As you know, the genesis for many of our stock ideas comes from our proprietary database.

Today, a company our team had never heard of popped up.

Ironically, it fit in nicely with today’s edition of The Juice that discussed the Fed.

We think this stock might be an overlooked gem.

Overall, banks haven’t fared as well as the rest of the market.

They rely on borrowing and high interest rates to make money, especially regional banks like Heartland Financial (HTLF).

Heartland offers a unique blend of growth and timing we thought was worth a look.

Check out our analysis and see if you agree.

Heartland Financial in a nutshell

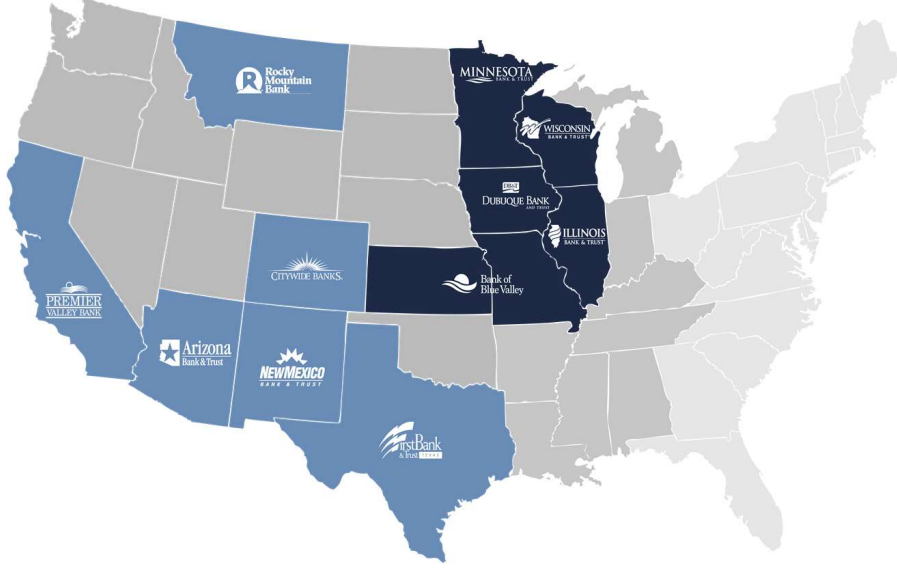

Headquartered in Dubuque, Iowa, Heartland Financial was established in 1981 and has traded on the Nasdaq since 2003.

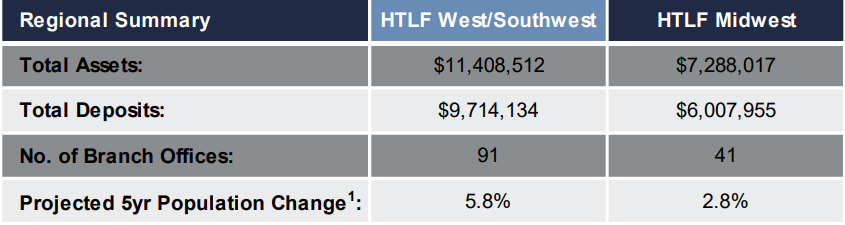

The company consists of 11 independently chartered banks and 132 branches in 12 states across the Midwest, Southwest, and Western regions of the country.

Heartland has chosen to grow through M&A with 13 acquisitions over the last 7 years.

Fed funds rates will be key to their earnings growth in the coming years.

