2020 was a tough year for Airbnb Inc (ABNB).

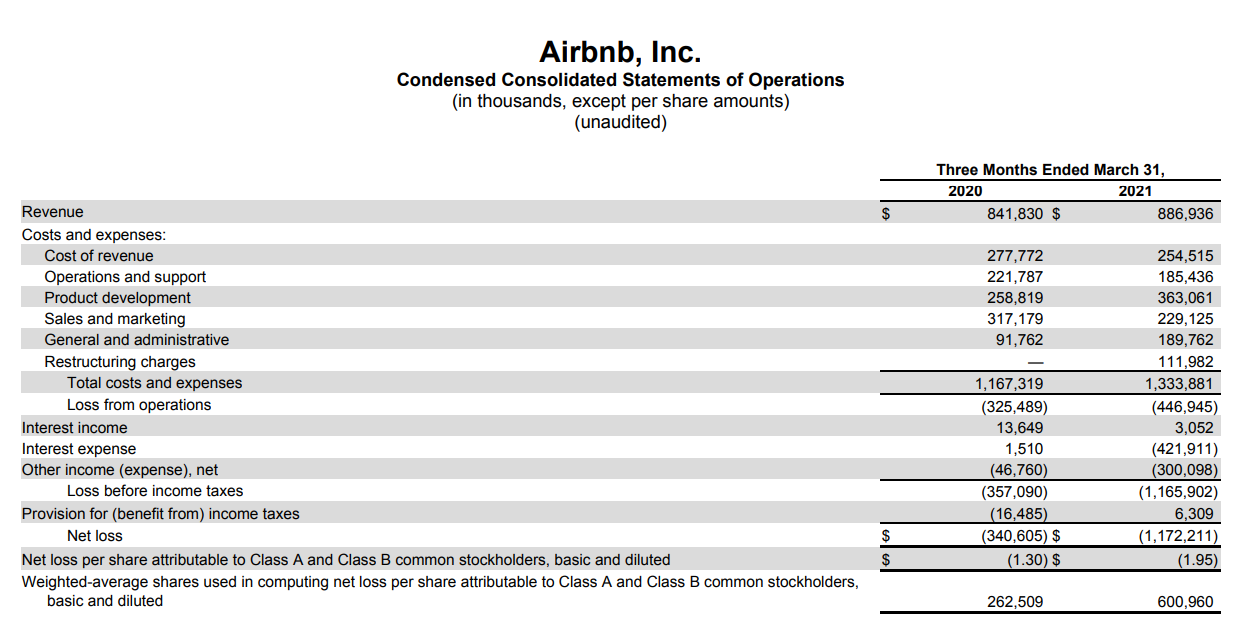

Revenues plummeted ~30%.

Net income losses spiked from $674 million to $4.585 billion.

But if we look beneath the covers, things weren’t actually that bad.

