Unless you’ve been hiding under a rock, you know China’s swinging the hammer on tech companies.

From Didi (DIDI) to Tal Education (TAL), regulators have managed to destroy more than $1.2 trillion in market value.

But that pushed some of these companies to bargain basement prices.

Chief among them is Alibaba (BABA).

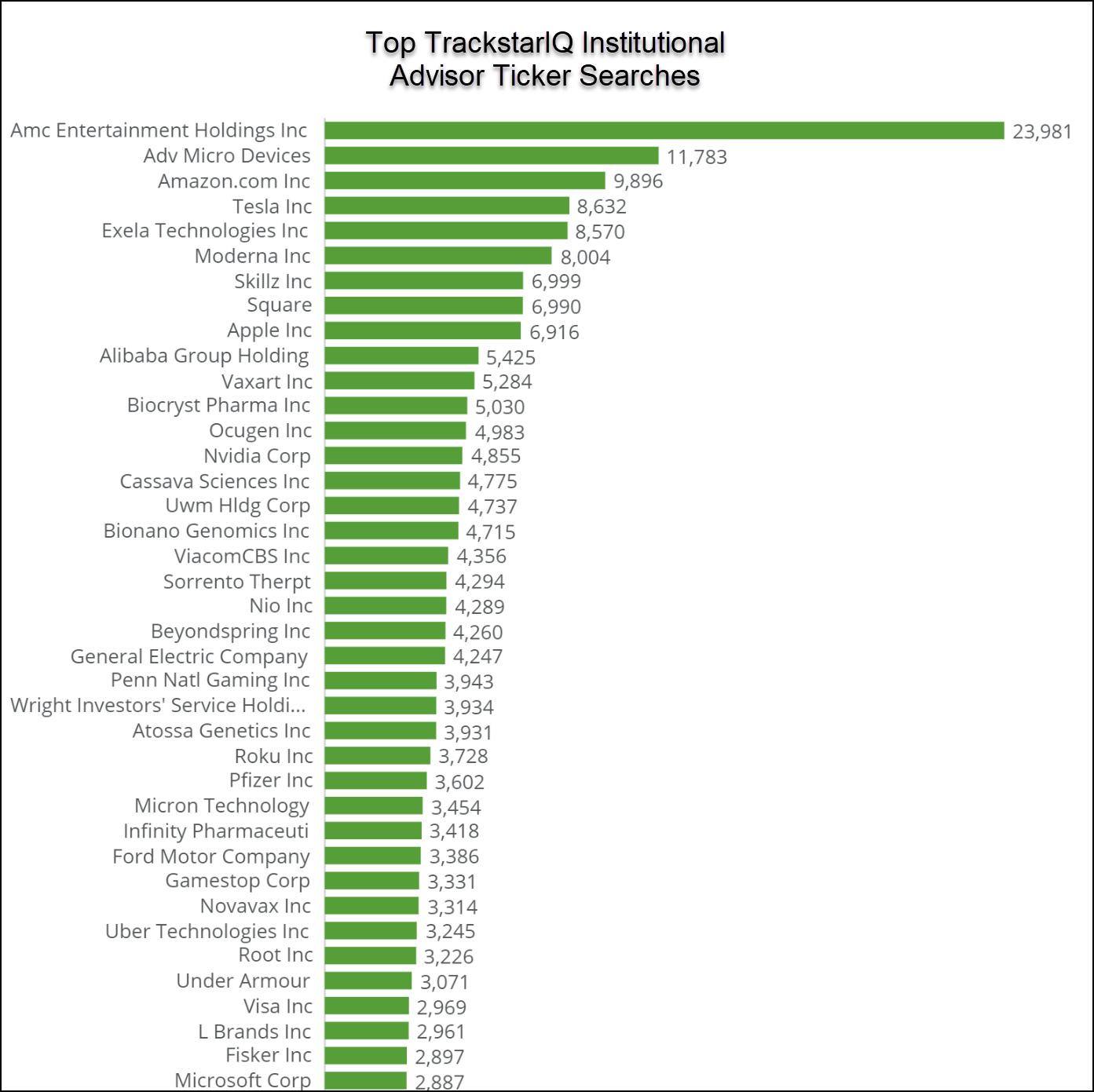

For the last several weeks, it’s topped our Trackstar search data.

