Disruptors love to shake up antiquated industries.

Think banking.

Think shipping.

Think furniture.

That last category hadn’t been touched until recently.

The Lovesac Company (LOVE) stepped into the stogy sector with technology and design never before seen.

Investors loved what they found.

Shares of the company zoomed over 200% since their debut on the Nasdaq in 2018.

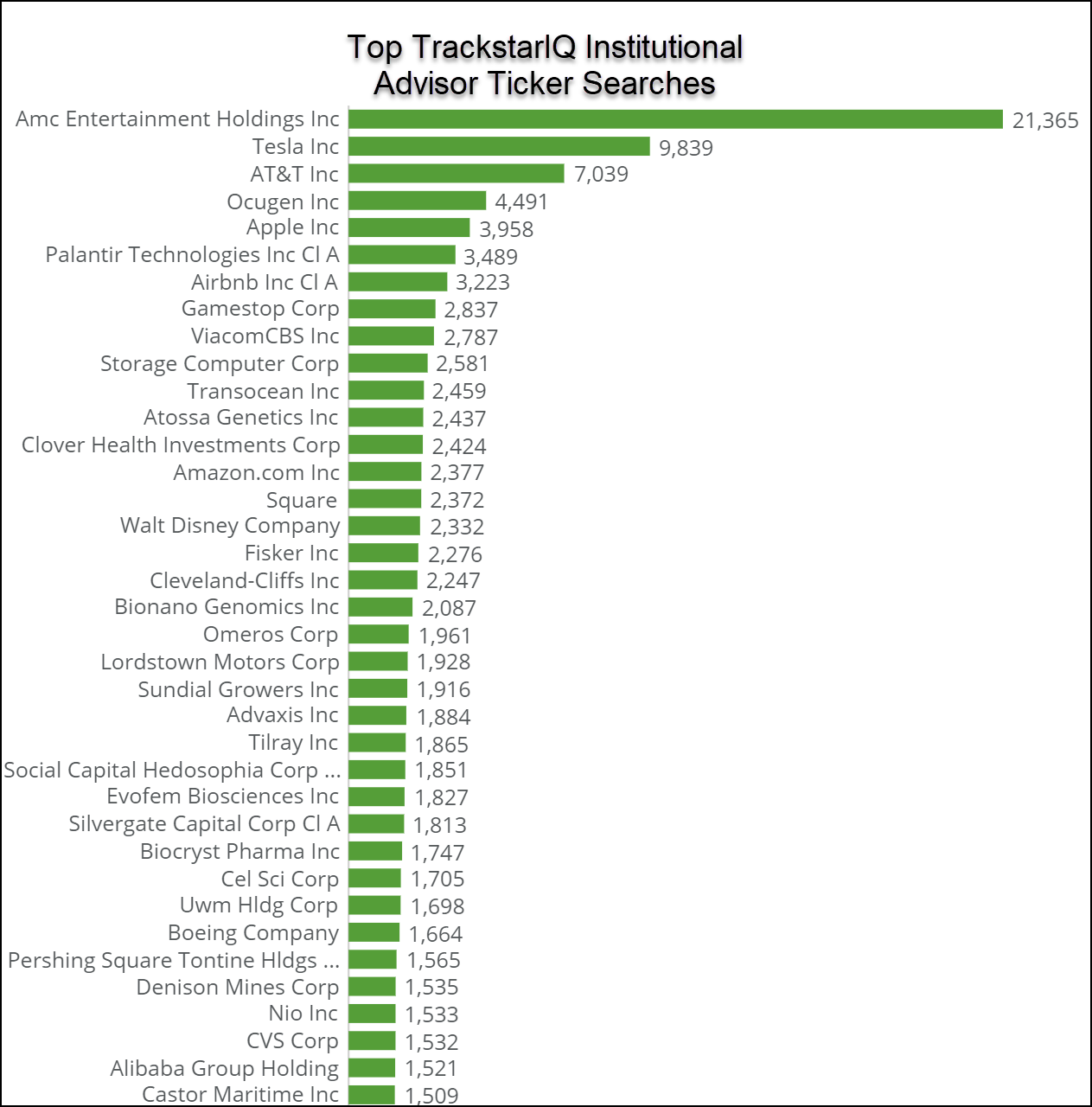

And a recent surge in institutional advisors searches from our TrackstarIQ data suggests the epic run may not be done.

