Black Widow hit theatres this past weekend.

And Disney (DIS) couldn’t be happier.

The Marvel franchise owners picked up $80 million from theaters with an additional $60 million from Disney+.

Ohh, and they snagged another $78 million from international ticket sales.

The latest installment in MCU grossed the highest revenues since the pandemic hit.

This was a BIG DEAL!

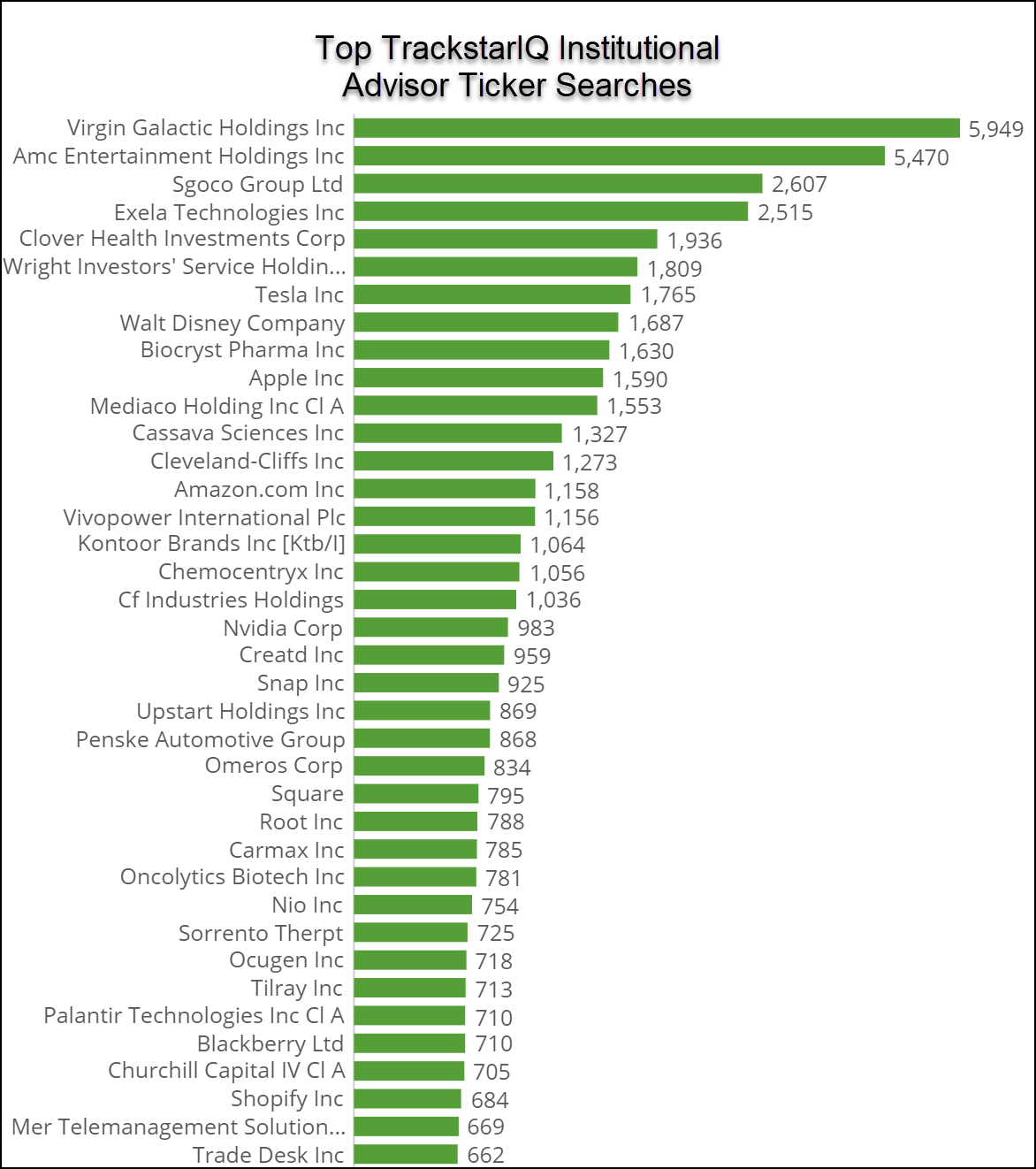

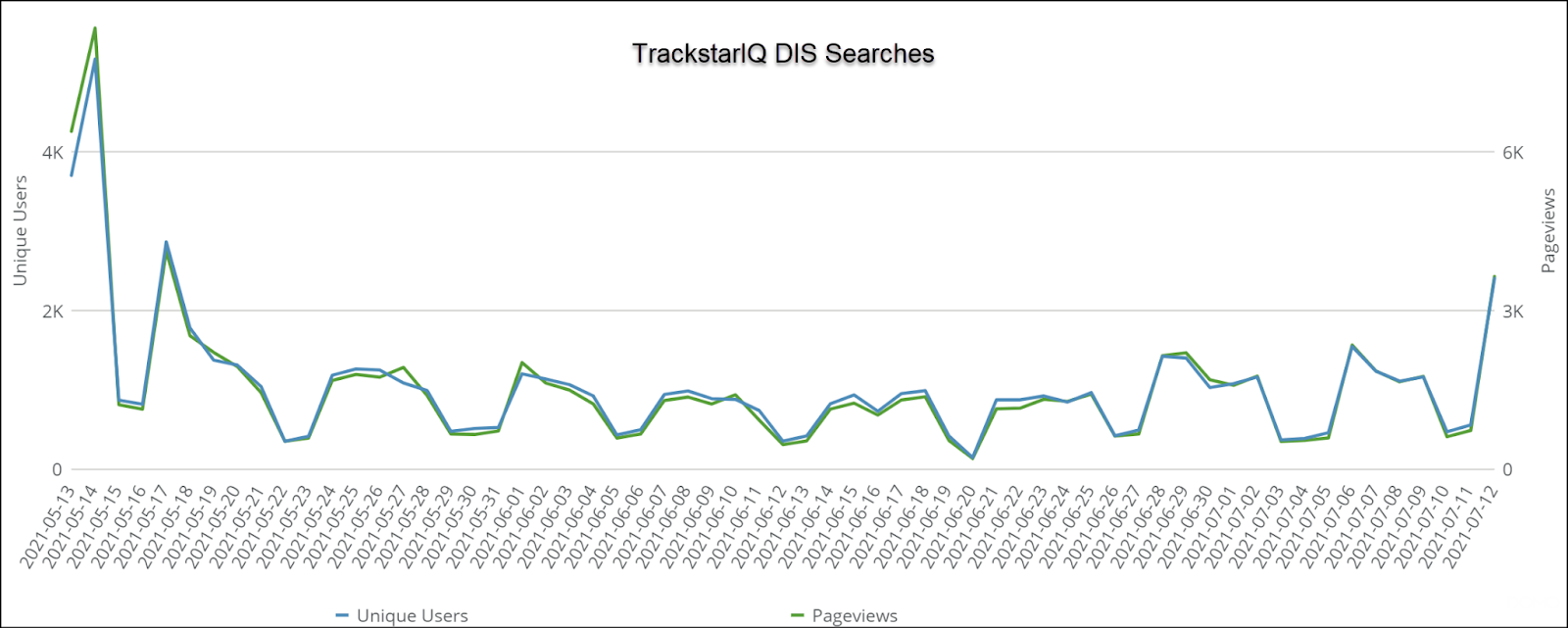

It’s no wonder that TrackstarIQ data logged a spike in searches for the mouse powerhouse.

But make no mistake.

Disney took a massive hit from the pandemic.

And recovery will take several years.

So, is this an opportunity to get in while the gettings good?

Disney & Covid

Disney’s revenue breaks down into three categories:

- Media Networks (43.4% of revenues)

- Studio Entertainment (14.7% of revenues)

- Theme Parks & Products (25.2% of revenues)

- Direct-to-consumer (25.9% of revenues)

To give you a point of reference, here’s the revenue breakdown for Comcast (CMCSA), NBC’s parent company as well as Universal Studios:

- Cable Communications (58% of revenues)

- NBCUniversal (27.1% of revenues)

- Sky direct-to-consumer content and services (17.9% of revenues)

What’s important to note here is how theme parks make up a much larger segment of Disney’s business.

In fact, in 2019 theme parks accounted for 38% of revenues and 45% of operating income!

And those took a shellacking during the pandemic.

Most parks were effectively shuttered.

Complying with guidance costs them about $1 billion a year.

Furthermore, while theatres in the U.S. are open (globally they’re barely open), traffic is nowhere near pre-pandemic levels.

At their theme parks, labor shortages force them to cap capacity below the max.

Profits have made a comeback, with the latest quarter coming in close to Q1 of 2020.

