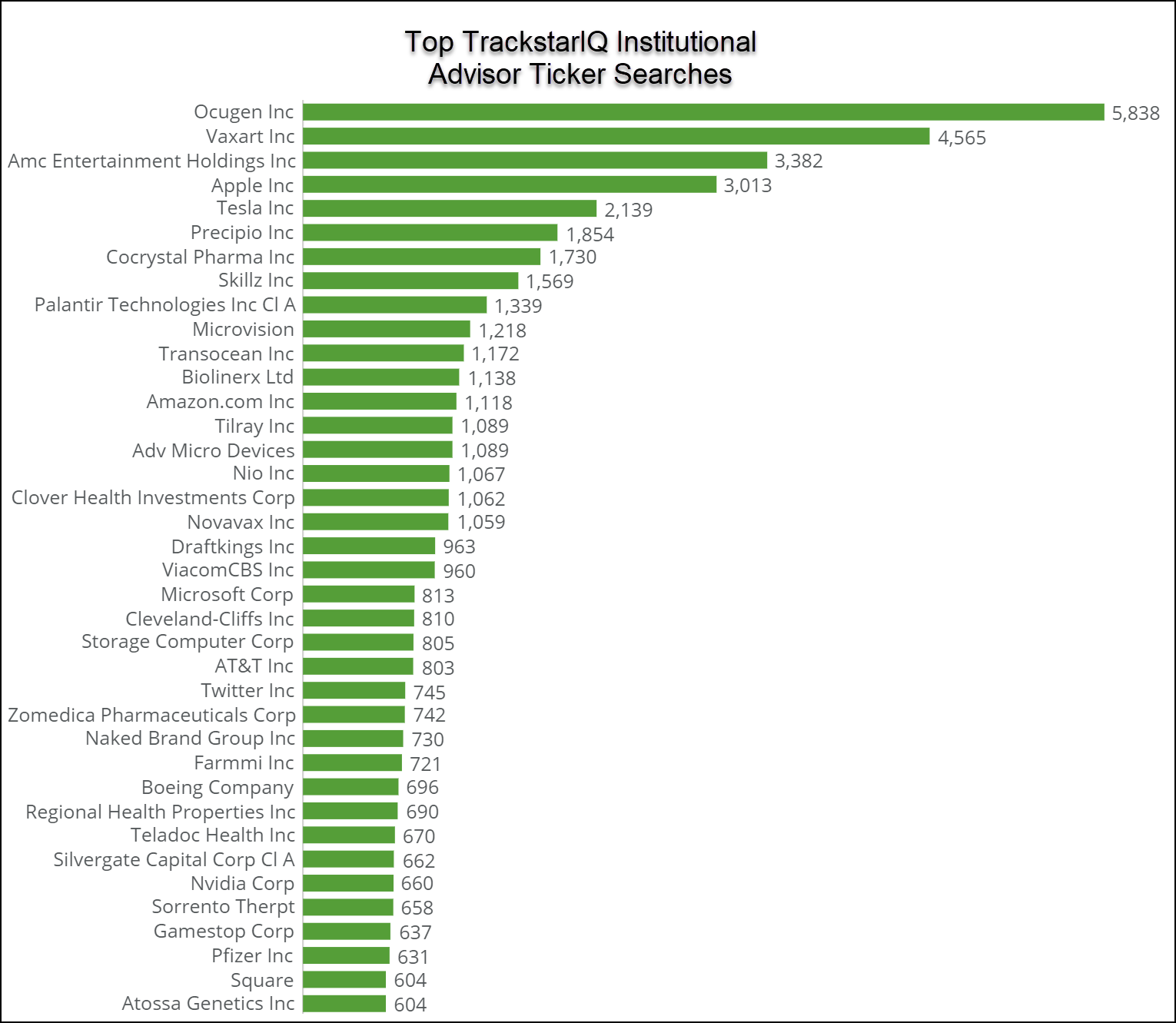

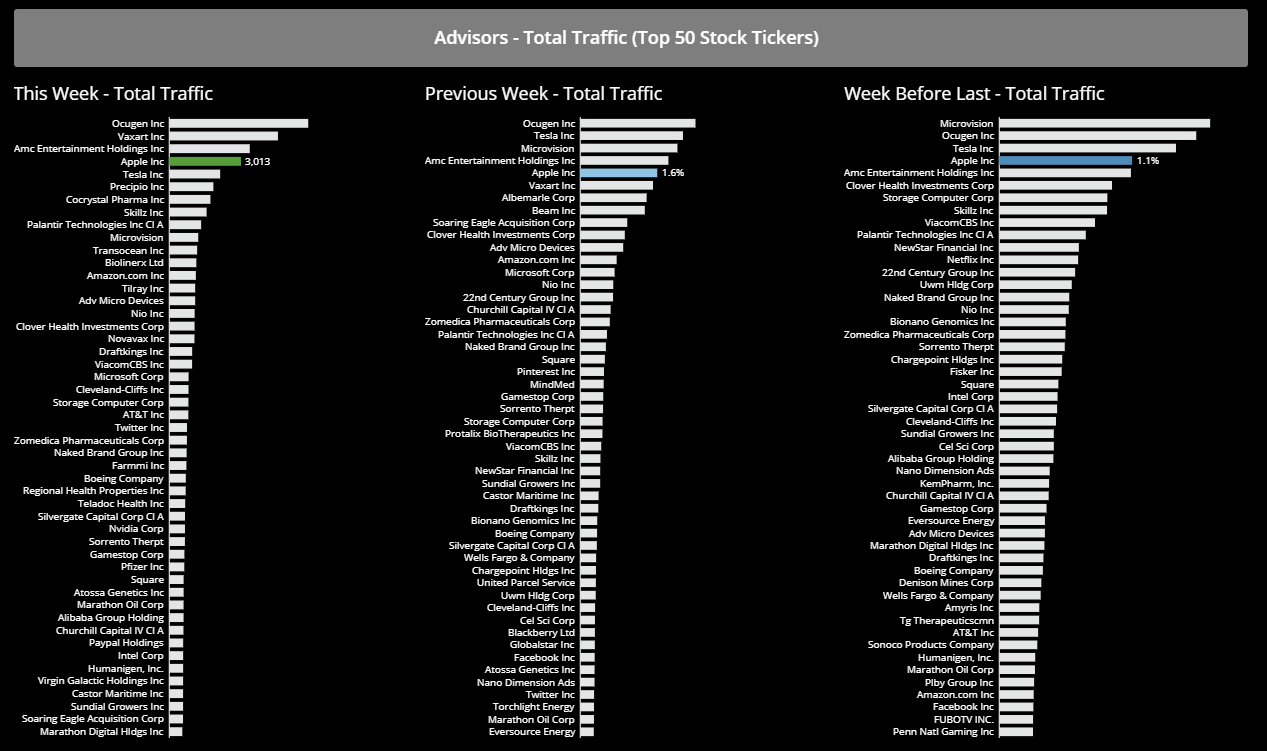

Without fail, Apple (AAPL) lands in the top 5 search results from our TrackstarIQ data for institutional advisors.

This behemoth makes up 5.7% of the S&P 500 and nearly 11% of the Nasdaq 100.

Heck, on a correlation scale of -1 to +1, Apple has a +0.41 correlation to the S&P 500 and a +0.85 with the Nasdaq 100.

Essentially, Apple and the markets move in tandem.

So, what can we expect from the company in the coming months?

Revenue diversification

Apple’s flagship device, the iPhone, generates over 50% of its revenues.

The remainder comes from services, Macs, iPads, and others at 19.6%, 11.2%, 8.6%, and 10.4% respectively.

Go back in time, and from 2016-2019, iPhone sales accounted for 63.4%, 61.6%, 62.8%, and 54.7% of total revenues.

Instead, they’ve moved towards more wearables and services.

Services in particular help mitigate problems with supply chain disruption Apple may face on tangible products. That’s on top of the 66% gross margin achieved on services versus 31.5% on products.

Customers often need a reason to upgrade to newer model phones. 5G technology added that boost last year and is expected to continue for the foreseeable future.

Financial performance

2020 saw revenue growth of 5.51% over the prior year.

But their latest quarter was eye-popping.

Typically, the first few quarters are slow for Apple…except this latest quarter.

Revenues jumped, get this, +50%!

The largest freaking company in the world grew revenues like it was a startup.

Now, the 0.64% dividend yield isn’t that great.

But consider the company currently trades at a price to earnings ratio (P/E) of 27.2x.

That’s ridiculously cheap considering their growth rate.

You won’t find any company of this size like that.

And their balance sheet is rock solid with low interest rate expenses relative to their debt.

Plus, they have plenty of cash and short-term investments on hand to shore up their asset side of the ledger.

Not all glory

The biggest challenge the company faces is the same as many other hardware providers – supply chain issues.

Covid upended everything from glass to microprocessors. Companies from Ford to Caterpillar can’t meet demand because of supply shortages.

Apple isn’t any different.

And while they continue to diversify away from hardware, it still makes up the majority of their revenue, putting them at risk of capping their growth.

Our hot take

The rotation out of technology stocks of late provides a nice entry point for Apple.

Yes, it’s a popular name. This is one of the core holdings for many investors. And for good reason.