Market’s reacted to Netgear’s (NTGR) earnings in a puzzling way.

The stock was already trading at basement-level prices.

Driven by lockdowns revenues soared over the past year, well above 2019 levels.

However, the company said second-half revenues would land near $622 million, nearly 16.5% below the second half of 2020.

Specifically for Q3, CFO Bryan Murray told markets to expect $285 – $300 million compared to $265.9 and $378.1 million for the same period in 2019 and 2020 respectively.

All this sounds terrible.

But it discounts their changing business model and financial standing.

Right now, Netgear trades at a price-to-earnings ratio of 12.27x and a forward P/E ratio of 16.28x.

Does that mean there’s value? Or, does it mean markets are worried about their prospects?

We aim to find out.

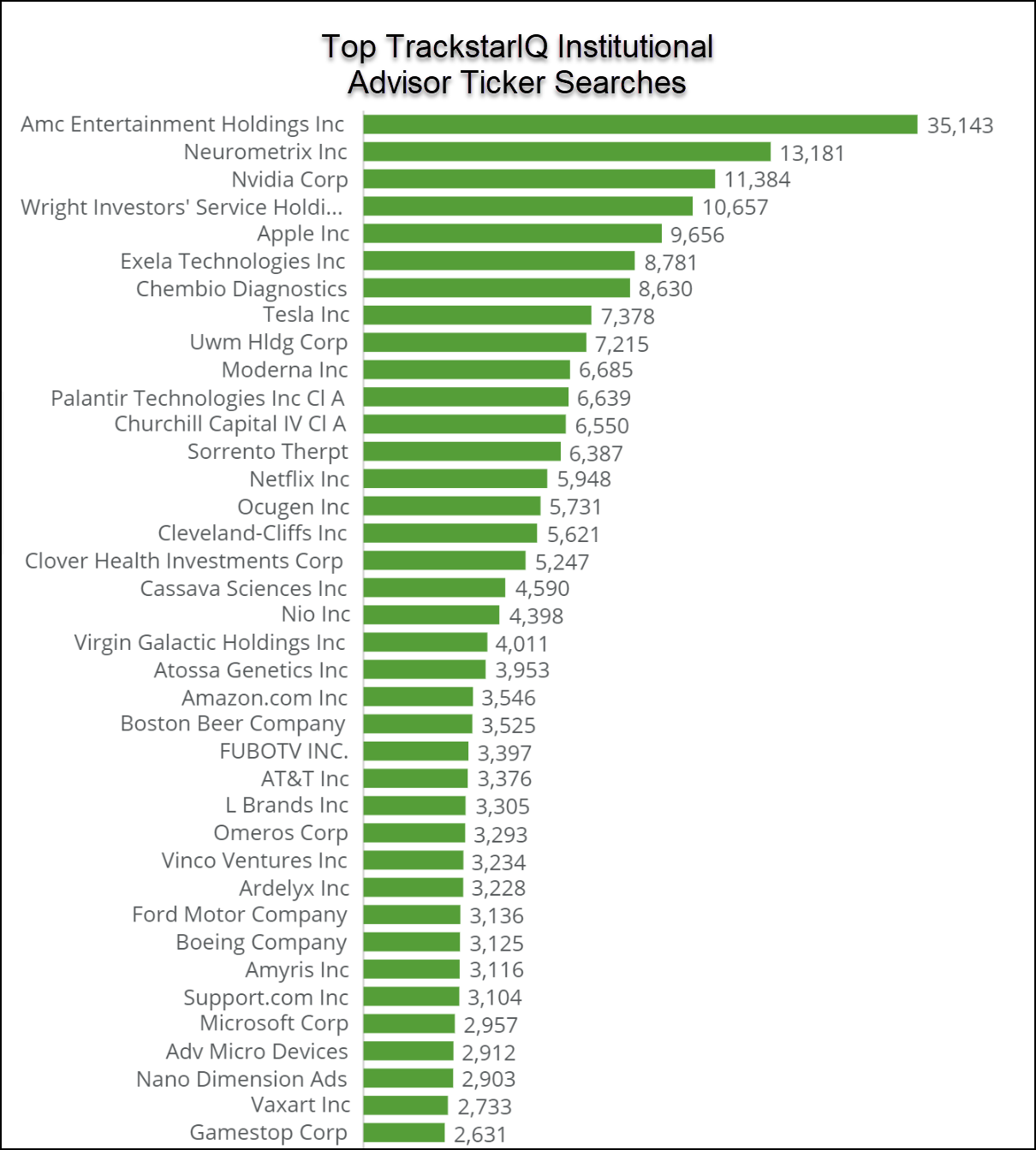

Especially since our TrackstarIQ data put it in the top 5 ticker searches yesterday.