As we dug into the stock and the company, we found a compelling reason why shares could break out to new all-time highs in the near future.

Unique value proposition

Normally, we would start with a discussion about the company itself.

But we think a better place would be a comparison to their competition.

La-Z-Boy provides a great foil Lovesac.

Anyone who grew up in the ‘80s and ‘90s had a La-Z-Boy recliner or a friend with one.

They were basically chair beds that snuggled you in a cocoon of fluff.

These days, the company plods along at a respectable 3%-4% growth rate.

Lovesac looked at the industry and decided it was time to bring in the change.

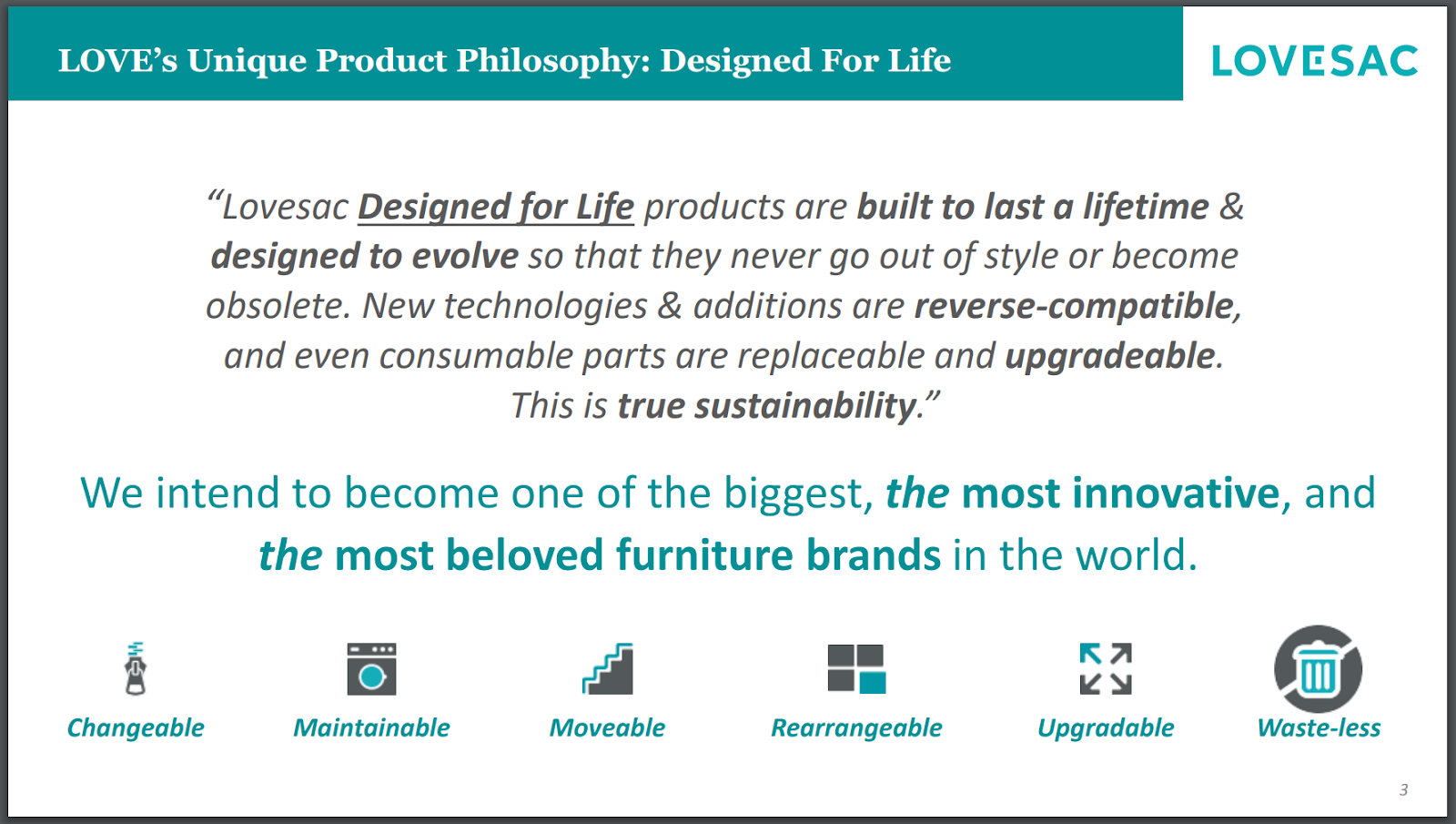

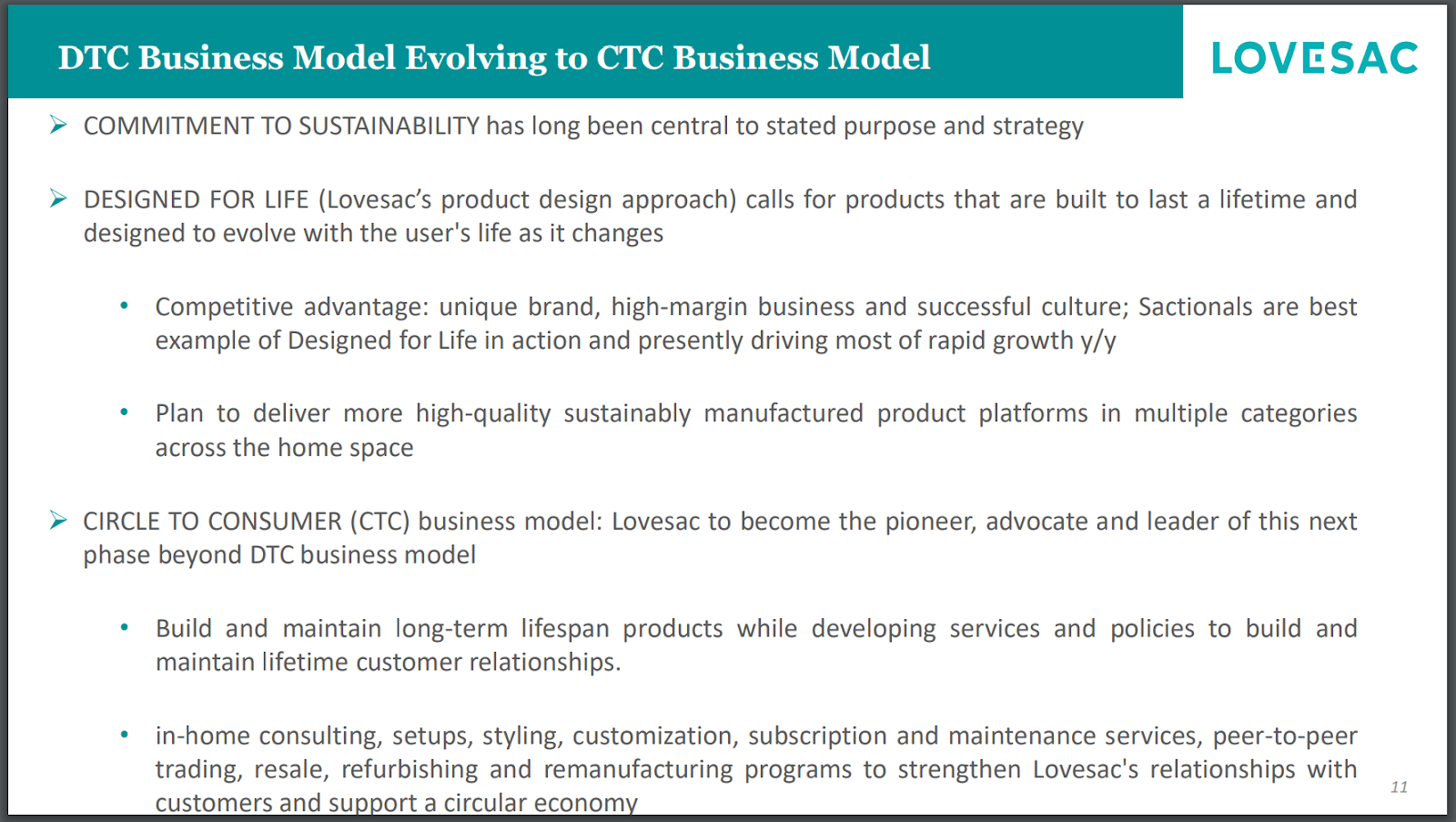

Leveraging technology and branding, the company did a fantastic job with its mission and vision statements.

