Did you know that steel demand only dropped by 0.2% in 2020?

You know why?

China.

They account for half the world’s steel demand.

And like many commodities, steel prices squeezed higher on supply constraints.

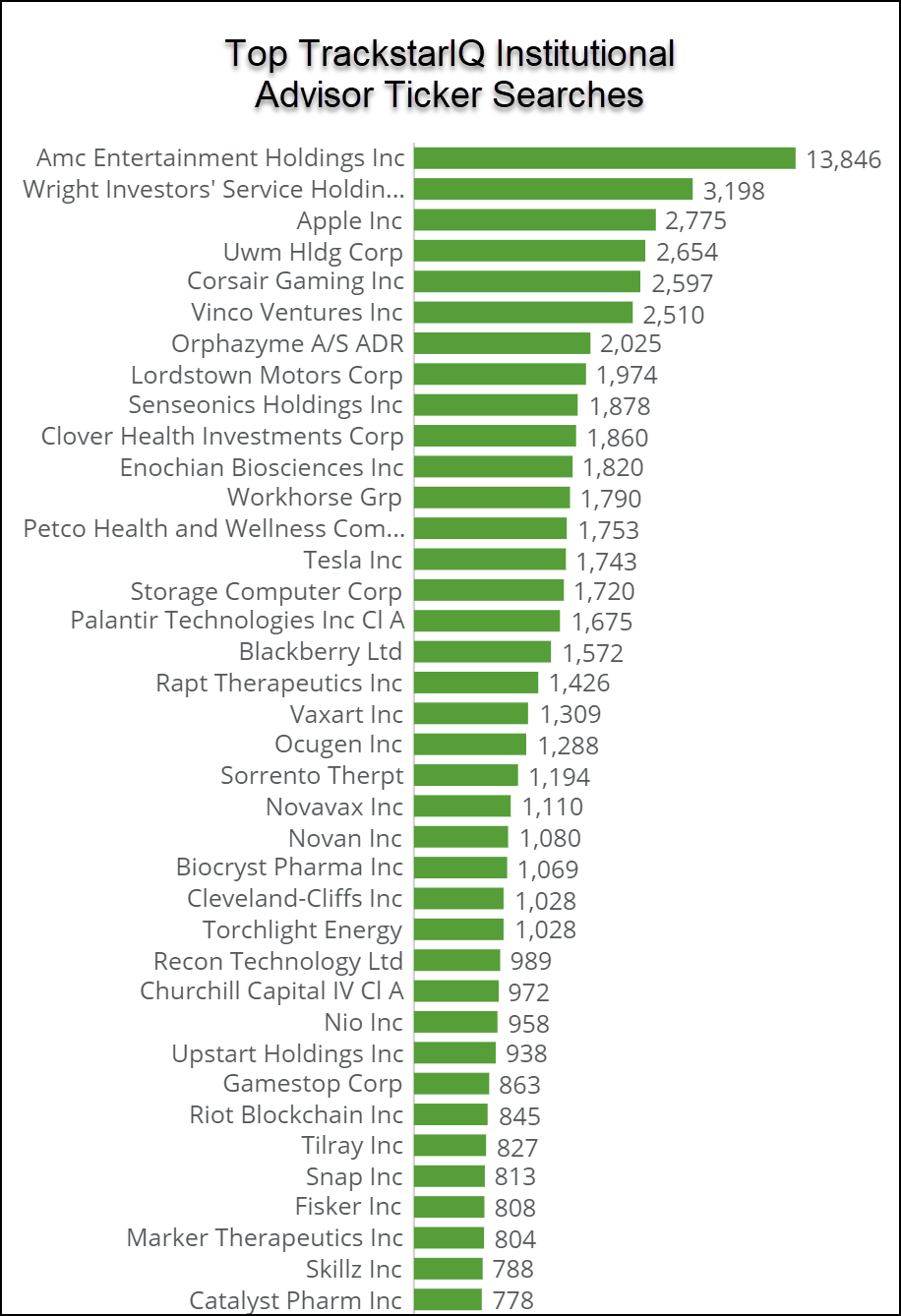

Now, most of us are familiar with U.S. Steel (X), one of the oldest companies in America.