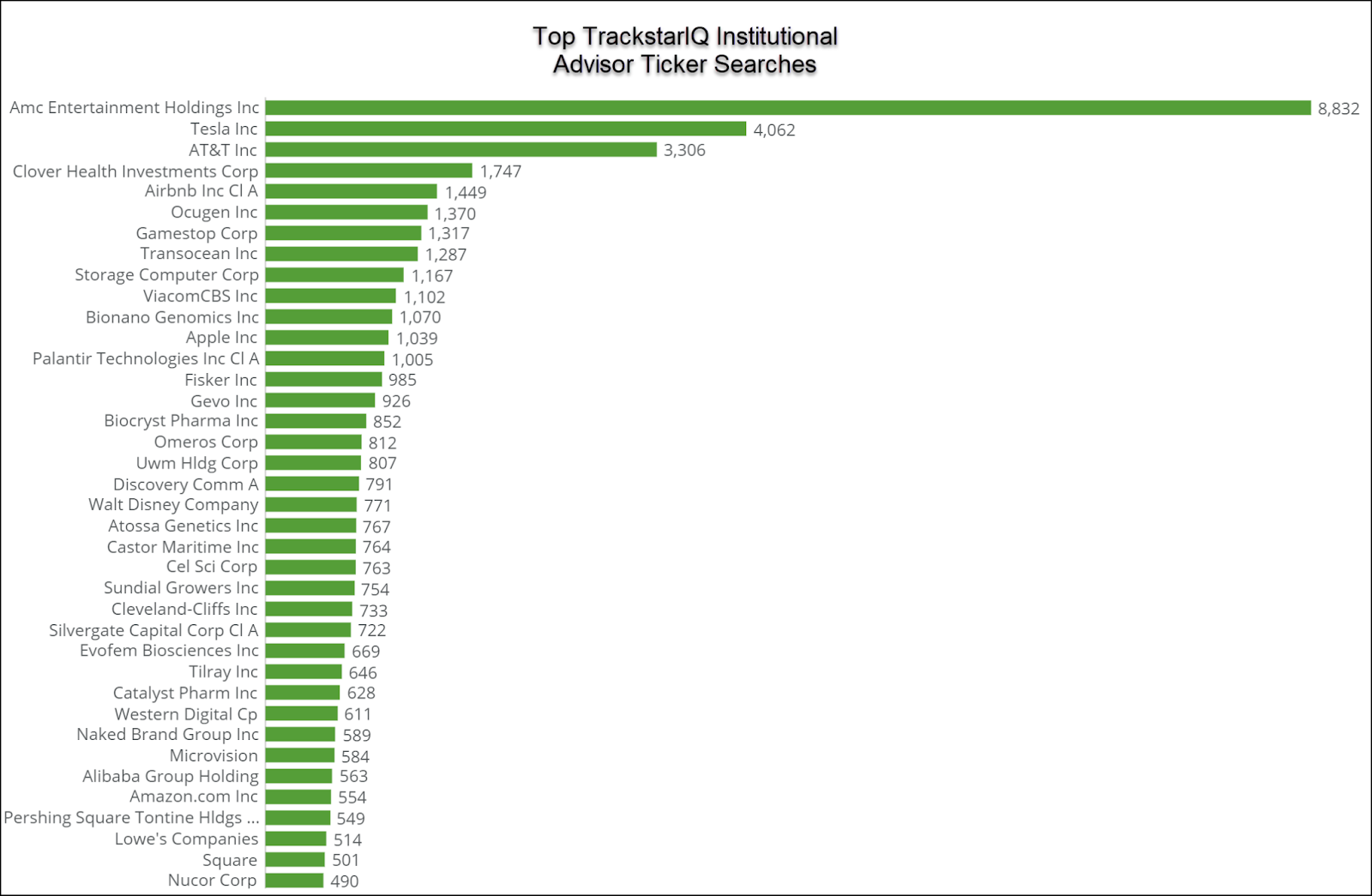

Institutional Advisors made ABNB one of their top search results this week according to our TrackstarIQ data coming in 5th.

With shares sitting below their opening price from their IPO back in December, we figured it was time to take a second look at this hot stock.

It turns out, there’s more here than meets the eye.

The truth behind the numbers

At a quick glance, the income statement for the most recent quarter looks abysmal.

Net losses jumped almost 250%.

The only reason EPS didn’t plummet is they added more shares which diluted the losses.

But as any good finance professor will tell you, bills are paid with cash.

