- Insperity grows consistently at 8%-10% in the highly competitive HR outsourcing space.

- Fundamentals suggest it’s overvalued except when you account for growth.

- A discounted cash flow analysis shows how there could be ~25% upside potential

- Technicals show price meeting resistance short-term against a longer-term bullish trend

Dear subscriber,

Hiring the right person is difficult, especially now.

Many businesses choose to outsource this and other human resource functions.

This highly cutthroat space is a tough nut to crack.

Yet, Insperity (NSP) manages consistent growth despite being much smaller than the competition.

Institutional advisor searches for the little-known company went from 0 to 572 in the last week.

That’s extremely unusual for a company with no news.

It got us curious as to what they saw.

We dug into the fundamentals and technicals of this company.

And we might have uncovered a unique value play.

Insperity in a nutshell

In 2020, the global human resource management market size was valued at $17.56 billion.

Over the next 8 years, it’s expected to grow at a compound annual rate of 12.2%.

Insperity formed way back in 1986. The company offers a broad source of human resources outsourcing including payroll, employment administration, benefits, workers’ compensation, government compliance, performance management, training and development, as well as talent acquisition.

Their two most comprehensive offerings are its Workforce Optimization and Workforce Synchronization solutions, with the former being its primary offering.

Insperity Premier is their current cloud-based human capital management platform.

Workforce Synchronization is offered only to middle-market clients. This low-cost offering comes with longer commitments that include many of the same compliance and administrative services as their Workforce Optimization solution.

Synchronization clients can add products and services from a menu of options for an additional fee.

For companies that simply want traditional human capital management and payroll, Insperity offers their Workforce Acceleration solution.

In a nutshell, they offer a wide array of human resource services, mainly targeted to small and medium businesses.

How much they buy determines the minimum contract commitment.

Lots of value

Insperity got smacked by Covid in 2020 as businesses retrenched.

Before that, revenues grew at around a 8%-10% clip annually, allowing them to more than double their revenues over the last decade.

Operating margins also improved, climbing from 2.9% to 3.4% over the same period.

Prior to the pandemic, they hit 4.5%.

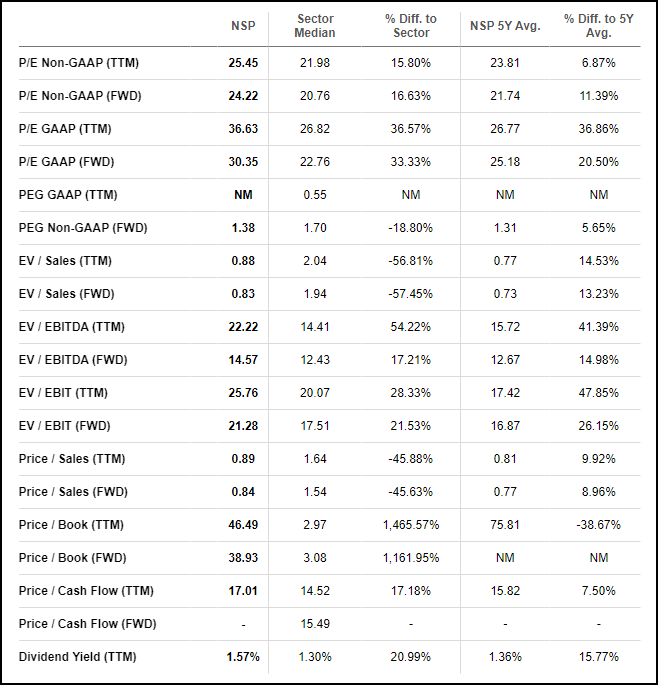

At first glance, the P/E ratio doesn’t look too great. But take a look at the EV to sales (price to sales) and price to earnings growth ratio (PEG).

NSP comes in lower than most of the industry in terms of price to EBIT and EBITDA.

It is worth noting that this compares it to the industrial sector which is fairly broad.

Looking at the basic performance measures tells us the stock is overvalued except when you factor in their growth.

So, let’s look at what a discounted cash flow analysis would yield.

When we go through their cash flows, we find their capital expenditures are a necessary part of their growth. Handling more business requires more buildings.

Otherwise, the operating cash flow seems like a good place to start.

When we take operating cash flow and subtract capex, we get an average cash flow of 3.96% of revenues.

Let’s take a look at the following scenario.

We made the following assumptions:

- Growth slows from 8% steadily over a 10-year period.

- Terminal growth is 2%, in-line with GDP.

- A discount rate of 6.46%

- The market implied discount rate for equities overall is 4.31%. Since NSP has a beta of 1.5, we multiplied 4.31% by 1.5.

Again, we want to point out that the output varies drastically based on your assumptions, especially the terminal growth rate and WACC discount rate.

But, we don’t think it’s unreasonable to say the stock has some upside potential from here.

Technically speaking

Turning to technical analysis, we find two key pieces of information on the weekly chart.

First, we’re about to hit a gap fill. These areas often act as support or resistance for a stock depending on the direction you approach from.

The second is the inflection level highlighted by the orange line.

We can tell this price is important because of how the stock bounces off it when it comes down from above, and struggles to break over it when it comes from below.

What this tells us is price is in a bullish (upward) trend, but it will likely slow down at the gap fill.

One thing to remember is that neither of these price points mean the reaction will be violent or particularly long-lived.

These are just areas where probabilities increase of a reaction from order flow.

Think of it this way.

Imagine a big fund comes in and buys the stock at the orange line.

As price goes up, it takes profits along the way.

If price goes back down into that line, that same fund now has a chance to buy more shares and try for another go at the same trade.

Our hot take

Insperity is a solid company that continues to deliver value to shareholders.

It may be a bit overpriced at the moment, but should be one to keep on your watchlist.

Top-trending tickers, market-moving news alerts: Straight in your inbox!

See the pulse of the market as researched by Wall Street Elites and receive top-trending tickers and other market intelligence to inform your trades.Sign up for Wall Street Connected – our free daily newsletter that leverages our TrackstarIQ Data.