Canadian National Railway (CNI) and Canadian Pacific Railway (CP) are in an all-out bidding war.

Their target…

Kansas City Southern (KSU).

Currently, CNI holds the top bid with $33.6 billion with an assumption of $3.8 billion in outstanding KSU debt.

But the battle is far from over.

And folks are starting to get interested.

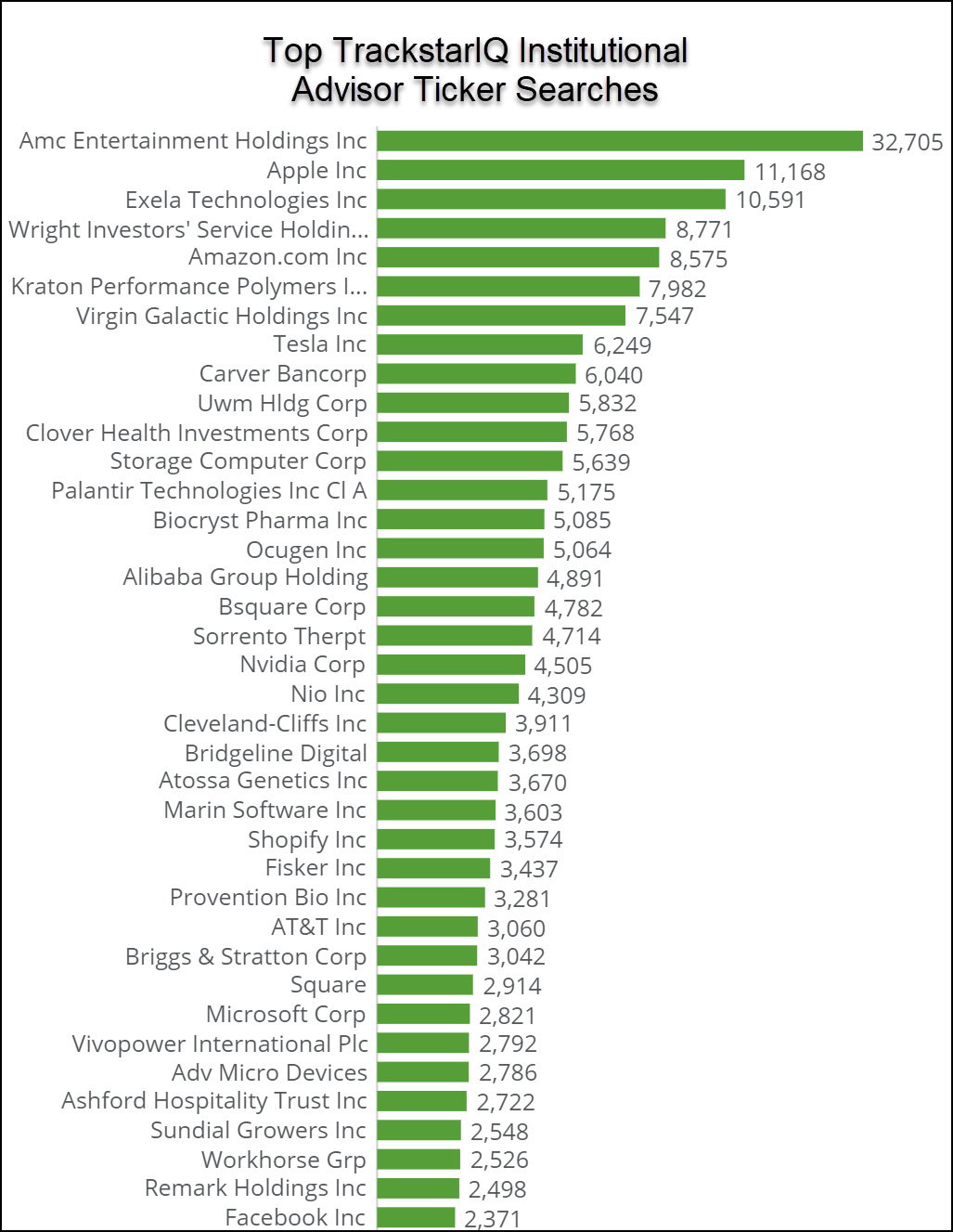

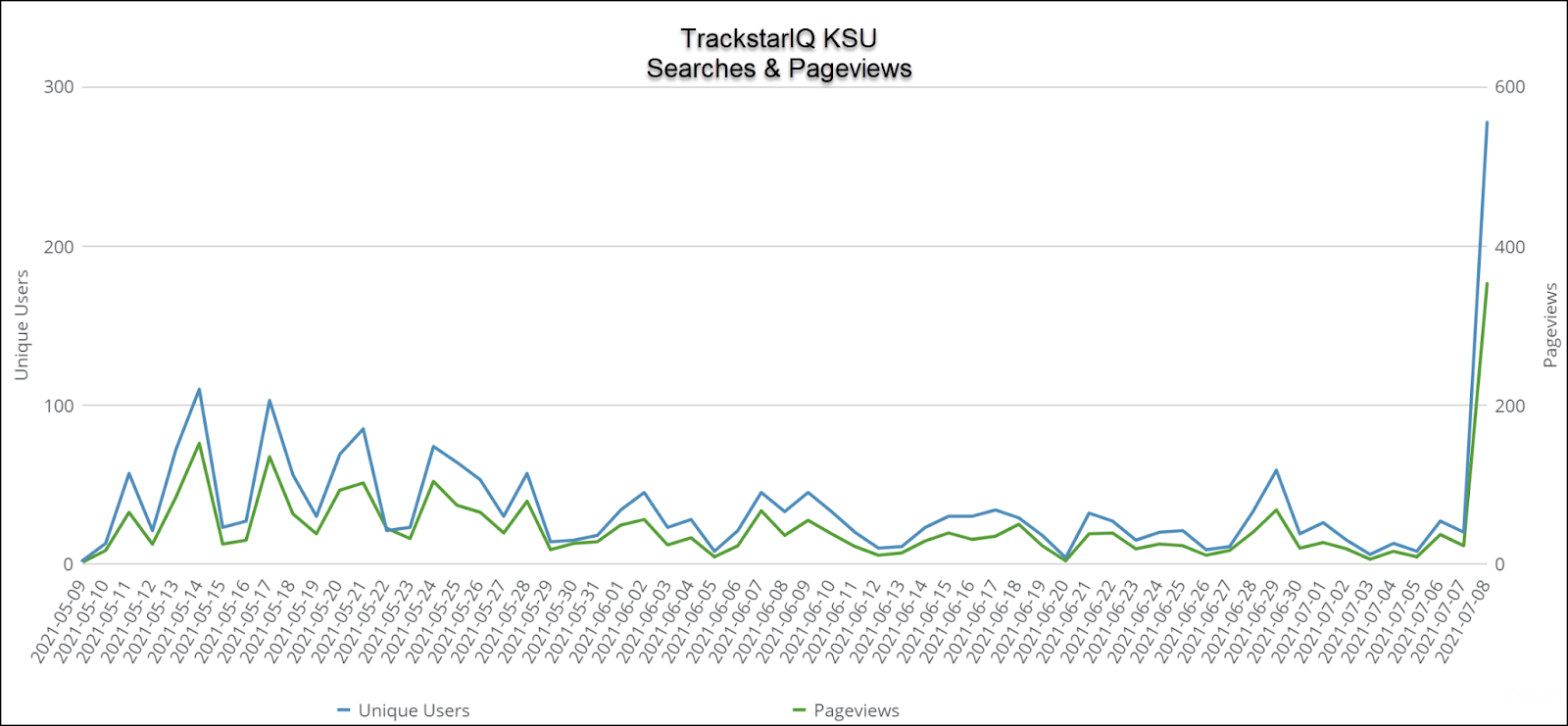

TrackstarIQ data identified a surge in interest for KSU’s stock in the last few days.

That likely comes after KSU shares took a hit on Thursday, dropping more than 7.8%.

With shares significantly cheaper than a week ago, we have to ask if there’s a play here.

KSU’s merger

As it stands, the top offer came from CNI with $33.7B as well as $200 cash per share plus 1.129 shares of CNI for each share of KSU.

Here’s some simple math to consider.

Right now KSU shares trade around $270.

CNI shares currently trade at $107.

According to CNI’s proposal, you would get $200 + (1.129 x $107) = $320.80.

