United Parcel Service (UPS) shows up at our home at least once a day with an Amazon package.

This daily reminder speaks to the scope of UPS’s business.

Yet, when the company beat both earnings and revenue expectations, the stock cratered.

But did this create a unique buying opportunity?

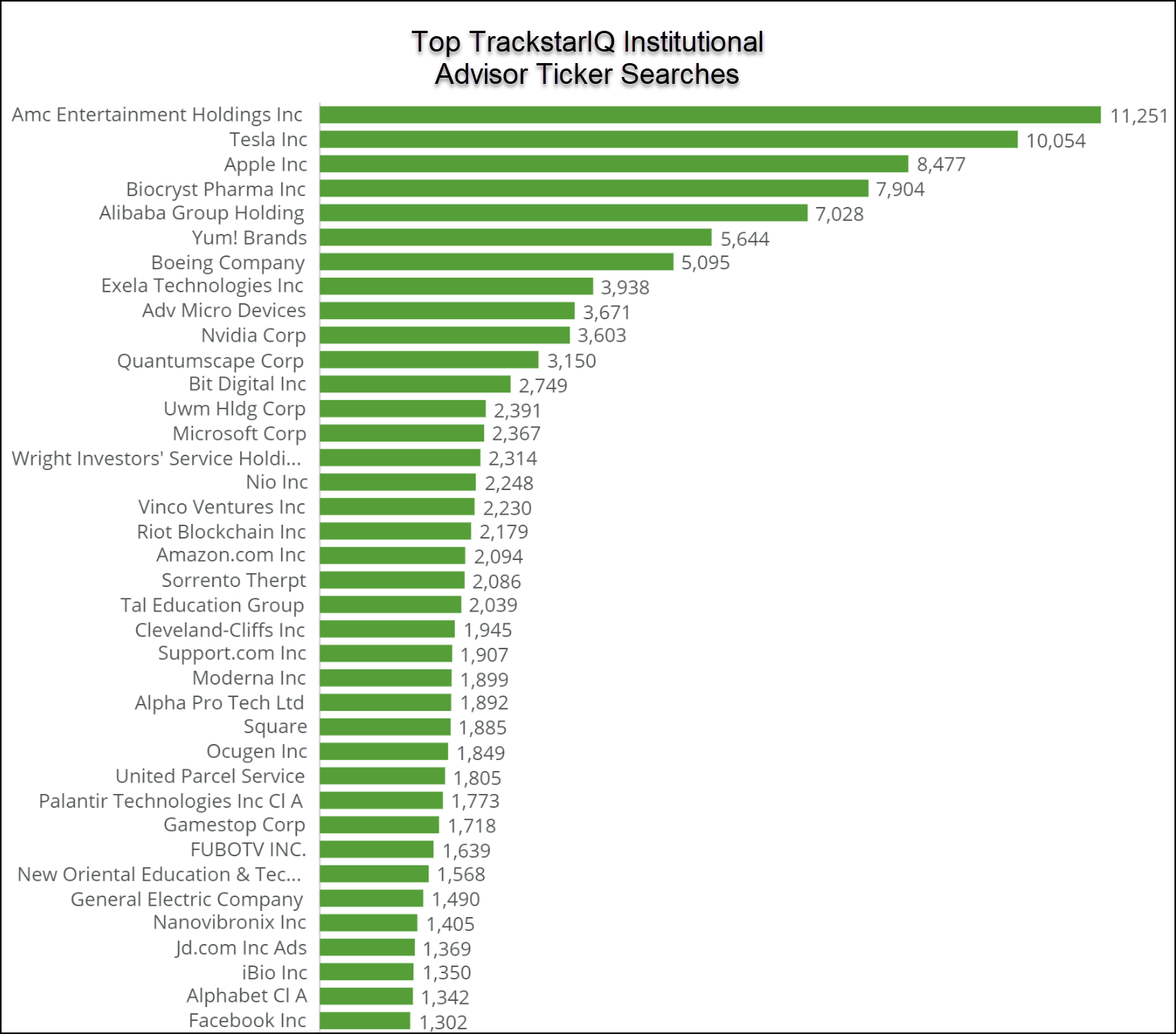

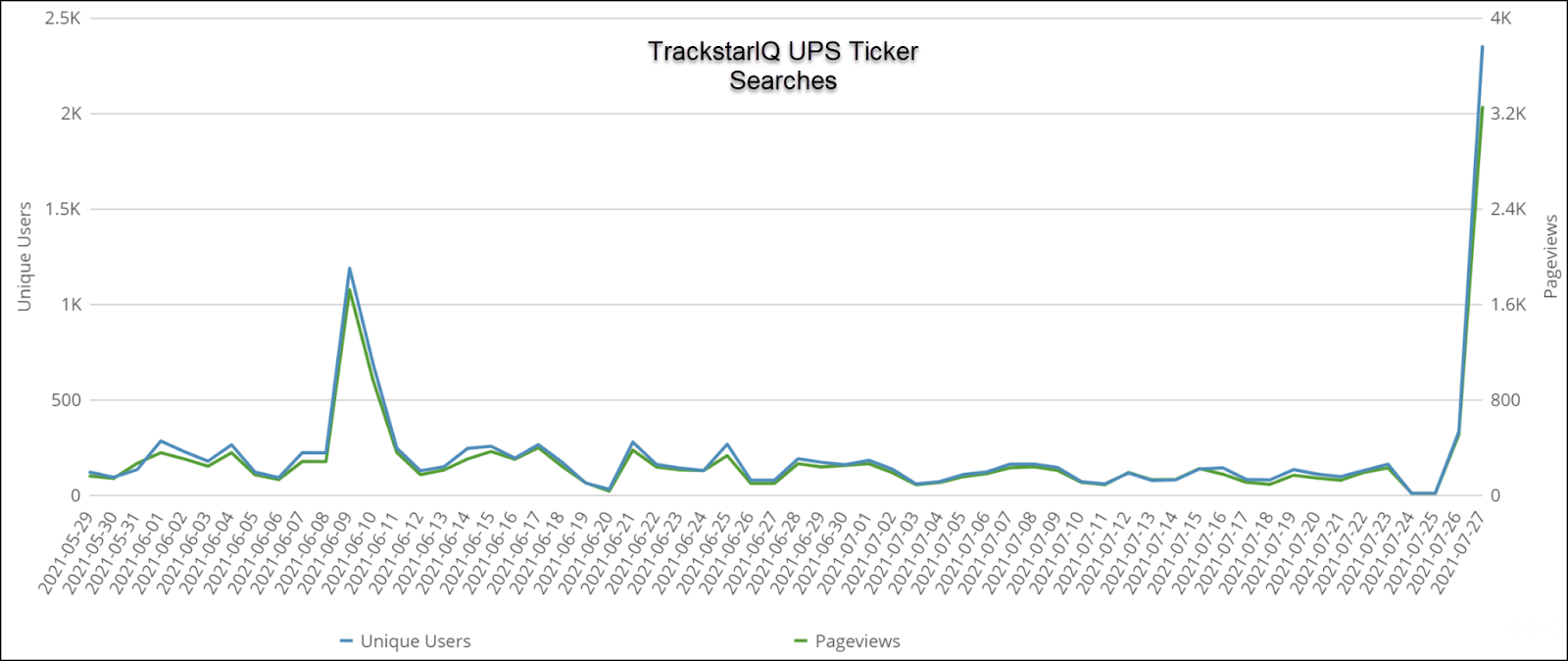

The stock was one of the top 5 ticker searches in our TrackstarIQ data the day of its earnings release.

So clearly, many folks were interested.

Analyzing their results

UPS operates three distinct segments:

- Domestic operations (63.2% of revenue)

- International operations (18.8% of revenue)

- Supply chain and freight (17.9% of revenue)

The first two are self-explanatory.

The supply chain and freight segment encompass logistics, excess value package insurance, and freight ancillary services such as brokerage.

What you may not realize is one of their biggest expenditures isn’t fuel. It’s purchased transportation.

You see, UPS hires out many third party carriers to deliver its freight.

In fact, it accounts for nearly 20% of their revenues.

Compensation and benefits are their biggest expense at just above 48% of revenue.

The company benefited substantially from the lockdowns which led to a shift in consumer habits.

That kicked off 14.22% YOY growth, nearly double the growth of any other year in the last decade.

UPS spent the last five years building out its footprint.

Now, management is shifting focus to cost efficiencies and better performance which led directly to some of their best EPS in the last two quarters.

So why the selloff?

Not everything is roses.

Those Amazon packages I spoke of?

Those account for 13.3% of 2020’s revenues.

Amazon decided it wanted to build out its own delivery network.

That doesn’t mean UPS will lose them entirely. But it will be a hit to their top line.