But operating income is still half what it was in 2019.

And debt increased substantially.

Disney’s outlook

Make no mistake, the company’s streaming business is a powerhouse set to drive substantial growth in the future.

The problem is the company bet big on theme park expansion right into the pandemic.

That leaves their overall results hampered looking out over the next several years.

To give you a sense of what the market thinks, shares of Disney currently trade at 79.1x this year’s P/E estimate and 37.1x next year’s.

Comcast trades at 19.8x and 15.8x respectively. Netflix (NFLX) trades at 51x and 41.5x respectively.

Heck, shares of DIS are flat on the year while CMCSA is up over 10%.

Markets price Disney at these levels because they expect the company’s core businesses to grind back to 2019 levels while their streaming services take flight.

Consider this.

EPS were $6.64, $8.36, and $5.69 in 2019, 2018, and 2017 respectively.

At the current price, that translates to a P/E of 27.5x, 21.9x, and 32.1x.

The highest prices for shares during those years were $153, $120, and $116.

Shares currently trade at $183.

Our hot take

Disney is a great company with solid growth potential.

It’s just going to take a while for them to recover.

In the meantime, like other equities, buying shares here means you’re paying a premium for a stock that has YET to catch up to pre-pandemic levels.

Call us crazy, but that doesn’t sound like thoughtful investing.

Top-trending tickers, market-moving news alerts: Straight in your inbox!

See the pulse of the market as researched by Wall Street Elites and receive top-trending tickers and other market intelligence to inform your trades.Sign up for Wall Street Connected – our free daily newsletter that leverages our TrackstarIQ Data.

Click here to learn more