Every stock related to home buying should be flying now right?

One stock is particularly intriguing – Zillow (ZG).

The site that only used to do home listings has taken on another challenge – buying and selling homes.

And it’s led to some unsteady results.

Last quarter, the company missed on earnings by a wide margin while beating on revenues which sent shares plunging the following day.

But all might not be lost for Zillow fans.

Zillow’s new model

Back in 2014, Zillow acquired rival Trulia, giving it the 1st and 3rd most visited real estate websites by traffic.

For years, the company focused on expanding its audience on Zillow.com, allowing them to overtake rival Realtor.com.

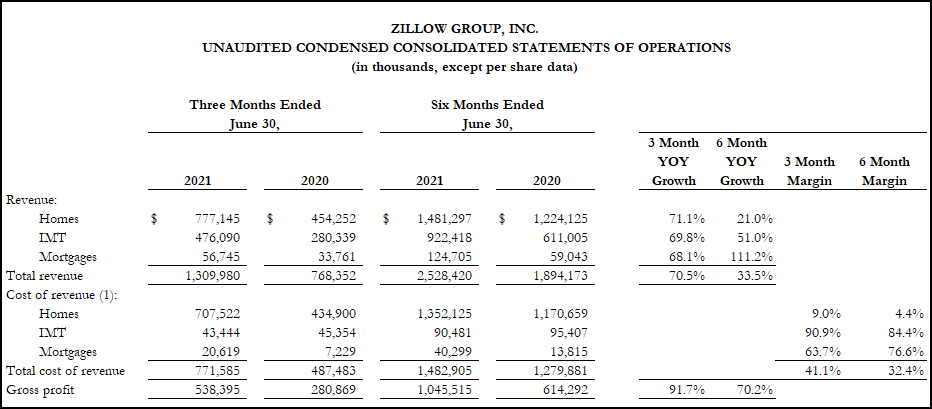

Today, Zillow operates three business segments:

- Internet, Media, Technology (IMT) (43.4% of revenues) – Zillow’s IMT segment includes their Premier Agent, the advertising arm for realtors, rentals, new construction marketplaces, as well as other display advertising.

- Homes (51.4% of revenues)– This is the newest segment for Zillow where they buy and sell homes directly.

- Mortgages (5.2% of revenues) – Mortgage company advertising, solutions, and software make up the mortgage segment for Zillow.

While Homes might look awesome with such a huge portion of revenue, it’s actually the least profitable on a gross margin basis.

In fact, their IMT division still rakes in the majority of their profits.

It’s important to point out because when you look at Zillow’s aggregate margins over time, they get significantly worse as home sales make up a bigger percentage of their revenues.

For the rest of the year, Zillow expects IMT growth to slow to 15% year over year and EBITDA margins to drop from 46% to 37%.

Mortgage outlook is flat for revenue. However, Zillow expects to lose between $6 million and $13 million EBITDA.

Homes is expected to increase to $1.45 billion, an 86.7% increase quarter over quarter.

Their total forecast for $2 billion in Q3 revenue blew away estimates of $1.45 billion.

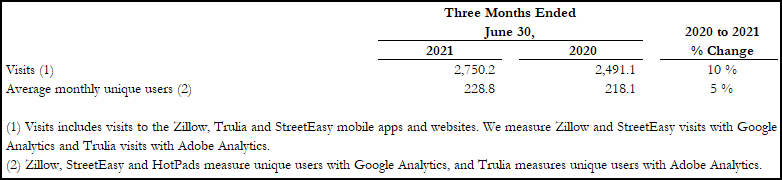

Now, a key ingredient to Zillow’s success is traffic.

While they increased year over year, they barely managed double digits in just one category.

Profits aren’t consistent

Zillow hasn’t been one to consistently deliver profits.

While they managed to finally break a 4-year streak in 2017, the next two years saw operating income worsen.

It wasn’t until 2020 that they started turning a profit again, and that began in Q3 of 2020.

Since then, they’ve had a year of solid earnings. However, they’ve only reached basic EPS of $0.60.

That puts their price to earnings ratio (P/E) at 75.88x.

In nearly every category, Zillow is more expensive than the sector median.

One important point to mention. Zillow’s cash flows are deeply affected by the amount of housing inventory it holds on its books. That means you can see wild swings quarter to quarter depending on how many houses they own.

So, one adjustment we can make is looking at their operating cash flows without this piece.

Doing a back of the napkin math, we get a cash flow to price ratio of $3.30 annualized.

Why bother doing this?

It gives us an idea of what they generate in cash from their business.

And even by that measure, it’s still rich.

But let’s do one last calculation.

Let’s say that we think Zillow could grow their earnings at 20% per year for the next 5 years and then 0% after that.

What would our old friend the Discount Cash Flow model, which takes streams of income and turns it into today’s dollars based on an interest rate, say?

Using a 12% discount rate, we would get a fair value of $49.43.

Ok, not great.

What if we did 20% for 5 years and then 2% every year afterward?

Only changes things to $55.23.

Now, let’s say we bring that discount rate down to 10%. Where does that leave us?

$60.40 and $70.08.

These calculations aren’t meant to say, ‘This is the value of the stock.’

It’s meant to give you an idea of what changes in different assumptions mean.

Our hot take

Zillow is a well-run company.

And they managed to make nice profits off their original core business.

But their growth now relies on an entirely new model that changes the dynamics.

It’s tough to assume they’ll continue at the same growth rate or achieve the same margins.