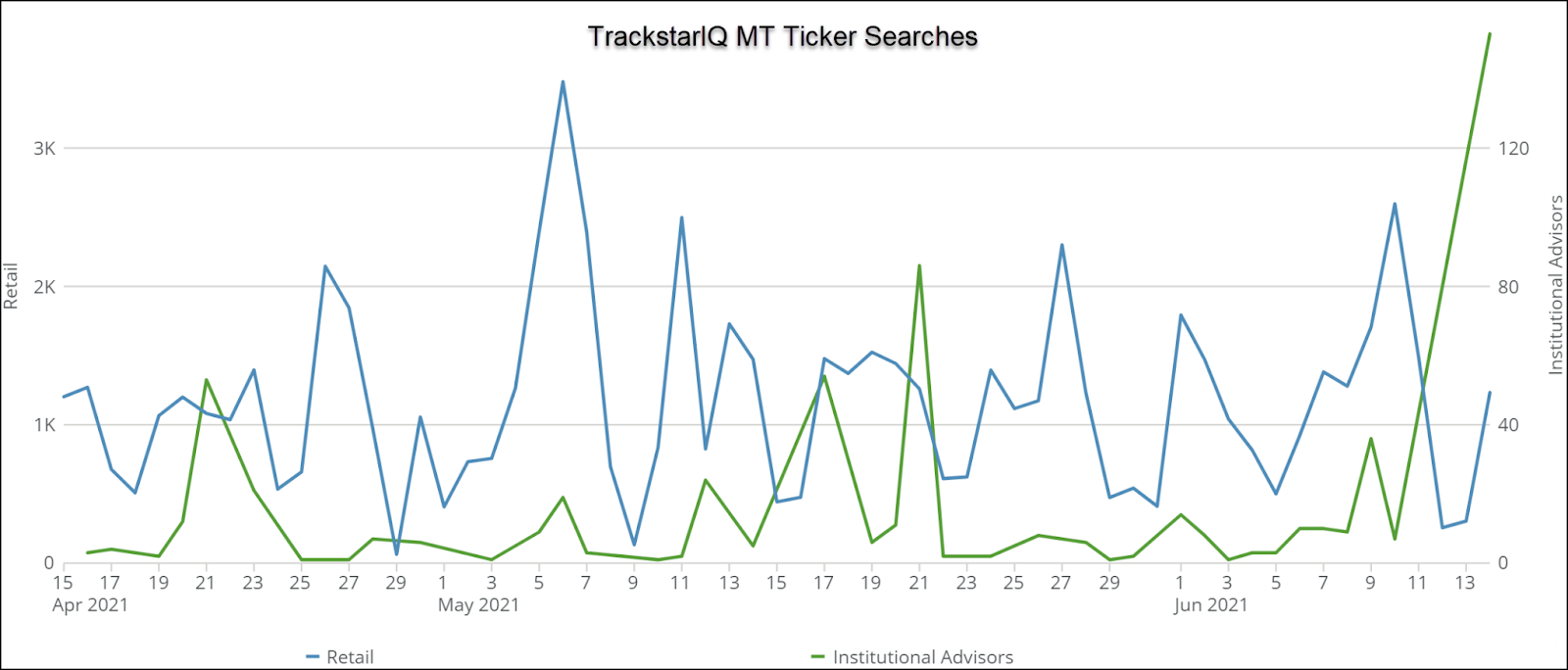

But recent TrackstarIQ institutional advisor searches point to another company…ArcelorMittal (MT), the Luxembourg-based steel and mining company.

We need to answer two questions.

First, what is the outlook for the sector?

Second, is Arcelor Mittal poised to outperform its peers.

The current situation

Steel lives and dies by broad economic growth and construction.

China propped up global demand in 2020 as advanced economies saw demand drop 12.7% during the same period.

Overall global demand for steel is expected to increase by 5.8% in 2021 and an additional 2.7% in 2022, with demand in developed economies expected to jump 8.2% and 4.2% respectively.

Interestingly, that still puts steel demand in advanced economies in 2022 below 2019 levels.

Fiscal stimulus for infrastructure from the U.S., and similar packages in the E.U., could add to demand over multiple years.

In developing countries (excluding China), demand is expected to pick up from the 7.8% drop in 2020 to 10.2% in 2021 and 5.2% in 2022.

Ironically, even with strong demand for automobiles, the semiconductor supply constraints hold back increased production and thus steel demand.

But with half the demand for steel coming from construction, automotive’s 12% of total demand won’t move the needle that much.

What Arcelor Mittal has to offer

Let’s start by defining Arcelor Mittal’s business model.

While the company primarily focuses on steel, they do some coal mining as well.

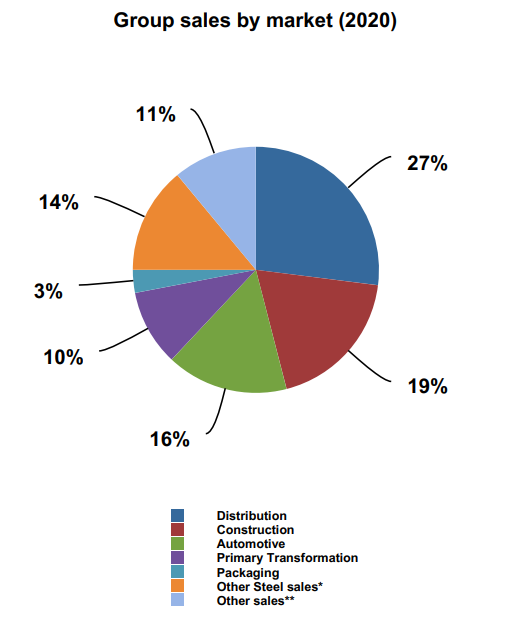

Unlike what you might expect, they have a fairly balanced revenue stream portfolio.

