Domino’s Pizza (DPZ) used to suck…hard.

It tasted like cardboard.

And its spokesperson was some putty creature cross between the Trix Rabbit and a serial killer.

Like a terrible 80s movie, Domino’s put together a montage of music and charm, clawing its way back into peoples’ hearts.

Today, it’s the largest pizza company in the U.S. and around the world.

Like the US Postal Service, they cover nearly every household in America.

Our proprietary database highlighted a massive uptick in searches from financial professionals for Domino’s.

And it got us curious.

At a high level, shares look insanely expensive.

But is there something more below the surface?

Domino’s Rebrand

If you never tasted Domino’s Pizza from 20 years ago, consider yourself lucky.

It was an experience akin to a fist fight with your stomach.

Put their 30-minute guarantee or it’s free even got Ninja Turtles excited.

A survey of national brands dumped Domino’s in last place with Chuck E’ Cheese (a whole other place filled with robotic nightmares).

To top it all off, viral videos hit the net that showed pizzas being made with…well let’s just say ingredients not approved for consumption.

So, in 2009 Domino’s got a makeover.

Corporate redid their recipe and profile from top to bottom.

For once, their pizza wasn’t just edible, it was pretty darn good.

And the company grew…quickly.

Today, the company runs 6,426 U.S. locations and 11,631 internationally.

Over the last decade, annual revenue growth hit 10% each year as well as positive earnings, and free cash flow…the triple turkey.

During that same time period, gross margin improved from 28.5% to 39% while Operating margin increased from 15.7% to 18.1%

EPS growth averages 23.93% over the last decade as well.

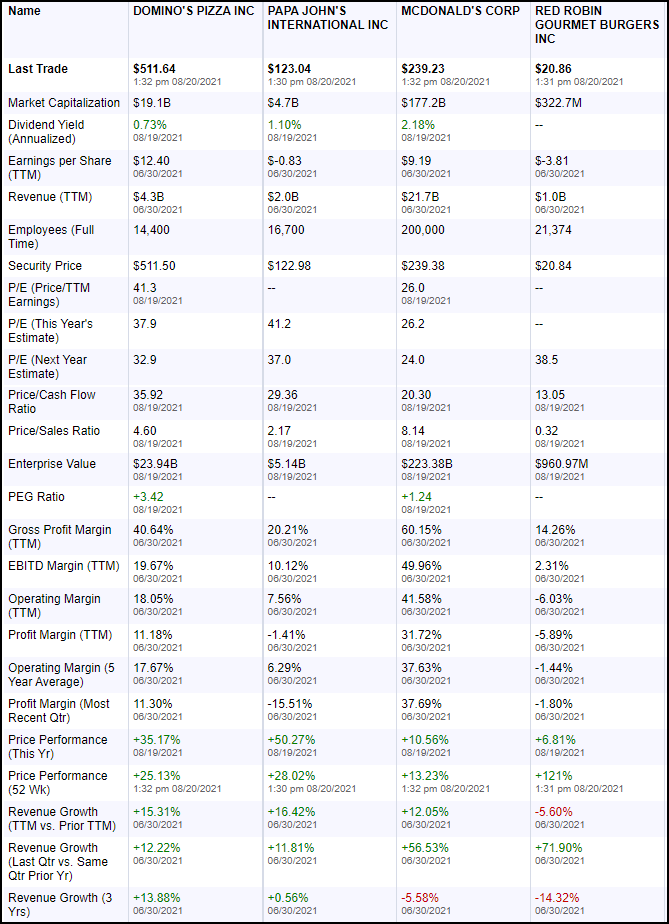

Poor valuation but…

Valuations for the +$500 stock aren’t great.

But then again, its competitors don’t look so hot either.

Papa Johns (PZZA) is the only other publicly traded pizza chain.

Compared to them, Domino’s P/E ratios now and looking forward are better.

However, they’re more expensive on almost every other valuation measure.

Yet, there’s one thing worth noting.

Only McDonald’s (MCD) displays a Price to Earnings Growth Ratio (PEG).

That means Domino’s and Mcdonald’s are the only ones in this chart that grew earnings.

In fact, Papa John’s earnings over the last 12 months are negative as they were in 2019.