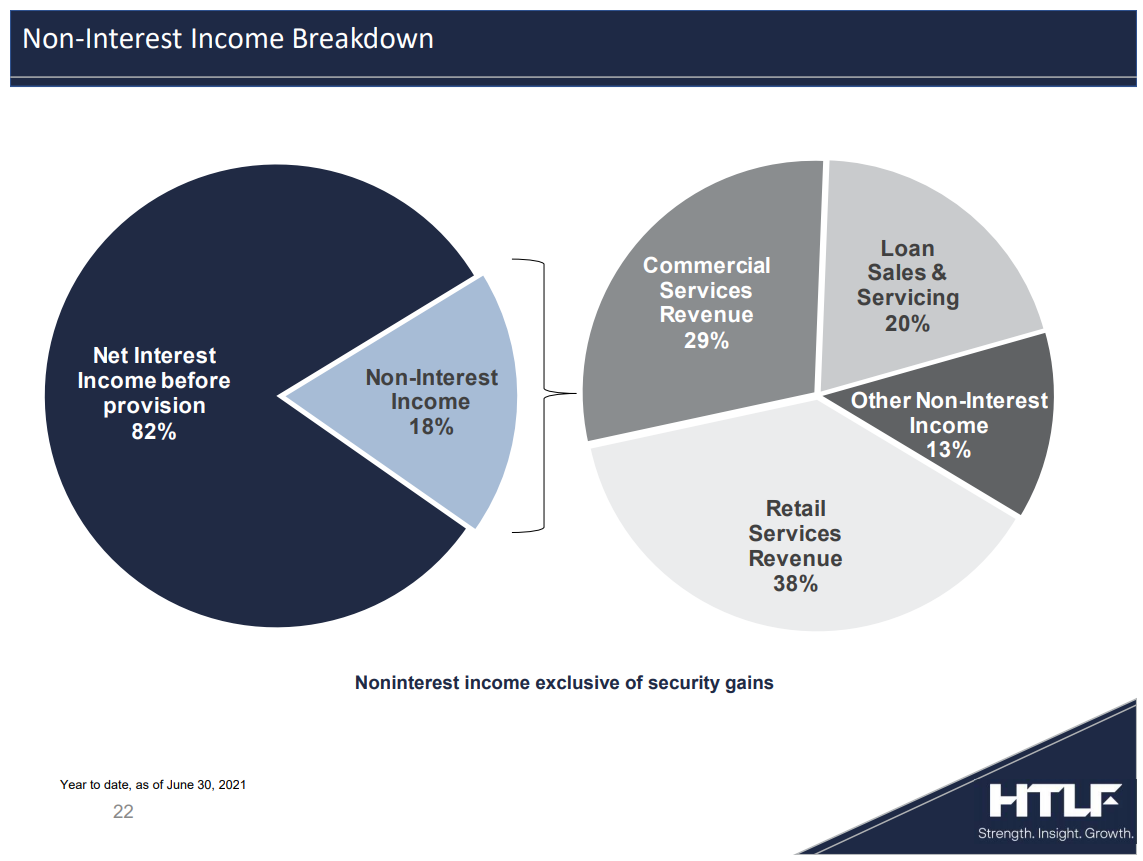

Unlike big banks like JP Morgan who get less than half its earnings from net interest income (NII), Heartland relies on NII for 82% of its income.

Net interest income is the difference between the rates a bank borrows and the rate it lends at.

Banks borrow using short-term rates, which are much lower, and lend at long-term rates, which are much higher.

For example, a bank might borrow at the 2-year treasury rate of 0.23% and lend at the 10-year rate of 1.24%, making 1.01% on the money it borrows (IE savings accounts for customers).

When interest rates rise (IE the Fed raises rates), long-term rates move up faster than short-term rates.

Using our same example, say both the 2-year and 10-year rate rise 20%.

Your 2-year rate is now 0.276% and the 10-year is 1.488%.

Now the spread is 1.212%.

