Want your dog to participate in your next Cosplay?

Etsy’s here to help!

With unique crafts, vintage, and homemade items, Etsy (ETSY) carved out a niche in a highly competitive eCommerce marketplace.

And they turn a serious profit!

But should you buy it before earnings on the 14th?

That’s what we’re here to find out.

Etsy managed to go up against titans like eBay (EBAY) and Amazon (AMZN) and didn’t just survive…it thrived.

Just a few short years ago, the company’s market cap sat around $5 billion.

Today, they’ve turned into a juggernaut at over $23 billion.

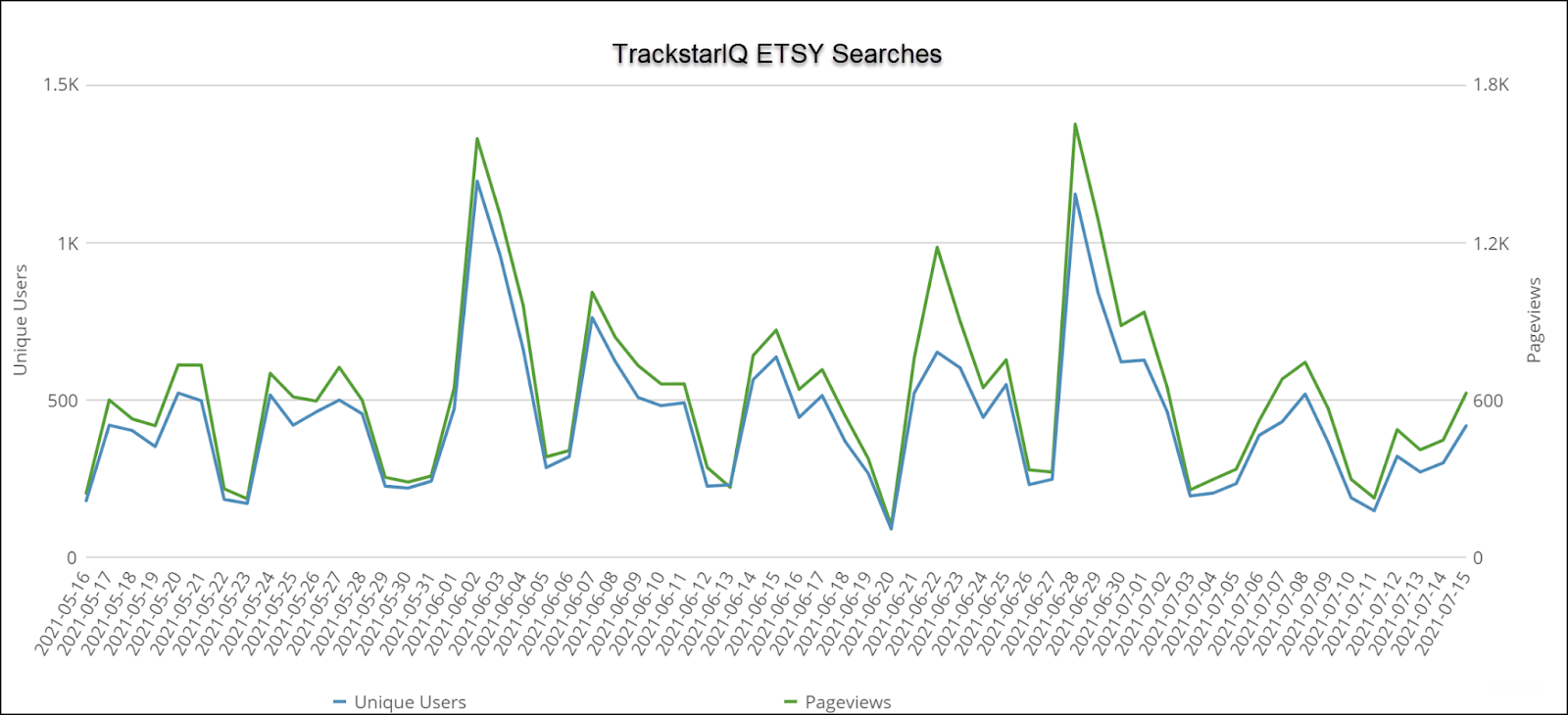

And it’s one of the most consistently searched online commerce stocks according to our TrackstarIQ data.

At over $180 a share, and a nearly 75% return in the last year, we wanted to know whether it was worth a buy here and now.

Etsy expands

In recent quarters, Etsy decided to expand its business through strategic acquisitions.

The company paid $1.6 billion for the fashion resale marketplace Depop which has offices in the U.S., U.K., and Italy.

In 2020, Depop grew a100% in GMS (gross merchandise sales – the value of items sold on the platform) to $650 million while doubling revenue to $70 million.

Etsy hopes Depop will extend their reach into the high frequency apparently sector, specifically the fast-growing resale space.

The only downside is they expect Depop to dilute their adjusted EBITDA margins.

Back in 2019, they acquired Reverb, a marketplace focused on musical instruments, for $270 million.

In Q1, Reverb saw ~50% growth in GMS.

Fine financials

Unlike many tech startups, Etsy turns a pretty solid profit.

The competitor comparison below pulls together several similar companies.

While no one directly competes with Etsy, these names give us a decent range to evaluate aspects of their business.

We can look at eBay as a future state.

Poshmark (POSH) deals with online clothing resale.

Fiverr (FVRR) manages freelance contracts.

Wayfair (W) operates an online furniture marketplace.

First, let’s look at eBay and Etsy.

eBay has been around a long while. And their revenues are about 5x higher than Etsy’s.

What’s interesting is how the market only values eBay at 18x earnings this year and 15.2x next year’s.

That’s pretty odd considering eBay’s consistent growth and profitability.

However, it says less about Etsy and more about eBay.

When we turn to the other three companies, we get a better sense of Etsy’s profitability.

Poshmark and Fiverr both have yet to turn a profit.

Wayfair just began to turn one this year.

Etsy has been profitable since 2017. And it hasn’t sacrificed growth.

Our hot take

Etsy may look expensive here at 48x forward earnings given the S&P 500 is at 22x.

However, looking at the current S&P 500 p/e ratio of 46x, Etsy’s 52x doesn’t look too shabby.

Share price is volatile here. So, if you like the company, dollar cost averaging may be the way to go.

Top-trending tickers, market-moving news alerts: Straight in your inbox!

See the pulse of the market as researched by Wall Street Elites and receive top-trending tickers and other market intelligence to inform your trades.Sign up for Wall Street Connected – our free daily newsletter that leverages our TrackstarIQ Data.

Click here to learn more