When we first saw Big Lots (BIG) come across our screen, we did a double-take.

You see, this stock’s price to earnings ratio (P/E) is…get this 4.3x

I know right?

We wanted to see if this was real.

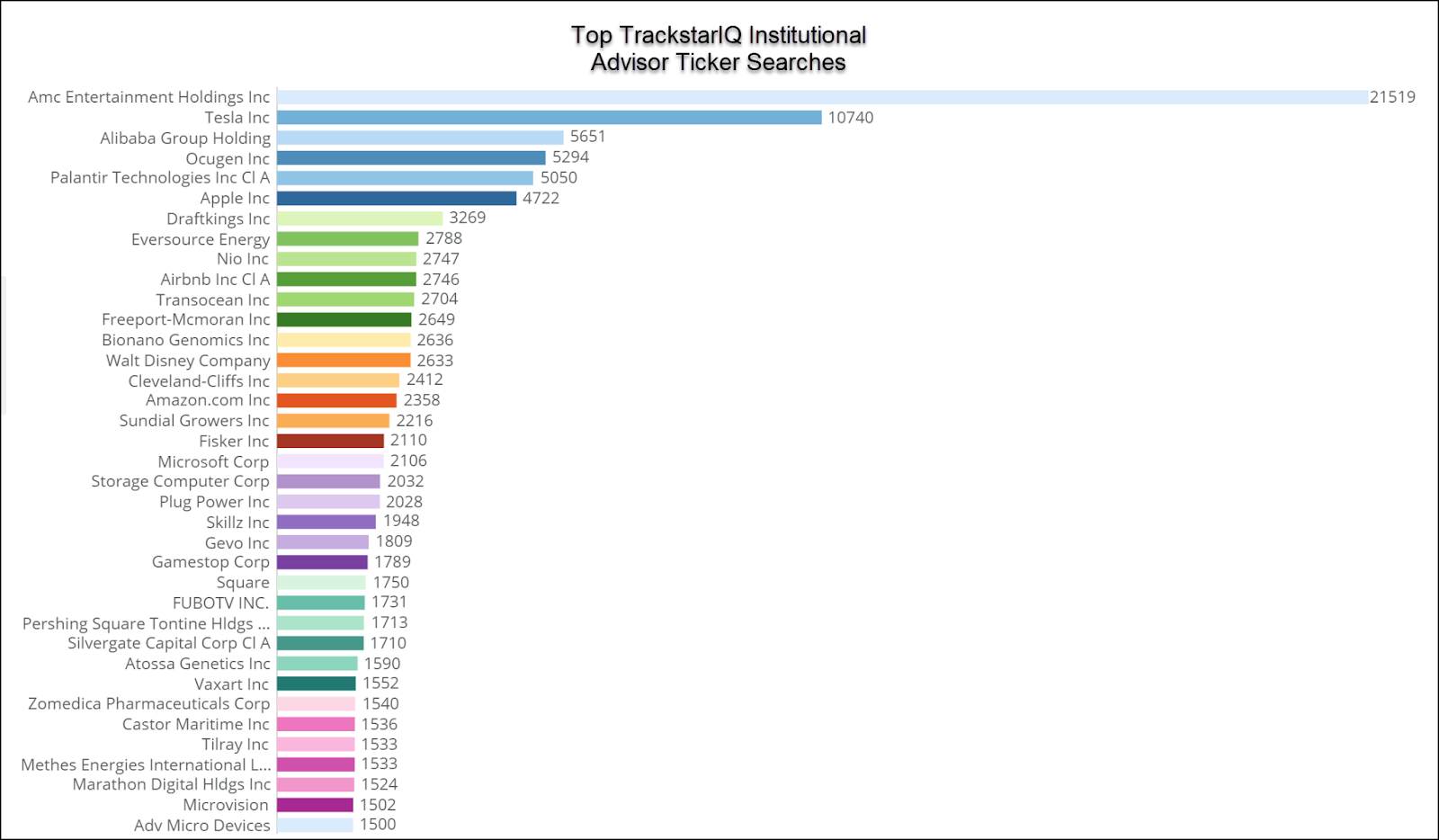

After all, our TrackstarIQ Data showed a spike in pageviews amongst institutional advisors over the weekend.