That’s an arbitrage opportunity of nearly 18.5% upside potential!

Why isn’t everyone jumping on this train?

Because the deal isn’t done.

And it faces a serious uphill battle.

First, to participate in this deal, you have to lock up $200 in cash until the shares are exchanged.

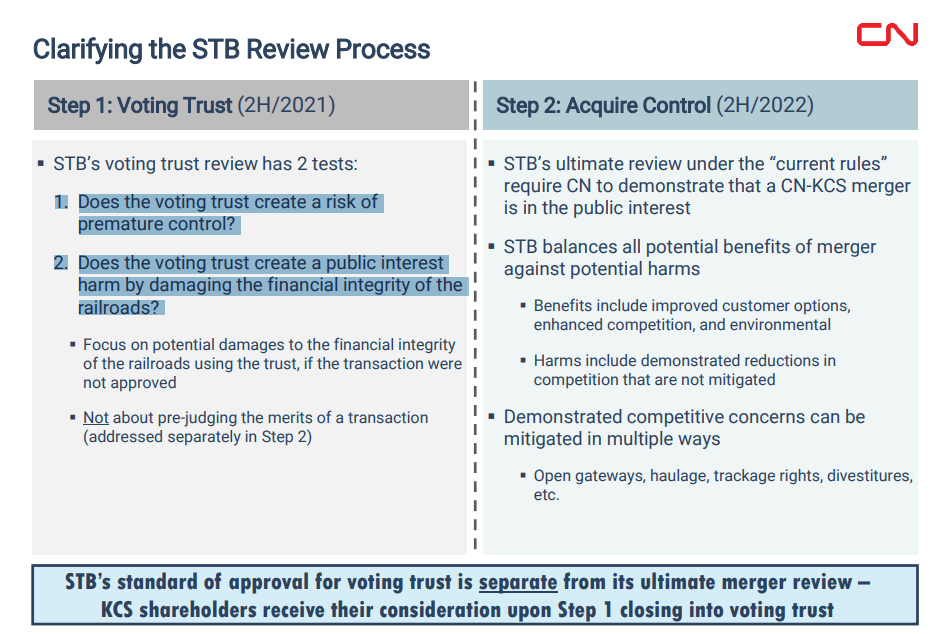

Second, this merger would create the first U.S./Canadian/Mexican railway.

That means the Surface Transportation Board (STB) needs to approve the merger.

The antitrust executive order by President Biden today could further complicate matters.

However, KSU claimed the merger would meaningfully reduce truck traffic, which plays nicely to climate change initiatives.

Then, you need KSU shareholders to approve the deal.

Lastly, the deal requires the Mexican Competition Bearue to approve the deal.

Funny enough, neither the Canadian government nor CNI’s shareholders need to approve the merger.

Of these, the STB is the biggest hurdle.

The entire process will take a minimum of 24 months. That’s a long time for a deal that ‘might’ happen to make 18.5%.

The hidden gem

CNI agreed to pay $1 billion if the voting trust fails, or $11 a share.

Additionally, CP is still pursuing the deal. If you updated their offer to account for splits, it would work out to $90 + (2.445 x CP Share price) = $271.

Third, both companies will continue to grow operations in the interim.

Like many industries, rail freight is experiencing extraordinary pricing power. Although, that is partially offset by increased fuel costs.

Nonetheless, KSU expects EPS to meet or exceed $9 per share in 2021, with 2022 at $10.50-$11.00. Plus, revenues should grow by double digits from 2020 levels.

With current share prices, that gives KSU a 2021 P/E ratio of 30x and a 2022 P/E ratio of 24.5x-25.5x

The average amongst its peers is around 22x and 19x for 2021 and 2022 respectively.

Our hot take

There’s a lot to like here. With plenty of time before the deal is done, investors could take a partial position now and wait for a deeper discount between the two stocks.

However, once the news hits the wire of KSU accepting an offer, you can expect arbitrage opportunities to shrink.

Top-trending tickers, market-moving news alerts: Straight in your inbox!

See the pulse of the market as researched by Wall Street Elites and receive top-trending tickers and other market intelligence to inform your trades.Sign up for Wall Street Connected – our free daily newsletter that leverages our TrackstarIQ Data.

Click here to learn more