You see, Lovesac’s furniture is designed in such a way that you can mix, match, move, and upgrade pieces to suit your specific needs.

But the innovation isn’t limited to their products.

Management deployed an omnichannel marketing strategy, with showrooms, store-in-store partnerships with Best Buy, as well as a robust online presence.

What’s we found the following slide from their most recent presentation fascinating:

This clearly articulates not only where they are now, but where they want to go.

Lifestyle branding and deep relationships are proven success factors. Yet, few companies understand how to implement them.

They should take a notes from Lovesac.

Price catalyst

2020 was a difficult year for nearly everyone.

Unless you were Lovesac.

Despite the pandemic, the company turned a profit over the last two quarters.

And revenue skyrocketed.

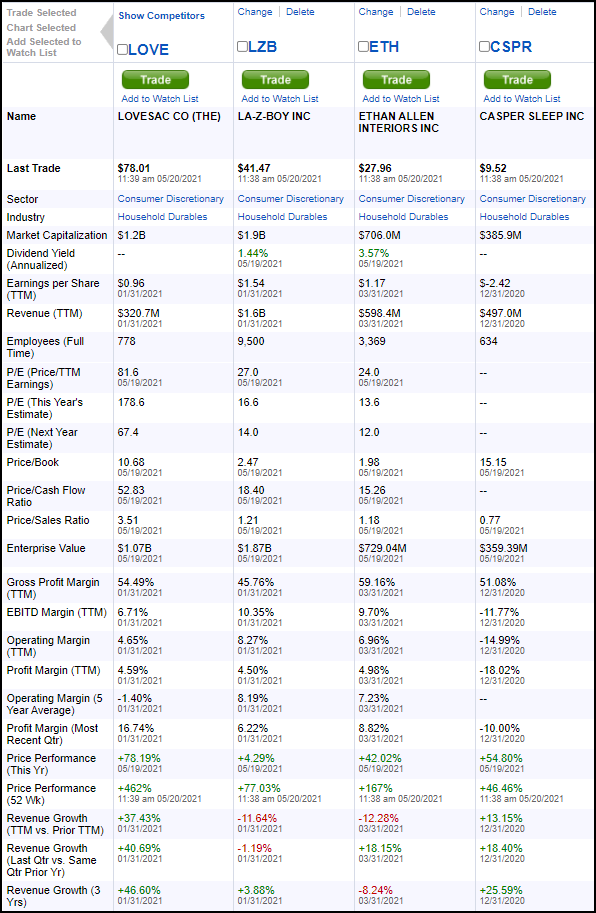

Which brings us to an interesting comparison with its peers.

There are a few items we want to highlight.

First, the growth for LOVE blows away traditional furniture stores like La-Z-Boy and Ethan Allen (ETH).

Second, despite revenues that are only a fifth of LAZB, the market cap is nearly 2/3rds, implying investors see a lot of potential in LOVE.

Third, a niche company like Casper (CSPR) has yet to turn a profit. Lovesac did it the last two quarters.

Lastly, if LOVE had the same operating margin as LZB, next year’s forward price-to-earnings (P/E) ratio estimates would be closer to 35x, which is about in line with the S&P 500. Yet, LOVE grows at close to 40%.

Did we mention that the stock carries a 16.12% short float, making it highlight susceptible to a short-squeeze?

Our hot take

By all appearances, Lovesac is a textbook case of what a company should look and feel like in 2021.

They have a great product and vision not to mention a solid financial performance.

Keep this one on your radar. If markets pull back hard, this could be a nice play to add to a portfolio.