Since 2013, revenue for China’s FinTech sector exploded more than 20-fold.

In 2019, over 800 million people used digital payments in China, more user volume than any other service.

Right now, the company trades at an incredible 9.5x price-to-earnings ratio (P/E) compared to the S&P 500’s 44.64x.

Does the discount accurately reflect the risks in this stock?

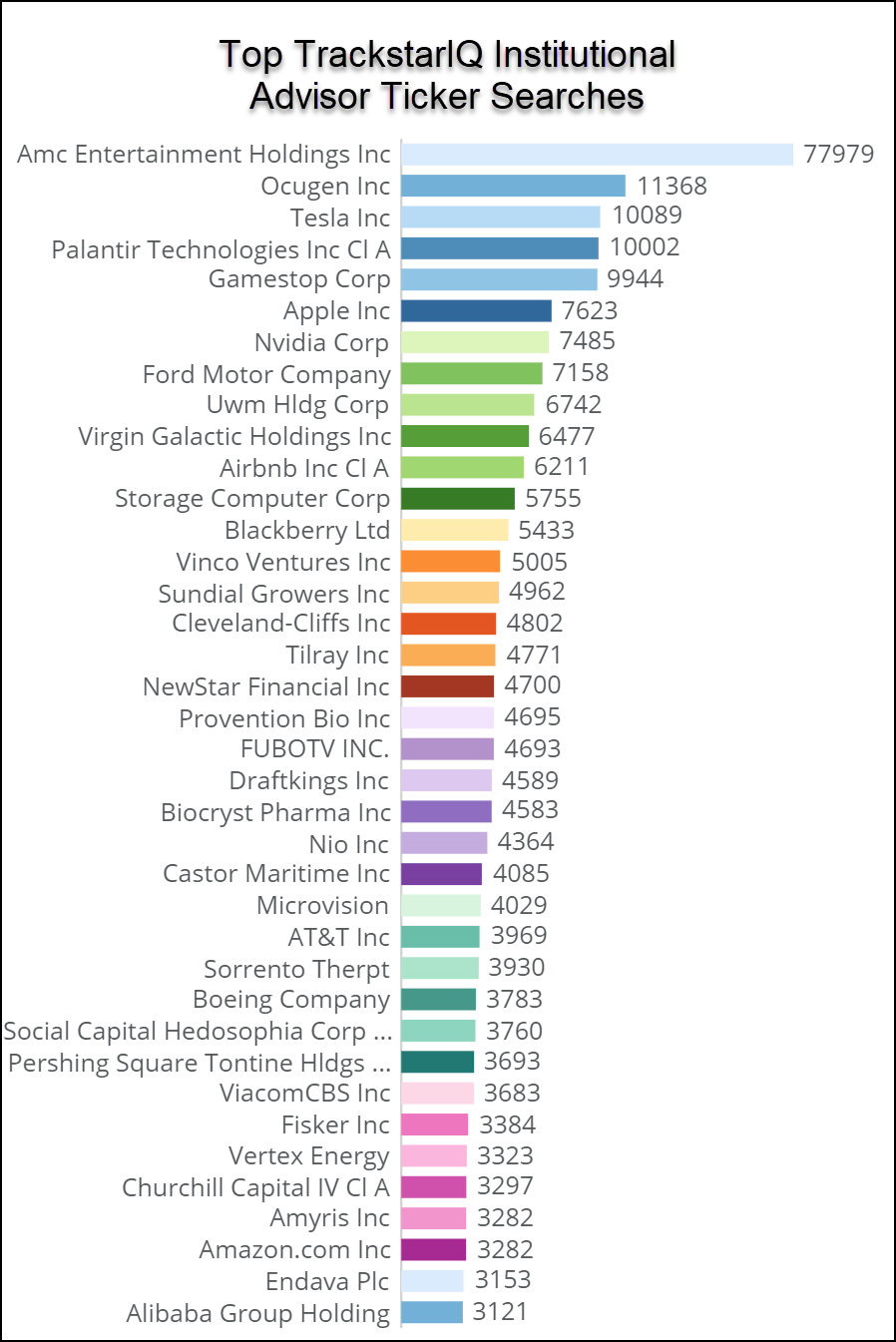

After noting the surge in search volume among institutional advisors in our TrackstarIQ data, we decided it was worth a look.

Who is FinVolution?

Started back in 2007, PPDAI Group FinVolution entered the lending space, connecting borrowers and lenders.

Initially, they focused on P2P loans, much as LendingClub did in the U.S.

Since the recent crackdowns on China’s shadow banking system, FinVolution moved to exclusively connect borrowers with institutional lenders.

Their current model connects borrowers with lenders, where they take a cut of each transaction.

The company isn’t limited to mainland China either as they operate in Indonesia, the Philippines, and Vietnam.

Changing over

Bears are quick to point out FinVolution lags behind its peers like 360 DigiTech (QFIN) and Lexin (LX).

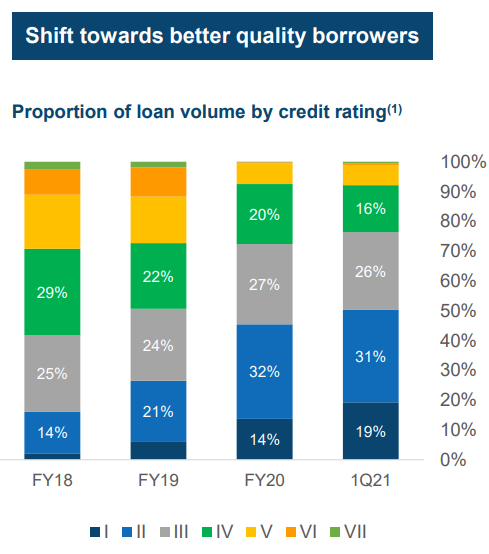

Yet, the company’s done a remarkable job in shifting its portfolio towards higher-quality borrowers while maintaining breakneck revenue growth at 26.8% year-over-year.

During the fourth quarter of last year through the most recent quarter, FinVolution took charges against credit losses for ‘quality assurance commitment.’

These are related to the adoption of ASC 326 in January 2020.

When the company released their Q4 earnings in March, shares skyrocketed over 93% in one day!

Not so fast

As we went through the financial statements from both the company and various data providers, it became apparent that numbers were not going to match.

Take the 2020 revenues for example.

Company reports show 2020 net revenues of 7.563 RMB (Ren Min Bi: China’s official currency).

Morningstar had them at 6.450 RMB.

One item of particular concern is that Morningstar shows a drop in Q4 revenues from 1,793 million RMB to 740 million RMB, climbing back to 2,113 million RMB in Q1.

S&P Global has them at $981M vs the company report of $1.159M.

Some of this has to do with currency adjustments.

But it also highlights the challenges of investing in foreign companies.

Remember, FINV is an American Depository Receipt (ADR). That means a financial firm that operates in both countries buys the stock in China and then issues shares against that in the U.S.

As an owner, you can’t vote or participate in most shareholder activities.

Our hot take

Generally speaking, while the exact numbers don’t completely align, the overall trends do.

But this is definitely a speculative play even given its size.

Overall, the company has a solid business plan with expansion ideas in Southeast Asia. And the one thing nearly all the numbers agree on is the company hasn’t lost money in a long while.

Plus you get a 2.3% dividend yield while you wait, which isn’t too shabby.

Top-trending tickers, market-moving news alerts: Straight in your inbox!

See the pulse of the market as researched by Wall Street Elites and receive top-trending tickers and other market intelligence to inform your trades.Sign up for Wall Street Connected – our free daily newsletter that leverages our TrackstarIQ Data.

Click here to learn more