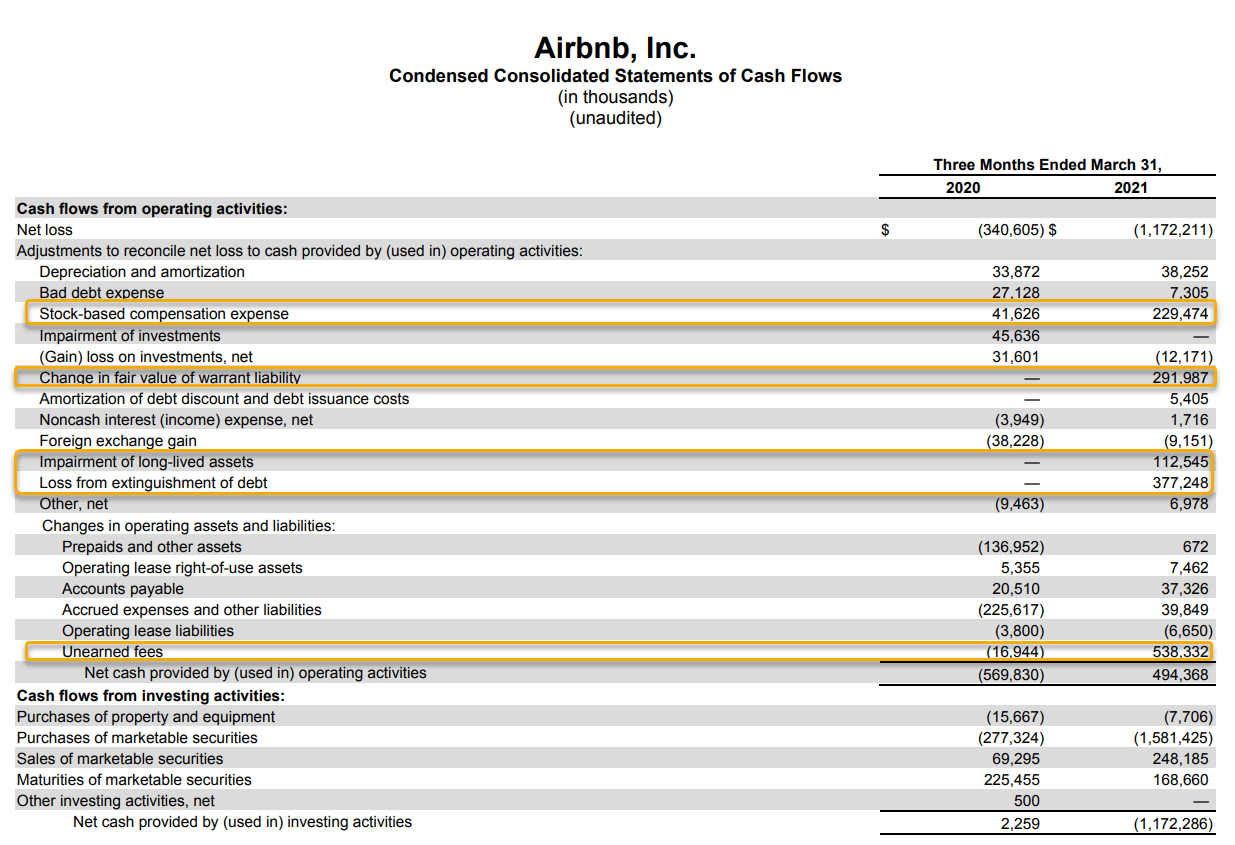

That’s why the cash flow statement paints an entirely different picture.

We highlighted several major items. These are all one-time expenses with the exception of unearned fees which is seasonal.

These major impairments come from items including:

- $377 million loss related to the repayment of term loans

- $292 million mark-to-market adjustment for warrants associated with a term loan

- $113 million impairment related to office space in San Francisco

- $229 million related to stock-based compensation.

All of these added up to $782 million in items unrelated to ongoing operations.

Excluding just these items, we’re left with a loss of $383.9 million compared to the prior year at $340.6 million.

Outlook

In Q1, 2021, ABNB processed 75% more bookings than the prior quarter.

Nights booked through the platform surged 39%.

Their average daily rate increased 25% quarter over quarter.

All this illustrates a growing trend amongst hotel and leisure – pent-up demand is real.

People want to get back to their normal lives.

And with many forgoing vacations for all of 2020, 2021 looks much busier.

In their latest report, the company expected adjusted EBITDA (earnings before interest, taxes, depreciation, and amortization) to be lower in the first half than the second due to seasonality and investments.

However, the company expects to turn a breakeven or slightly positive EBITDA in the second half, a huge milestone for the company.

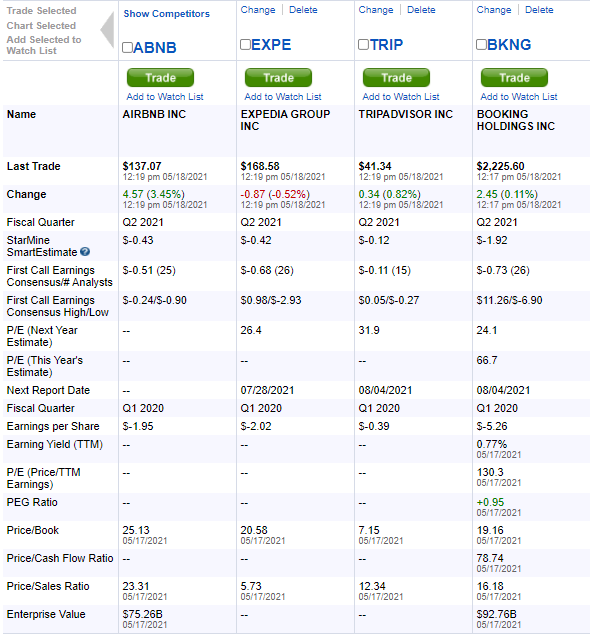

Competition

Without positive earnings, we tend to evaluate companies against their peers through price to sales ratios or similar metrics.

In that regard, ABNB comes in a bit more expensive than similar companies.

What’s worth noting is the growth rate for ABNB is expected to far outpace the competition due to its specific niche.

Our hot take

Airbnb is an interesting opportunity. Given the potential to turn profitable in the next couple of years and the unique business model, this could be a winner over the next decade.

Top-trending tickers, market-moving news alerts: Straight in your inbox!

See the pulse of the market as researched by Wall Street Elites and receive top-trending tickers and other market intelligence to inform your trades.

Sign up for Wall Street Connected – our free daily newsletter that leverages our TrackstarIQ Data.

Click here to learn more