Splunk (SPLK) was one of the hot stocks of 2020.

Search volume in our TrackstarIQ data showed consistent interest in a company that hasn’t turned a profit…well…ever.

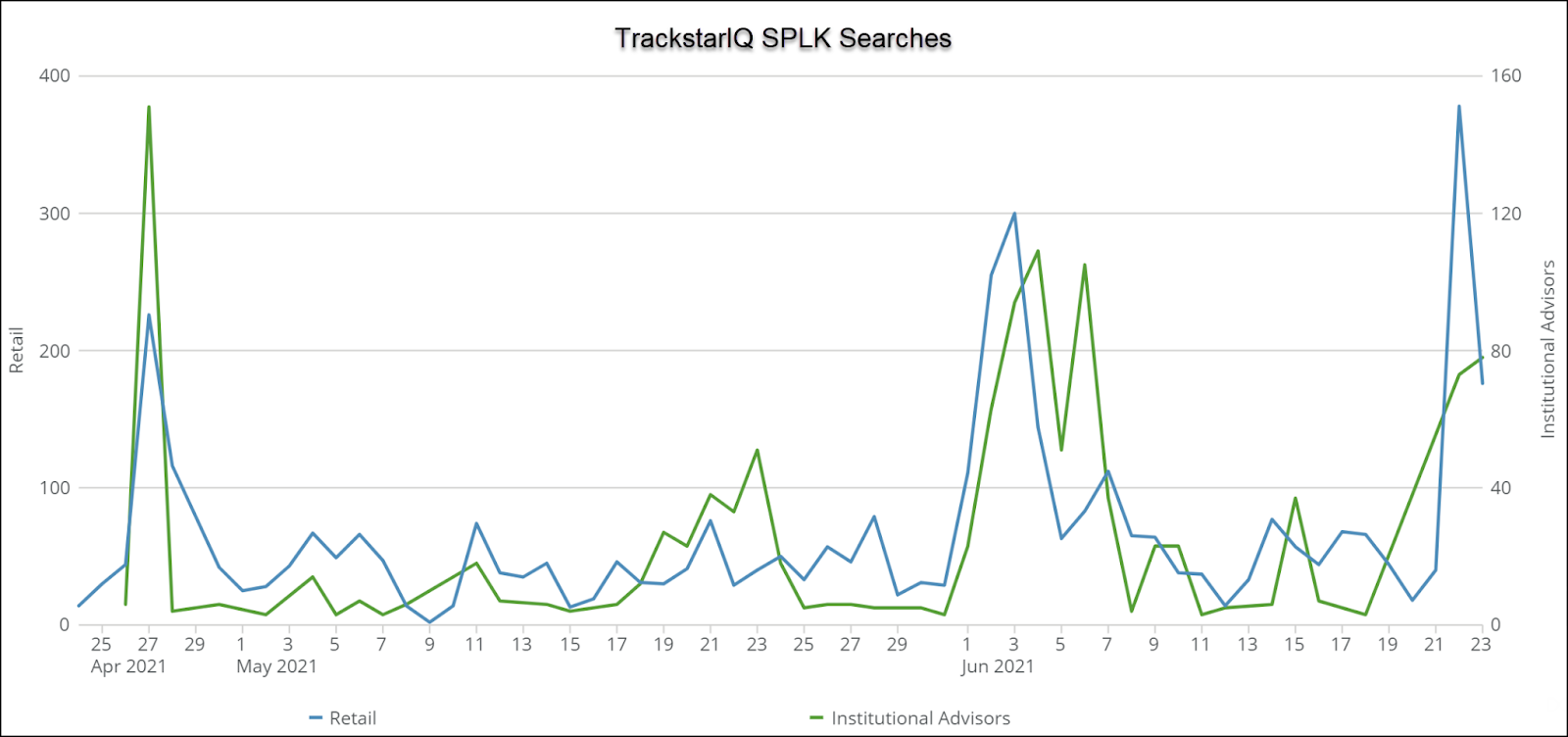

Recently, institutional search volume spiked with a focus on options surrounding the stock.

Options are leveraged bets on a company where you need to get not just the direction right, but also the timing.

So what might these big money players know that the rest of us don’t?

Breaking down Splunk

Despite its recent fame, Splunk has been publicly traded since 2012.

As the business of big data grew, so did their revenues.

Splunk’s software solutions enable businesses to aggregate, visualize, and dissect their data.

Their flagship offering, Splunk Enterprise, collects and indexes machine data, letting users explore it interactively and visualize the information.

Splunk Cloud provides the same capabilities with scalability and is their highest growth product.

Keeping with current trends, Splunk began to transition away from front-loaded sales, instead opting for subscription services.

