We know about the microprocessor shortage impacting the auto industry.

So why are shares of Toyota Motors (TM) at all-time highs?

I’ll tell you why.

Because they’re incredibly cheap.

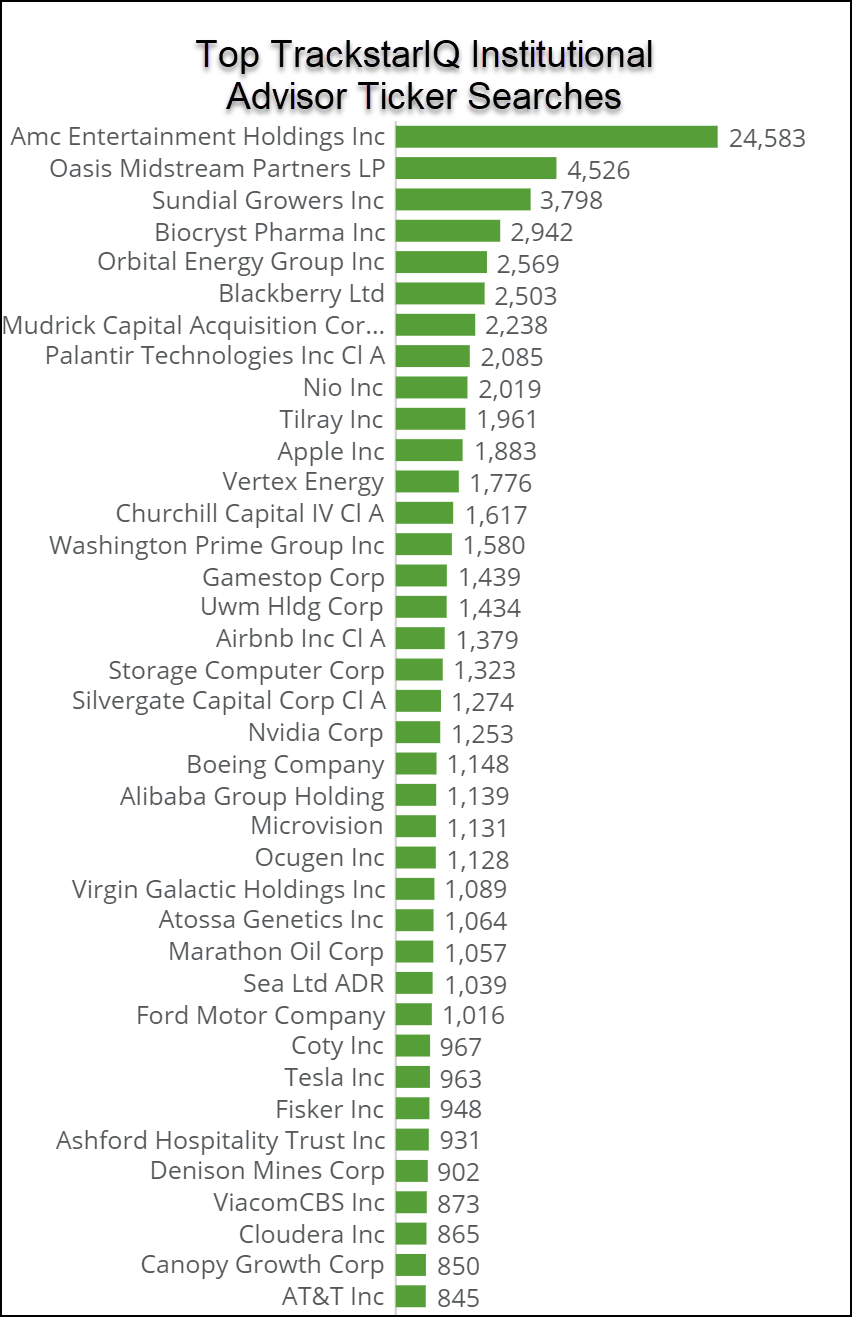

And clearly, institutional advisors think so as well.

Recent search data highlighted increased pageviews for the Japanese automaker.