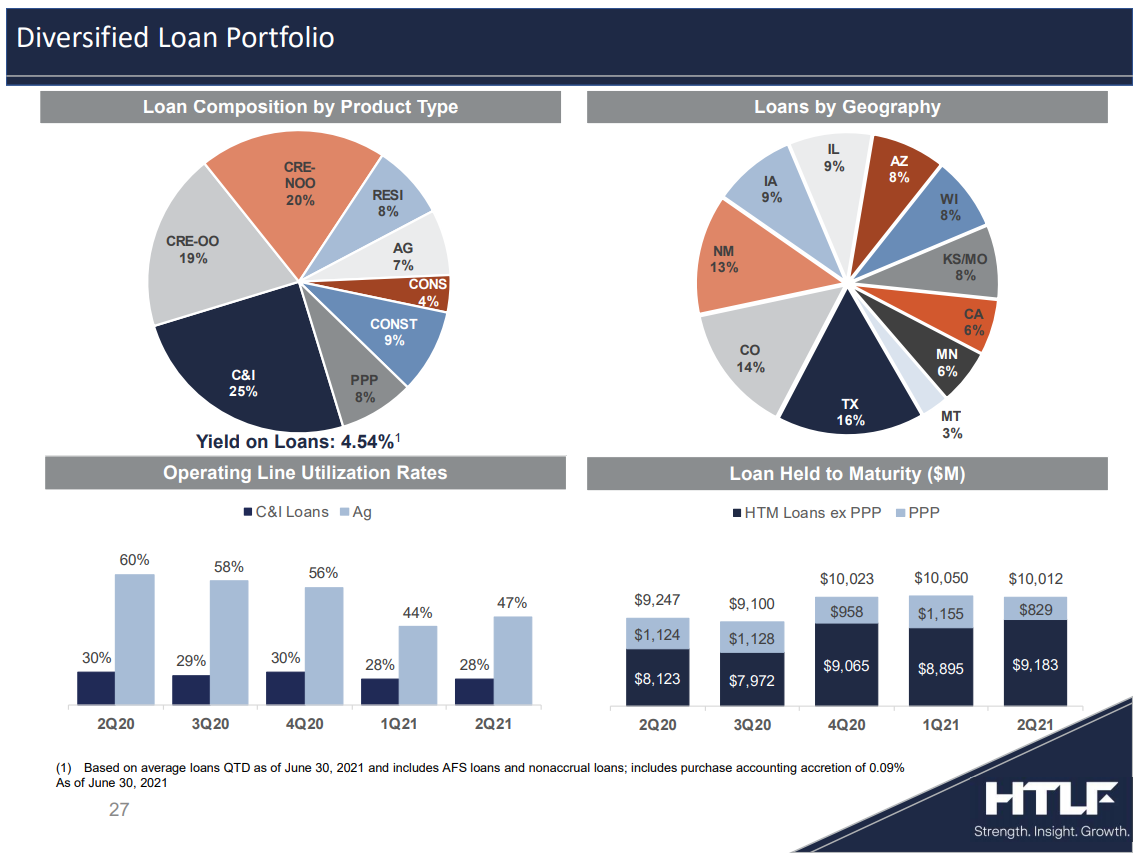

The question we want to answer next is who is getting these loans.

Heartland was kind enough to not only break it out for us but tell us the rate they get on their loans.

Ledger:

CRE = Commercial Real Estate, (N)OO = (Not) Owner Occupied

RESI = Residential, AG = Agricultural, CONS = Consumer

CONST = Construction, PPP = Paycheck Protection Program

C&I = Commercial & Industrial

Overall, they hold a balanced portfolio with a skew towards commercial real estate.

About half of their construction portfolio consists of multi-family or multi-unit facilities.

