Last week, Monster Energy (MNST) saw a +1,000% increase in search traffic from institutional advisors.

We found that intriguing considering the company reported earnings the week before.

Did these players know something we didn’t?

A quick look at the company’s valuation suggests it’s pricey.

But a deeper look revealed something interesting.

Monster Energy’s business

Previously known as Hansen Beverage, Monster energy markets and distributes energy drinks and alternative beverages.

In 2015, Monster signed a deal with The Coca-Cola Company (TCCC). Coke took a 16.7% equity stake in Monster while transferring ownership of its global energy drink business. That included brands like NOS and Full Throttle. In exchange, Monster gave Coke its non-energy business.

- Energy Drinks (93.6% of sales): Their largest segment by a mile, Energy drinks is exactly what you think it is – Monster Energy drinks. This segment also includes their former direct store delivery segments excluding the Peach Tea Brand.

- Strategic Brands (5.8% of sales): Strategic brands include names acquired from the TCCC Transaction. Interestingly, Monster kept in place the same business model with their acquisitions as their previous owners.

- Other (0.6%): Other includes the former warehouse segment and the Peach Tree Brand.

Energy drinks are immensely popular.

The global market was valued at $57 billion in 2020 and expected to grow at a compounded annual rate of 7% through 2025.

Monster has outpaced that with a 5-year average growth rate a bit higher than 11%.

In fact, their growth rate is pretty consistent year-over-year, never breaking below 9%.

Margins also remained pretty steady, though gross margin has declined from 63.7% in 2016 to 57.9% in the last 12 months.

Net margin has fallen from 35.6% to 35% during that same period. However, it grew from a low of 33.4% in 2019.

EPS consistently grew at a nice clip of around 22%.

Competitor comparison

Stacking up Monster against similar beverage and food companies, we get a sense that it’s currently overvalued.

Monster delivers better operating and profit margins.

However, it sits at a much higher price-to-earnings ratio than its peers both on a trailing 12 month basis and looking forward.

Even when you account for growth, its 2.31x PEG ratio is well above Starbucks (SBUX), though slightly lower than Pepsi’s 2.72x.

One advantage Monster has over its peers is its fortress balance sheet.

The company carries $1.5 billion in cash & securities with no long-term debt.

With over a billion dollars in cash from operations over the last several years, the company has bought back an insane amount of stock, reducing shares outstanding from 600 million in 2016 to 535 million today, a reduction of 10.8%.

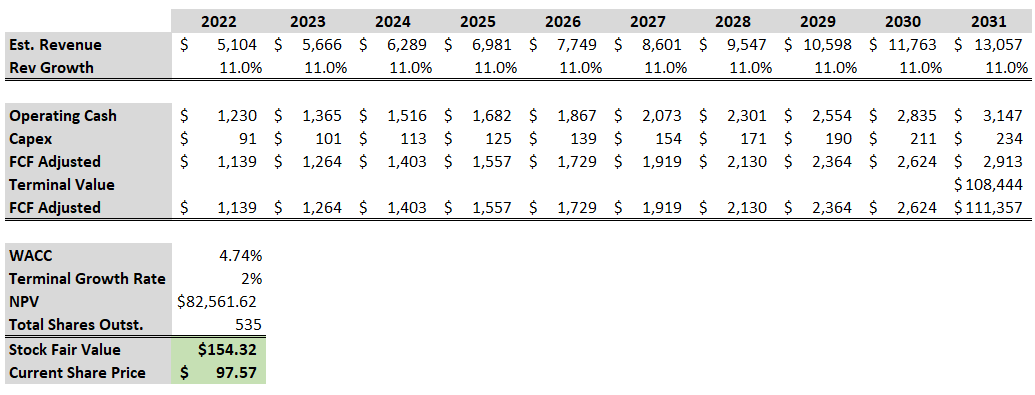

Discounted Cash Flow Analysis

Monster is a great company to run a discounted cash flow analysis on. They deliver consistent performance with little financing.

We know that revenue grows at around 11% while earnings grow around 20%.

Remember, we do a cash flow off cash, not revenues.

In this case, cash is pretty close to earnings.

Let’s assume for a moment that margins don’t improve and earnings grow at the same rate as revenues.

Using a 10th-year terminal value growth rate of 2% and a discount rate of 4.74%, we get the following output.

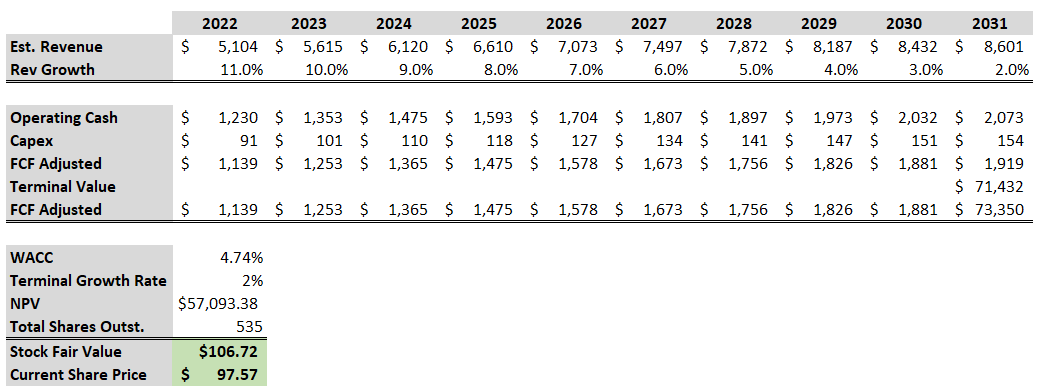

It’s probably fair to say that growth won’t always be 11%.

So let’s see what this analysis looks like if we start at 11% and then decrease it by 1% each year.

That knocks a sizable chunk off the value.

If you wanted to do a thorough analysis, you would perform a similar exercise with the competitors and see how they stack up.

Technically Speaking

Turning to our technical analysis, there is little doubt Monster is in a bullish uptrend.

Take a look at the daily chart below.

There are 3 key points to mention:

- Price recently broke the previous all-time high but came up short of the round $100 level. Breaking through the prior high and the $100 price level indicates buying pressure.

- Shares trade consistently above the 200-day simple moving average (green line). This moving average is often used by traders to determine the bullish or bearish nature of a stock. The purple arrow draws this out.

- $95 is an inflection point for the stock. You can see how that price acted as resistance, then support, then resistance again. Should shares fall back down to this area, probabilities are high that it will find support.

Our hot take

Monster Energy’s price is built on growth.

Unlike many other companies, Monster proves it can reach these targets year after year.

Given the macro trend behind energy drinks, it appears likely they will achieve growth targets over the next five years.

That said, like many other high-growth companies, it is susceptible to rate increases.

Top-trending tickers, market-moving news alerts: Straight in your inbox!

See the pulse of the market as researched by Wall Street Elites and receive top-trending tickers and other market intelligence to inform your trades.Sign up for Wall Street Connected – our free daily newsletter that leverages our TrackstarIQ Data.