What’s worth noting is that many of their products do end up in China. They simply go through intermediaries (about $1.6 billion of their $53 billion).

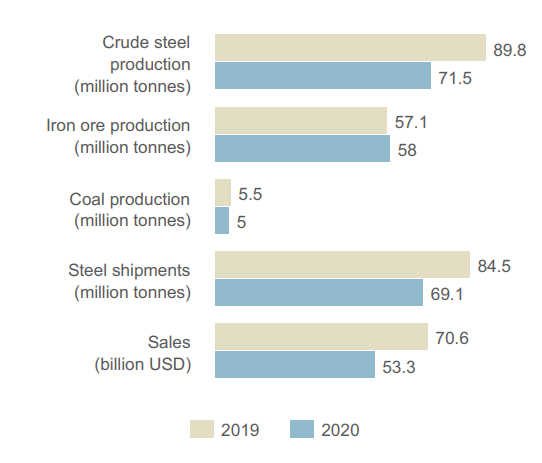

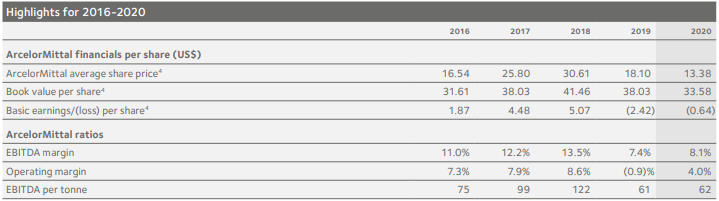

Notably, the company has focused on reducing operating expenses during the pandemic.

That’s led to lower debt levels and better margins, though well off better levels in recent years.

Nonetheless, their $1 billion fixed cost reduction program is expected to be completed by the end of this year.

But does all this make it better than its peers?

Arcelor Mittal vs its peers

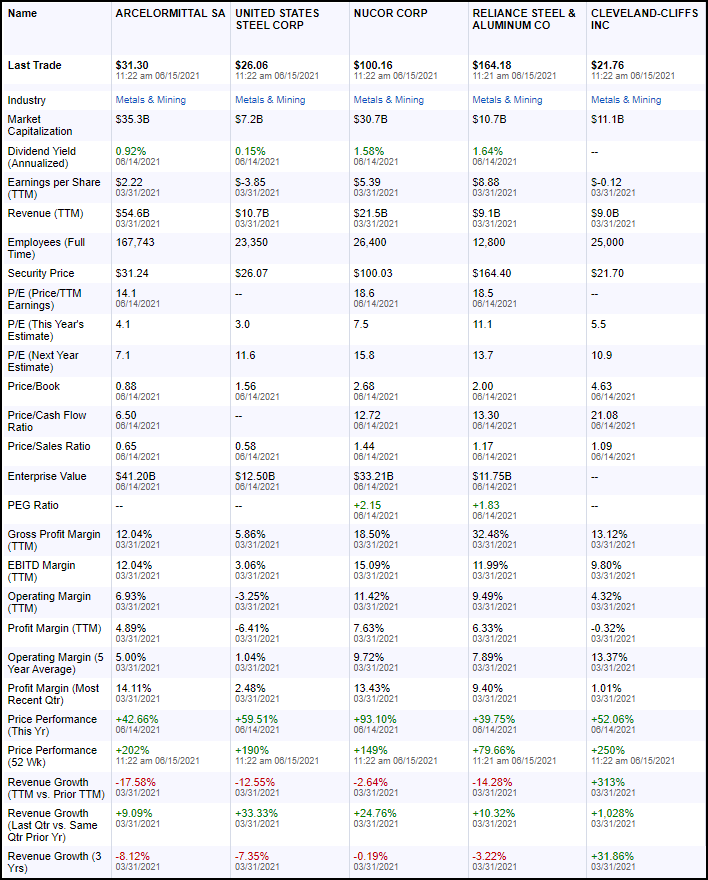

Most steel companies are incredibly cheap, trading at single-digit price-to-earnings ratios.

Arcelor Mittal happens to be one of the cheaper ones of the bunch.

Compared to its peers, Arcelor Mittal recovered earlier in 2020 which led to a slight underperformance year-to-date in share price.

Only Arcelor Mittal, Nucor, and Reliance Steel deliver positive profit margins. However, Reliance operates in slightly different verticals.

Nucor also carries less debt than Arcelor Mittal, giving it a better balance sheet.

Our hot take

Between the stocks in the sector, Nucor is a better long-term performer.

However, its better metrics show up in the higher P/E ratio.

With higher leverage, Arcelor Mittal should outperform if steel prices continue to rise and underperform if they fall.

Top-trending tickers, market-moving news alerts: Straight in your inbox!

See the pulse of the market as researched by Wall Street Elites and receive top-trending tickers and other market intelligence to inform your trades.Sign up for Wall Street Connected – our free daily newsletter that leverages our TrackstarIQ Data.

Click here to learn more