Additionally, UPS isn’t set up well to manage same day deliveries, a growing trend in the market. However, the problem isn’t unique to UPS.

But the big reason for the drop was U.S. delivery volume.

Investors are concerned that the boost from Covid won’t last.

Although Q1 and Q2 revenue this year came in higher than 2020, the company said U.S. ground deliveries dropped 3% from a year ago as total volume in the U.S. dropped by 4%.

B2C volume was down 15.8% while B2B increased by 25.7%, highlighting the shift away from consumer deliveries towards businesses.

The bright spot was they saw revenue per package rose by 13%.

However, CEO Carol Tome said she expected margins to ease in the second half of the year which is seasonal.

Additionally, she forecast the company would reach $102 billion in revenues, 20% higher than 2020, by 2023 with a 12% operating margin.

So is there value?

That depends.

The company trades at a 17.8 and a 17.07x forward P/E ratio.

That’s pretty cheap compared to sector medians of 23.21x and 20.37x respectively.

The company also pays a nice 2% dividend.

Yet, they hit a 12.1% and 13.1% operating margin in Q1 and Q2.

Based on the CEO’s comments, that’s likely to come in lower in the second half, which typically drops around 1%-2%.

Our hot take

The stock is certainly cheap compared to the market and historical standards.

UPS probably has a rough second half awaiting them.

And it’s tough to say how much margins will contract.

But, if you look past that to 2022 and 2023, there’s a lot to like.

Top-trending tickers, market-moving news alerts: Straight in your inbox!

See the pulse of the market as researched by Wall Street Elites and receive top-trending tickers and other market intelligence to inform your trades.Sign up for Wall Street Connected – our free daily newsletter that leverages our TrackstarIQ Data.

Click here to learn more