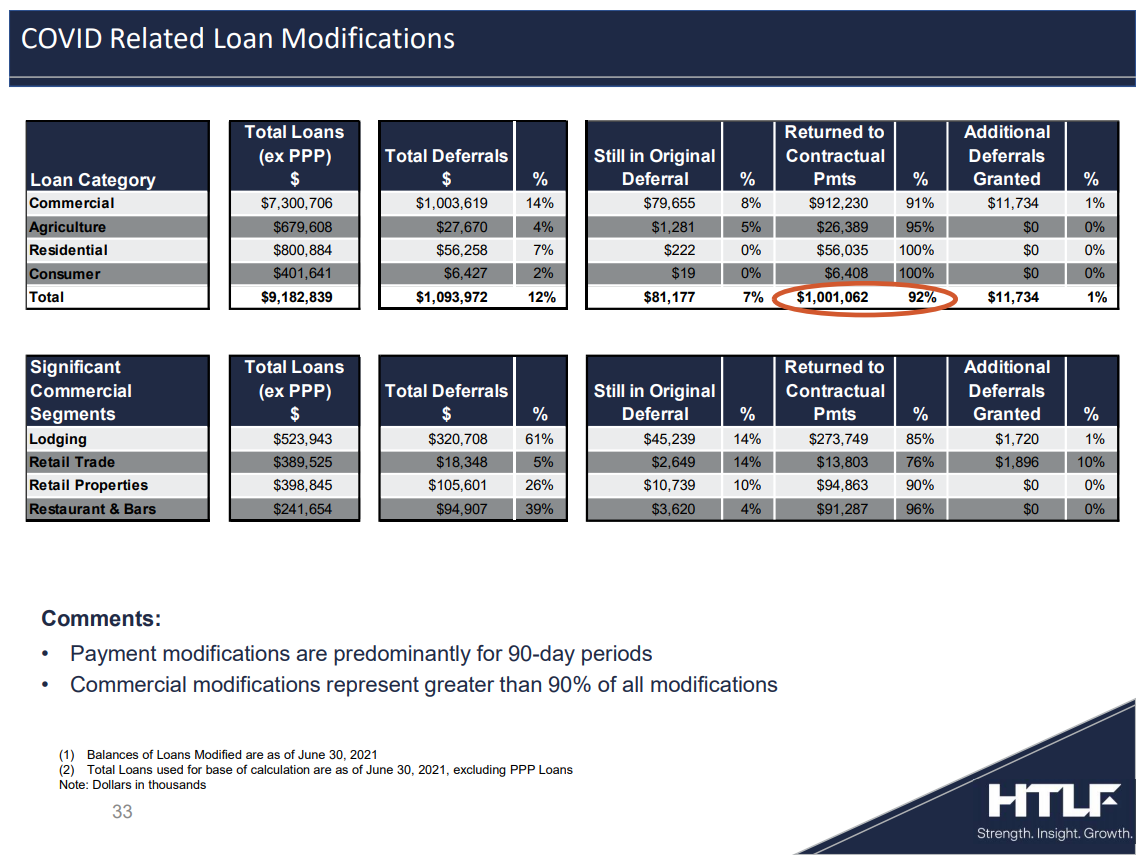

Because of their significant commercial real estate exposure, Heartland ended up making a significant amount of loan modifications. So far, they’ve gotten most of the deferred money back.

As you can see, the travel and leisure segment hit them the hardest, as it did most other banks.

Total loan deferments as a percentage of their total loans did drop in the most recent quarter by 2% from the previous quarter.

However, over half of those were interest modifications.

What’s their value

Banks can be tricky to evaluate because of how they operate.

