Few retailers weathered the pandemic better than Foot Locker (FL).

Unlike most other stocks, Footlocker is well below its all-time highs and exhibits significant value.

The question is whether it’s a trap.

We don’t think so.

Q2 of 2020 was the only quarter during the Pandemic where the company lost money.

But they quickly bounced back and then some the following quarter.

Interest surged after their recent acquisition of California shoe store chain WSS for $750 million and Japanese streetwear brand Atmos for $360 million.

The move comes at a time when retailers push more sales online and away from brick-and-mortar stores.

And despite the market’s pricing, we think this stock has enormous potential.

Shoes that can’t lose

Foot Locker doesn’t run a complicated business.

They sell shoes and apparel through 2,998 retail stores in 27 countries from the U.S. to Asia along with ownership of the Champs Sports brand.

Digital sales grew 65% in 2020 to over $2 billion. Yet, it still only represents ~30% of their total sales.

That’s why the acquisition of Atmos, where 60% of sales are online, makes a ton of sense.

WSS is a bit different with its neighborhood-based store models.

Bulls vs bears

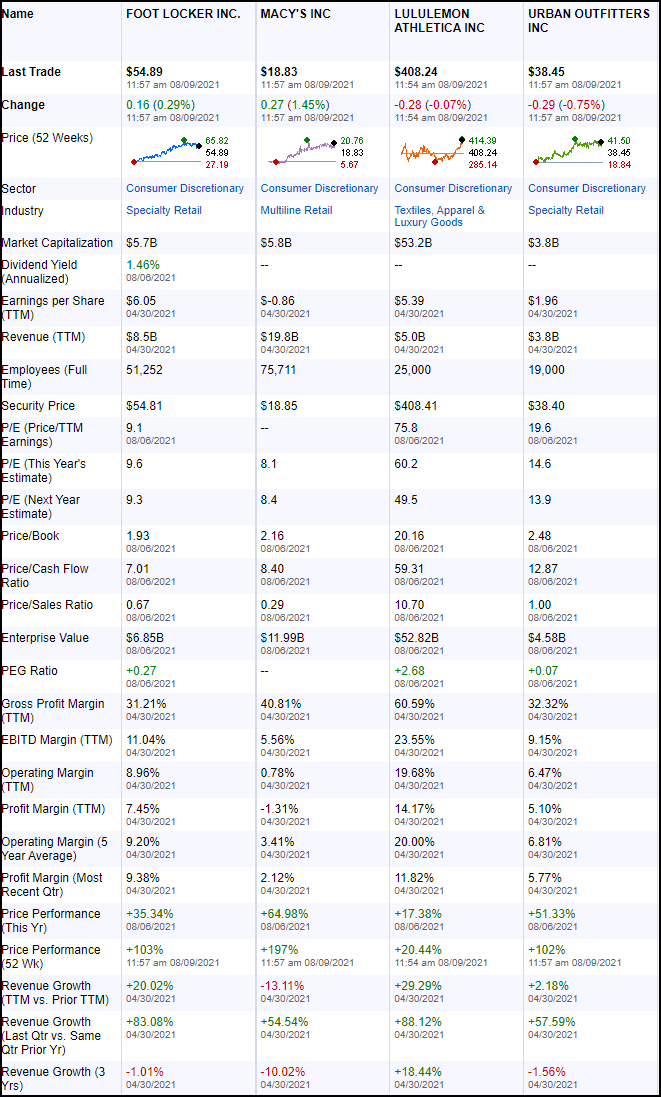

Bulls love the exceptional value.

Currently, shares trade at 9.1x earnings compared to a sector median of 15x.

Looking at the comparison, we can see that retailers aren’t getting any love. Only Lululemon Athletica garners a premium.

Macy’s may look cheaper than Foot Locker, yet its margins are much worse not to mention the sales decline the company experienced long before the pandemic.

Although Foot Locker’s margins declined the last few years, the company’s initiatives to control inventory and increase supply chain efficiency have yielded promising results.

Bears are quick to point out that despite a strong Q1, Footlocker has yet to show sustained revenue growth.

Additionally, their heavy physical footprint exposes them to Covid lockdowns and general mall traffic declines.

Our hot take

Over the last 10 years, Foot Locker has seen the following ranges:

- Price to earnings (P/E) of 8.4x to 17.6x

- Price to sales (P/S) of 0.6x to 1.2x

- Price to cash flow of 5.9x to 13.4x

Here are its current measures:

- P/E of 9.1x

- P/S of 0.67x

- Price to cash flow of 7.01x

There’s no denying shares trade at the discount end of the range.

The cash generated in one year could effectively pay off all their liabilities, giving them a robust balance sheet.

Management already indicated a willingness to acquire more companies, giving them a real opportunity to grow both earnings and revenues.

If shares price even at 13x earnings, that gives shares a 36% upside without breaking a sweat.

Top-trending tickers, market-moving news alerts: Straight in your inbox!

See the pulse of the market as researched by Wall Street Elites and receive top-trending tickers and other market intelligence to inform your trades.Sign up for Wall Street Connected – our free daily newsletter that leverages our TrackstarIQ Data.

Click here to learn more