Netgear’s business

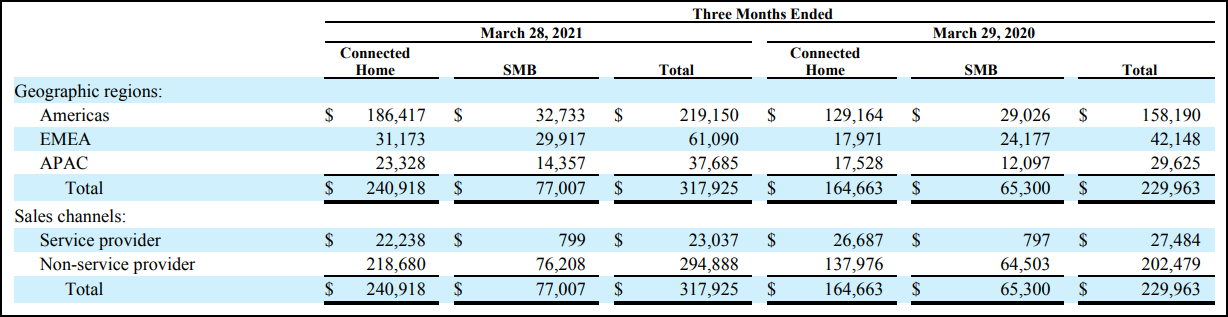

Netgear operates under two main segments: connected home and small & medium business (SMB).

The connected home segment focuses on consumers and WiFi networking solutions like mesh, range extenders, and hotspots.

At the other end, Netgear’s SMB consists of technology aimed at commercial players such as ethernet switches, cloud or stand alone access points, and internet security.

Their revenues for the most recent quarter breakdown as follows:

Like many of its peers, Netgear began to aggressively develop and push subscription services.

In Q2 alone they added 33,000 subscribers.

By the end of 2021, the company expects to have 650,000.

This is a key growth category for them.

A deep value play?

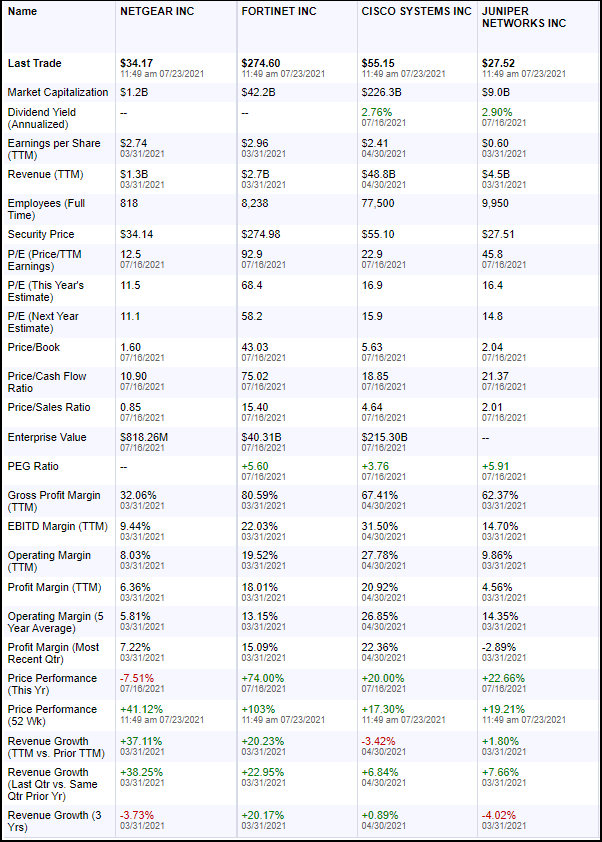

The best way to understand Netgear is through a competitor comparison.

Netgear has terrible gross margins and has for a long time. That’s to be expected when you only do hardware and not software.

When we get down to the operating margin, they are at the bottom again (and have been for a while).

Recent revenue numbers aren’t useful because of the pandemic.

But here’s what you need to know.

Netgear’s revenues have essentially gone nowhere for a decade. However, they spun off Arlo at the end of 2018 which cut around a third of revenues.

When you account for that, there has been some growth. But over a decade, it’s anemic at best.

Still, the company has a solid balance sheet it can leverage to make investments.

Our hot take

This is a tough one.

Shares are cheap if the company can truly grow its topline.

Otherwise, they’re probably fairly valued.

But, the price of a stock should consider the current fair value and then add a premium for the possibility of growth.

And that’s the piece we think is missing.

Top-trending tickers, market-moving news alerts: Straight in your inbox!

See the pulse of the market as researched by Wall Street Elites and receive top-trending tickers and other market intelligence to inform your trades.Sign up for Wall Street Connected – our free daily newsletter that leverages our TrackstarIQ Data.

Click here to learn more