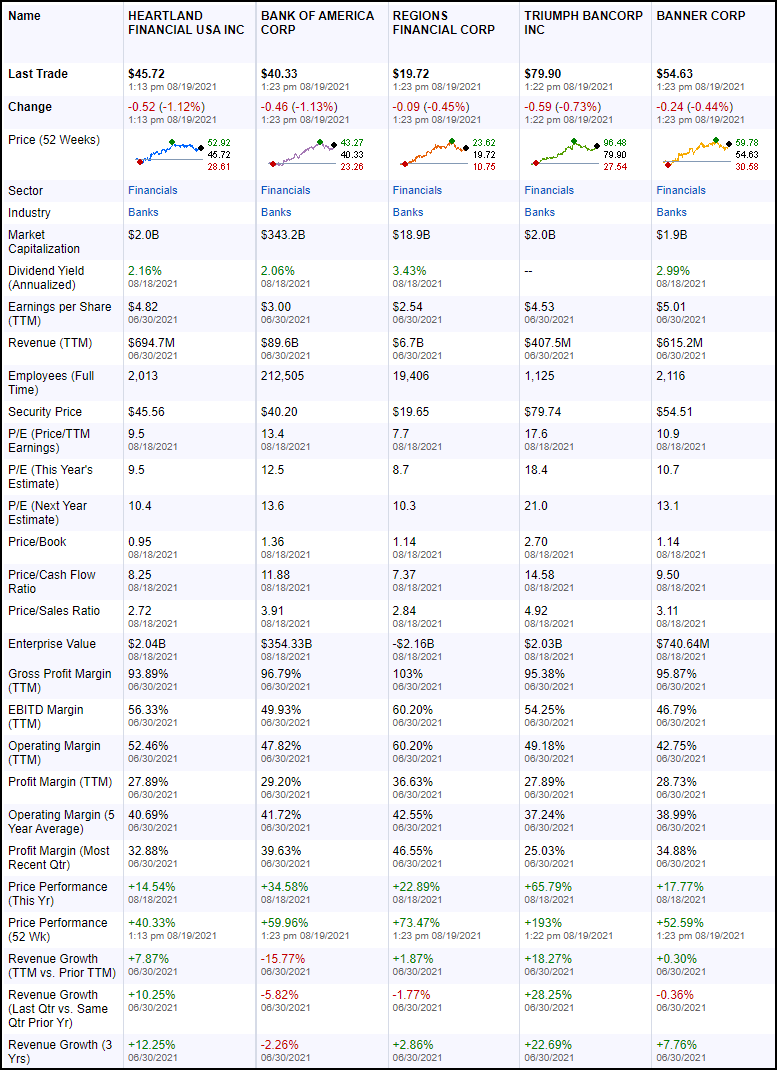

It’s best to compare them to competitors to get a sense of where they stand.

We listed Bank of America to help you get a sense of where big banks land compared to regionals.

Regions Financial is one of the larger regional banks.

The other two are comparable regional players.

Right off the bat, we can tell that Heartland comes in pretty cheap.

It’s at the lower end of P/E ratios, Price to Book, Price to Sales. The only bank that comes close is Regions.

From a profit margin standpoint, they’re at the lower end, although not by much.

For growth, Heartland comes in the middle of the pack.

Discounted Cash Flow Model

DCF models can be a little tricky. Especially since we expect margins to improve soon as rates head higher.

Free cash flow (FCF) for HTLF is pretty inconsistent as well.

But here’s where things get interesting.

We took the average FCF for the last 3-years and came up with $181.67 million.

If HTLF earned that exact same cash flow into perpetuity, with a 10.55% discount rate, we come up with $43.05 per share.

Obviously, that’s below the current share price.

But that is a VERY conservative estimate.

Every 1% in growth for the 10-year period adds around $3 to the share price.

So, with a share price around $45, that’s not too shabby.