Which means someone is definitely interested.

The question is whether this is the right time to step in.

Alibaba’s basics

Amazon is the big kid on the block.

But Alibaba is trying to mark their own path.

As China’s largest e-commerce giant, the company is represented by three segments:

- Alibaba.com – Kind of like eBay, Alibaba acts as the middleman between buyers and sellers, though typically on a commercial scale. If you need a supplier of 1,000 iPhone cases, you’ve come to the right spot.

- Taobao – A fee-free marketplace for retail. Instead, sellers pay to rank higher in the internal search engine as well as advertising. Here you’ll find smaller merchants.

- Tmall – The site you go to for name brands like Gap, Nike, and Apple.

Corporate risks

It all started back when the regulators put the kibosh on Ant Pay going public.

Shortly thereafter, Jack Ma disappeared from public life amid rumors of something nefarious.

Luckily, he was just fine.

But the Chinese government is wary of any data that could reveal personal information to entities outside China.

Many analysts believe that China’s crackdown aims to limit information about government and important officials as well as extend their influence over Hong Kong.

Most Americans don’t realize it, but Alibaba, and in fact most Chinese big tech companies we can invest in are on the Hong Kong exchange.

Their crackdown was fierce. But it also seems to be moving on. It doesn’t appear that they have any reason to come back to Alibaba after they already slapped them with a $2.8 billion fine.

Lots of value

It should be noted that because of the political risks, investors place a discount on Chinese companies.

That said, shares are off more than 38% from their all-time highs and priced below where they ended 2019.

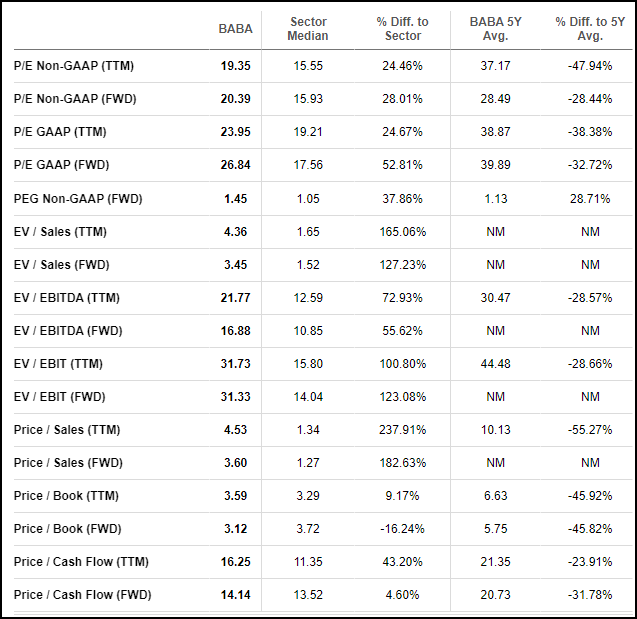

The below table summarizes many of the key valuation measures.

Note: We often find different measures depending on the site you pull data from because of how foreign companies report.

Generally speaking, Alibaba is quite cheap given its growth.

Every year they manage to add a blistering 40% to their top line. However, they lowered guidance on their core commerce business from 41% to 30% for FY 2022.

Generally speaking, we should expect a CAGR of around 16% on the net income over the next 5 years.

Translated to a forward P/E ratio, we’d land at around 1.5x which is fairly cheap.

Our hot take

The value in Alibaba is definitely there, especially compared to the rest of the market.

Unless the Chinese government comes back for seconds and thirds, it’s unlikely we’ll see ongoing fines and penalties levied on Alibaba.

Top-trending tickers, market-moving news alerts: Straight in your inbox!

See the pulse of the market as researched by Wall Street Elites and receive top-trending tickers and other market intelligence to inform your trades.Sign up for Wall Street Connected – our free daily newsletter that leverages our TrackstarIQ Data.

Click here to learn more