But with an incredibly cheap price-to-earnings (P/E) ratio just above 12x, why aren’t more people interested?

As we dug into the company, we noticed something quite unusual.

A history of low valuations

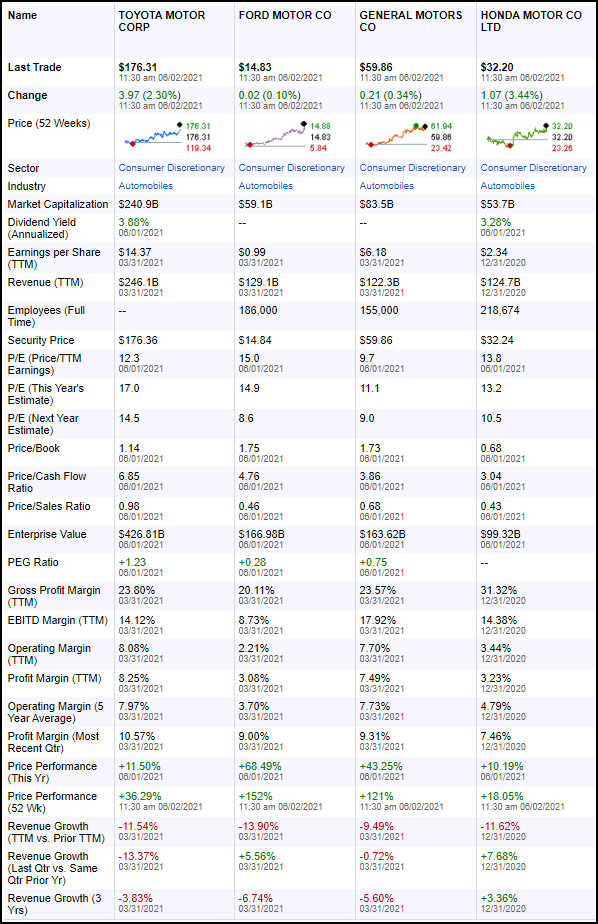

With the S&P 500 trading at a P/E ratio over 44x, 12x seems an incredible deal.

That is unless growth is questionable.

In 2020, Toyota revenues declined 0.98%, while they had grown by 2.88% in the prior year.

For their most recent quarter, revenues shot up 8.03% year over year.

But operating margins slipped from a steady 8.2% to 7.2% in the last 12 months.

No joke, the P/E for the company rarely gets above 10x.

What’s interesting is how the dividend yield tends to stay just below 3%.

However, the entire automotive manufacturing industry doesn’t get much love.

When you compare Toyota to its peers, you realize the entire sector is cheap compared to the broader market.

One could argue that Toyota is expensive when you compare it to Ford (F), General Motors (GM), or Honda (HMC).

Yet, it boasts the best profit and operating margin.

Future prospects

Ford plans to invest $29 billion towards EV and autonomous vehicles through 2025.

GM is at $27 billion.

Toyota is at $13 billion over ten years. Most of the money will go towards increasing production capacity.

Toyota’s CEO isn’t keen on an aggressive shift towards electric vehicles, despite being a pioneer in the field along with fuel cells.

One major change is Toyota’s move away from Toyota-specific standard parts, instead integrating more global standard parts. Their long-term goal is to have 70%-80% common parts.

Since their major recall back in 2013, Toyota struggled to maintain its ‘quality’ against the Detroit players, making it more of a perception than a reality these days.

In reality, there aren’t a ton of growth drivers for Toyota. Over the next few years, the company faces more headwinds than tailwinds.

Our hot take

Compared to their peers, Toyota experienced a much shallower decline in 2020 than the others, which led to smaller gains on the way up.

Given their size and breadth, this is probably the ‘safer’ of the automotive bets out there. But, you give up a lot of growth potential.

Top-trending tickers, market-moving news alerts: Straight in your inbox!

See the pulse of the market as researched by Wall Street Elites and receive top-trending tickers and other market intelligence to inform your trades.Sign up for Wall Street Connected – our free daily newsletter that leverages our TrackstarIQ Data.

Click here to learn more