Technically speaking

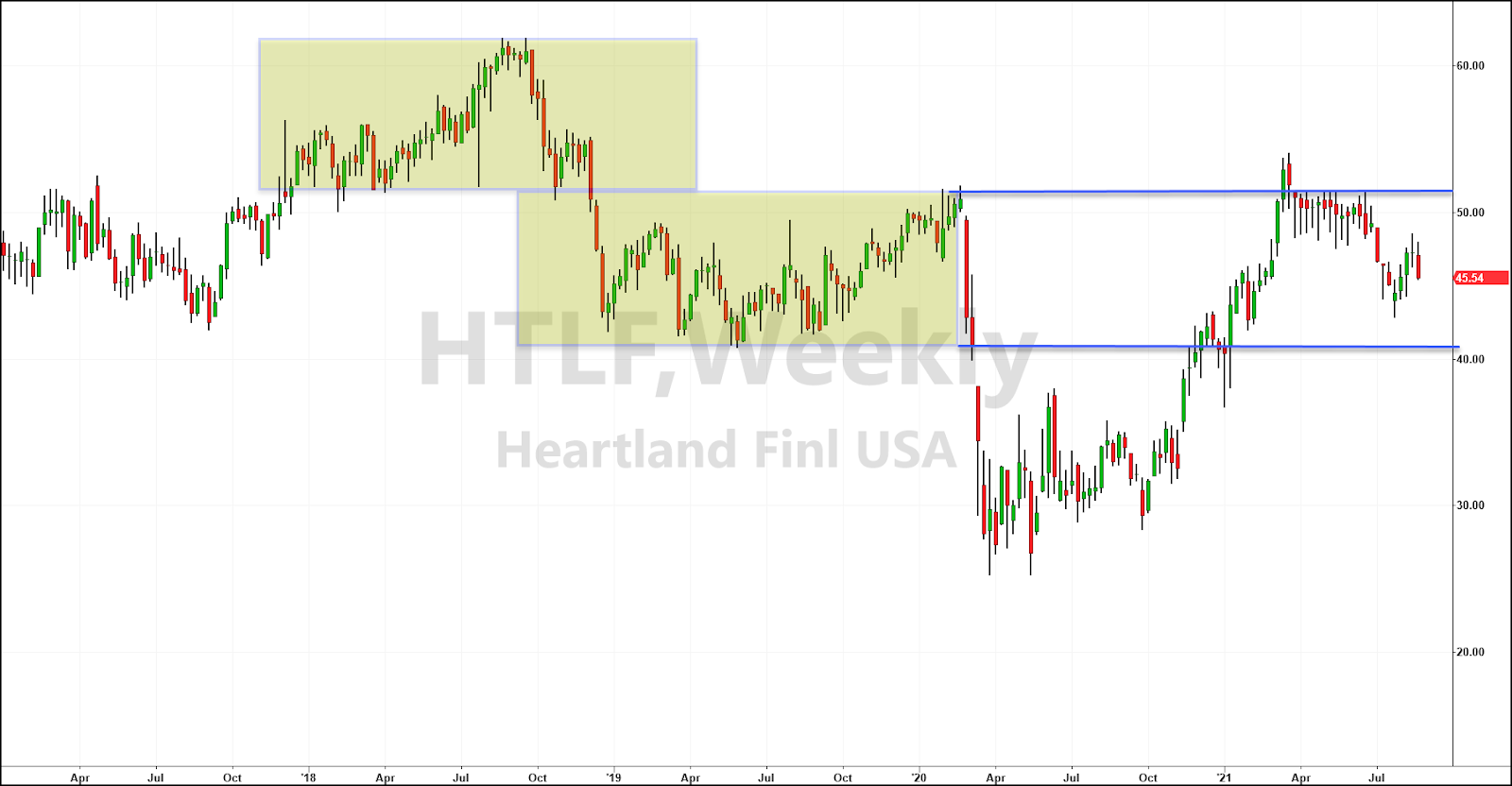

The chart for HTLF is actually very easy to understand.

Below, we’ve drawn out two boxes in yellow and then extended their edges out in time with blue lines.

Those are the support and resistance lines.

That’s where the stock’s price should have trouble breaking through.

How do we know?

It struggled to do it before.

In the top left box, you can see it tried for several weeks to break through the old high.

When it got down to the bottom of the range, it took more than one try to break through.

Once it did break through, it couldn’t get back above that level before the market crashed out.

And look at where the market stopped on that second week of heavy selling last year, right before it plunged.

Our hot take

Banks have a nice catalyst to boost their earnings over the coming months and years.

Take some time to look through the regional ones and see what they own.

Are they exposed to commercial or residential?

How about hotels?

Heartland is a great find as long as rates head higher. If they don’t, then the stock is likely to suffer.

Top-trending tickers, market-moving news alerts: Straight in your inbox!

See the pulse of the market as researched by Wall Street Elites and receive top-trending tickers and other market intelligence to inform your trades.Sign up for Wall Street Connected – our free daily newsletter that leverages our TrackstarIQ Data.