And earnings aren’t until May 28th.

So what’s the deal?

The cash is real…but temporary

Valuation 101 says we need to split one-time items versus ongoing.

In the case of Big Lots, there’s a very good reason that EPS exploded the last two years.

Unloading their distribution centers helped Big Lots rake in over $641 million.

That certainly helped pad their bottom line.

If we excluded those items, their EPS would have been $4.35 and $1.63 for 2020 and 2019 respectively.

That’s still pretty darn good for 2020 given the pandemic.

Why did they do this?

Big Lots went with a common practice known as sale-leaseback.

Instead of owning the distribution centers, they sell the assets and then lease them.

This often gives more capital flexibility to the company, allowing them to scale more rapidly.

Growth drivers

From a strictly stock trading perspective, BIG smoked competitors year-to-date with shares higher by over 50%.

Overall, shares are up 39.4% in the last six months compared to the industry’s rise of 11.6%.

Looking into 2021, management expects low single-digit comparable store growth.

Still, the company faces enormous challenges including lower foot traffic as well as higher freight and supply chain costs pinching margins.

Operation North Star was designed by executive staff to combat these challenges.

The program focuses on three objectives:

- Drive profitable long-term growth

- Strengthening our home offerings (“Home”), which spans our Furniture, Seasonal, and Soft Home merchandise categories, as a destination for Jennifer

- Growing our own brands, especially our Broyhill® brand.

- Growing store traffic

- Responsibly investing in store presentation initiatives to create an easy shopping experience

- Growing our store count

- Growing our e-commerce sales

- Fund the journey

- Expanding our gross margin rate

- Increasing store efficiency and productivity

- Increasing organizational efficiency

- Encouraging a culture of frugality

- Continuously analyzing our purchasing habits and vendor agreements to ensure we are maximizing our buying power and making cost-effective decisions

- Create long-term shareholder value

You can read more about the specifics on page 95 (21) of the company’s quarterly report.

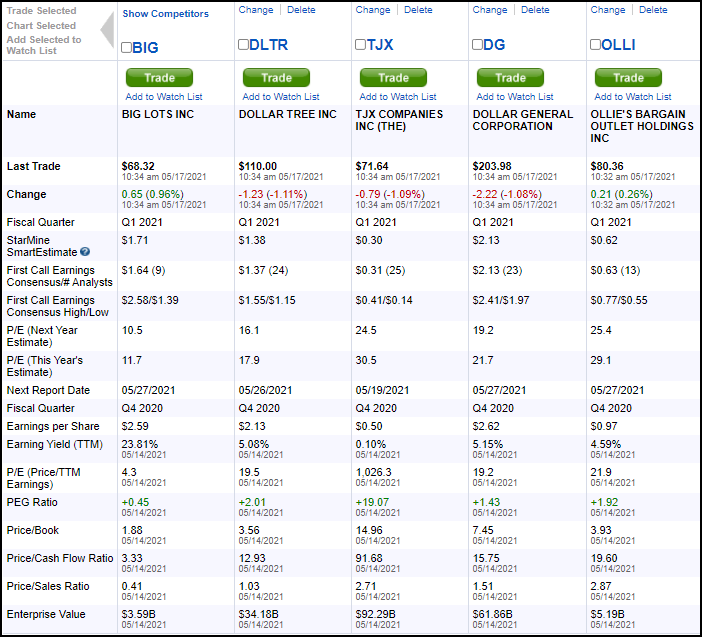

Competitor comparison

Even with shares near all-time highs, the market still values BIG’s stock below similar competitors.

In part, this is due to the tremendous rise in price recently.

However, the company appears better positioned on nearly every metric.

Our hot take

With earnings coming up, any pullback should create a nice entry point for long-term investors.

Plus, you get a nearly 2% dividend payout.

Top-trending tickers, market-moving news alerts: Straight in your inbox!

See the pulse of the market as researched by Wall Street Elites and receive top-trending tickers and other market intelligence to inform your trades.

Sign up for Wall Street Connected – our free daily newsletter that leverages our TrackstarIQ Data.