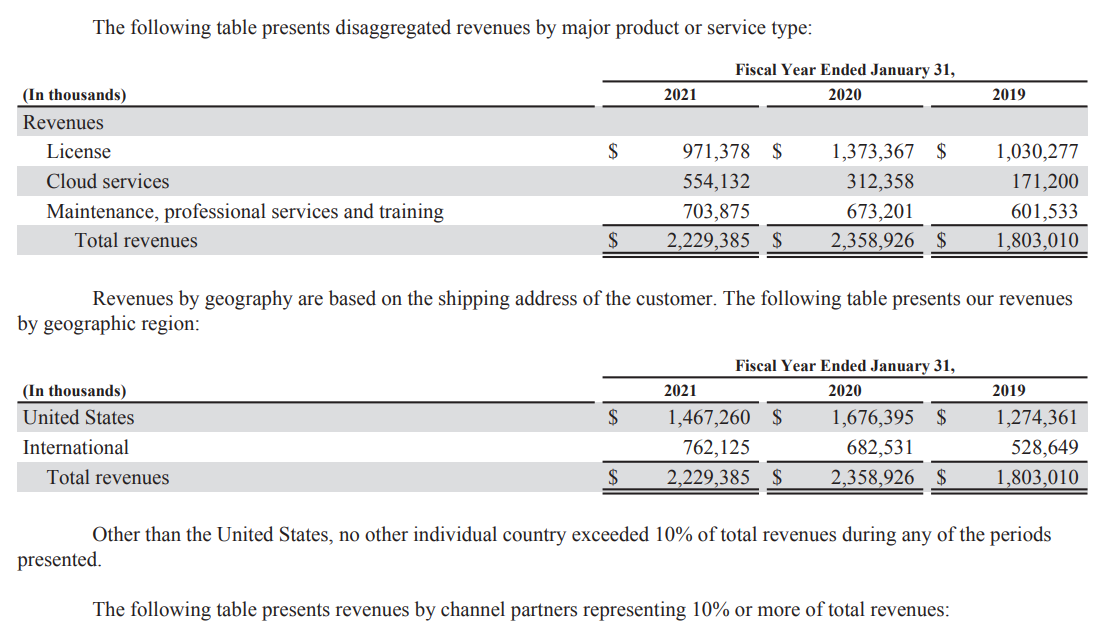

Their revenues breakdown into the following categories and geographies.

As is evident, the company continues to push harder into cloud-based.

Coupled with Covid, their enterprise license revenues took a big hit in the last fiscal year.

This shift also lowered cash flows as customers paid less up-front and more over time. Consequently, operating cash flow dropped from $296 million in 2018 to negative $288, $191, and $161 million in 2019-2021 respectively.

However, overall revenues increased 15.66% last quarter with cloud services up 72.9% from the same quarter last year.

Since its IPO, Splunk has yet to turn a profit. However, as the company pointed out in its recent financial reports if you exclude items like stock-based compensation, earnings were positive in 2020.

But, considering they took another hit in 2021 of greater size, it’s tough to call these immaterial or one-time events.

Long-term debt increased substantially in recent years, growing from nothing to $2.3 billion with $689 million due in 2023, $697 million due in 2025, and $941 million due in 2027.

How does it stack up?

With dozens of cloud companies out there each serving a slightly different niche, we compared Splunk to some familiar cloud names.

First, few high-growth cloud companies turn a profit consistently or at all. That’s why we see negative profit margins across the board.

So, how do we figure out which company is the better value?

Since gross margins are fairly similar, we look at revenue growth as it drives the majority of the value.

We know that Splunk’s sales contracted as they shifted towards a subscription-based model. That’s put their recent and three-year growth rate behind competitors.

Yet, probably one of the best metrics to use here is price to sales. That tells us the value of the stock price relative to their revenues.

And in that case, Splunk dominates the others.

Our hot take

The company is positioned well to grow over the next several years.

Their hangover from debt, stock-based incentives, and other non-cash related expenses will create earnings headwinds at least through 2022.

However, they are operating cash positive which allows them to pay down the debt.

Looking into the future, we can expect Splunk’s profits to start growing at a double-digit clip driven by the economic recovery as well as the shift to subscriptions.

Long-term, this company has a ton of potential.

Short-term, its financials are a bit opaque. But, if most are non-cash items, then this could be a nice value play at current price levels.

Top-trending tickers, market-moving news alerts: Straight in your inbox!

See the pulse of the market as researched by Wall Street Elites and receive top-trending tickers and other market intelligence to inform your trades.Sign up for Wall Street Connected – our free daily newsletter that leverages our TrackstarIQ Data.

Click here to learn more