When it comes to profitability, Domino’s beats out Papa John’s across the board.

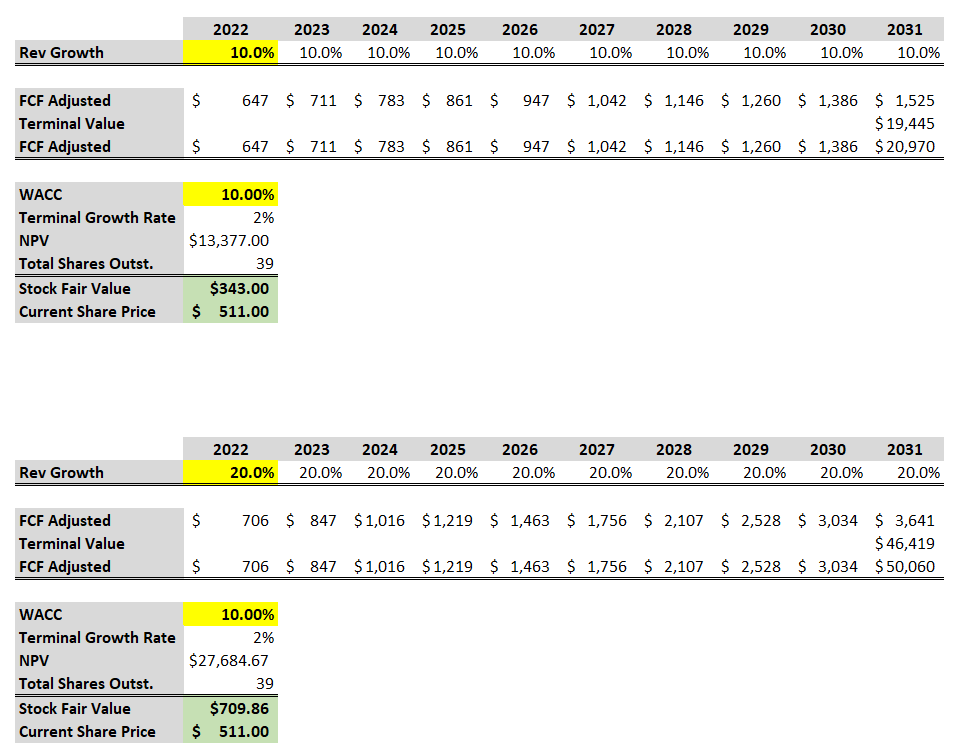

Discounted Cash Flow Says

Free cash flow grew an average of 20% in the last 10 years.

However, revenue grew at 10%.

Our calculated discount rate is 6.54%. But, it was near 10% just a few years ago.

So let’s see what different inputs get us:

In the first two models, we assumed the 6.54% discount rate and ran 10% and 20% 10-year growth models.

Both show nice upside potential.

In the second two models, we ran the same scenario, but jacked up the discount rate to 10%.

For these models, 20% growth leaves some nice upside, but 10% does not.

A word of caution

There is one glaring problem with Domino’s…its debt.

If you look on the balance sheet, you’ll notice that long-term debt continues to grow and retained earnings get more negative.

Neither of these are inherently bad.

In fact, their return on assets (ROA) of 29.54% and return on investment (ROI) of 39.47% demonstrate their ability to effectively use their capital.

However, the debt can become a drag as interest rates rise.

The negative retained earnings could indicate an unprofitable company. But in Domino’s case, it has more to do with how they went from private to public in the 2000’s.

Technically Speaking

Domino’s chart is about as bullish as they come.

What you’ll notice is the long uptrend since March of last year.

Additionally, we have what’s known as a flag pattern.

People that read charts look at this as a bullish consolidation.

Typically, a stock makes a sharp move higher and then starts to trade sideways, sometimes lower.

The key is that it never breaks below and stays below the original thrust higher (the part that makes the flagpole).

Traders read the strong push higher as conviction buying. The consolidation means that no major sellers are stepping in.

Ideally, buyers eventually step back in and push the stock to new highs.

Our hot take

There are a lot of reasons to like Domino’.

While share prices aren’t cheap, the company’s growth gives them a lot of value.

And technically speaking, that flag pattern is about as textbook as they come.