People are spending more on their homes than ever before.

Homeowners shelled out nearly $351 billion in Q1.

Forecasts put Q2 growth at 5.4% or $370 billion.

One of the top investments for any homeowner – countertops.

Installing granite, natural stone, or similar materials can increase the value of a home by as much as 25%.

If you’re looking for a top name out there, no one is better than CaesarStone (CSTE).

And with search data amongst financial pros spiking 201% in the past two days, we wanted to take a deeper look into this cash cow.

Caesarstone’s Business

Caesarstone’s unique countertops incorporate engineered quartz, a durable, abundant material that creates a uniform, modern appearance.

Headquartered in Sdot Yam, Israel, Caesarstone is a premier brand amongst interior designers and home builders.

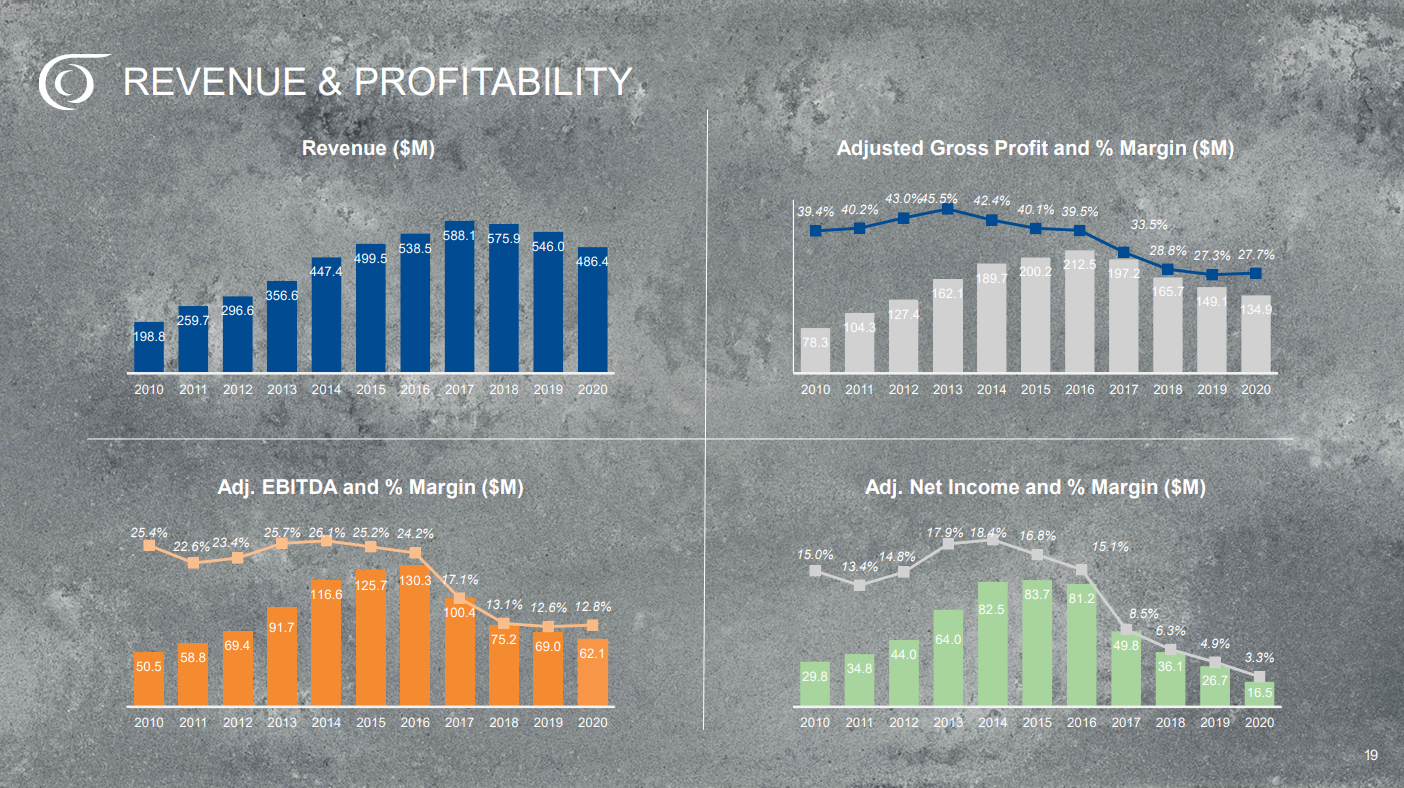

Growth hasn’t always been steady for the company, despite throwing off cash every year.

In 2011, the company hit $260 million in revenue. 2020 landed at $486 million.

Their peak came in 2017 at $588 million.

In 2018, the company began executing its three-pronged turnaround strategy.

Specifically, the company aimed to increase gross margins from 27.7% in 2020 to 32%-35% as well as expanding EBITDA margins from 12.8% to 17%-18%.

As part of the plan, Caesarstone recently acquired Lioli Ceramica, an India-based producer of porcelain slabs, a countertop material expected to grow at 10% annually through 2025.

Profitability

So far, the company has yet to improve its margins.

On a quarterly basis, gross margin landed at 29.65% and 28.01% the last two quarters.

But their gross profit margins start back in 2018 when a combination of higher raw material costs and poor manufacturing performance, neither of which has changed.

Value

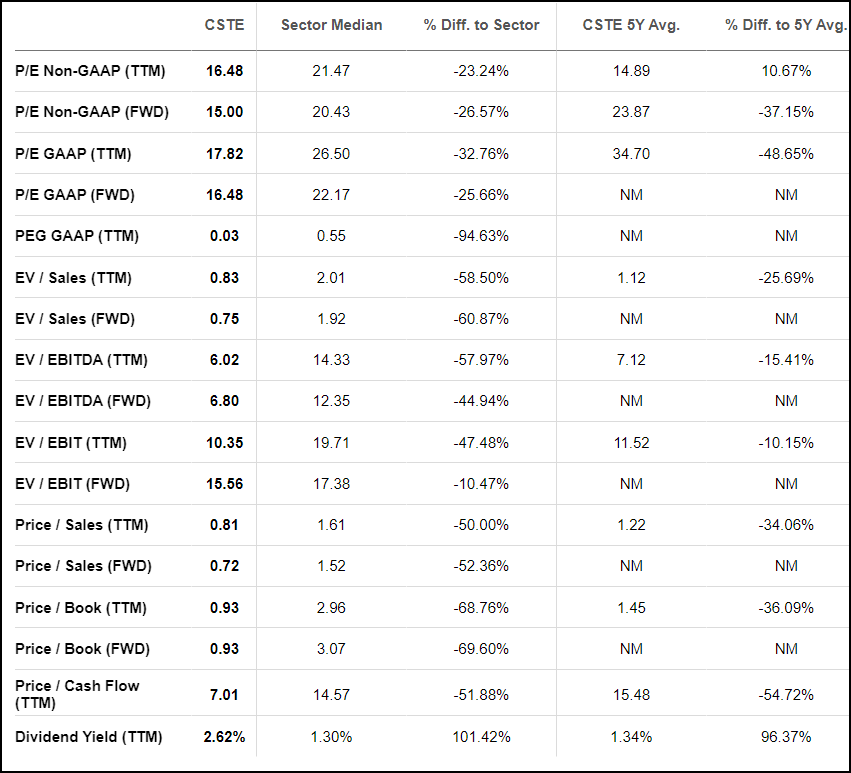

That said, shares are quite cheap.

From a value perspective, Caesarstone is cheap on nearly every metric from price to earnings (P/E) to price to cash flow.

So, if nothing else, at its current profitability, there is value.

Discounted Cash Flow Analysis

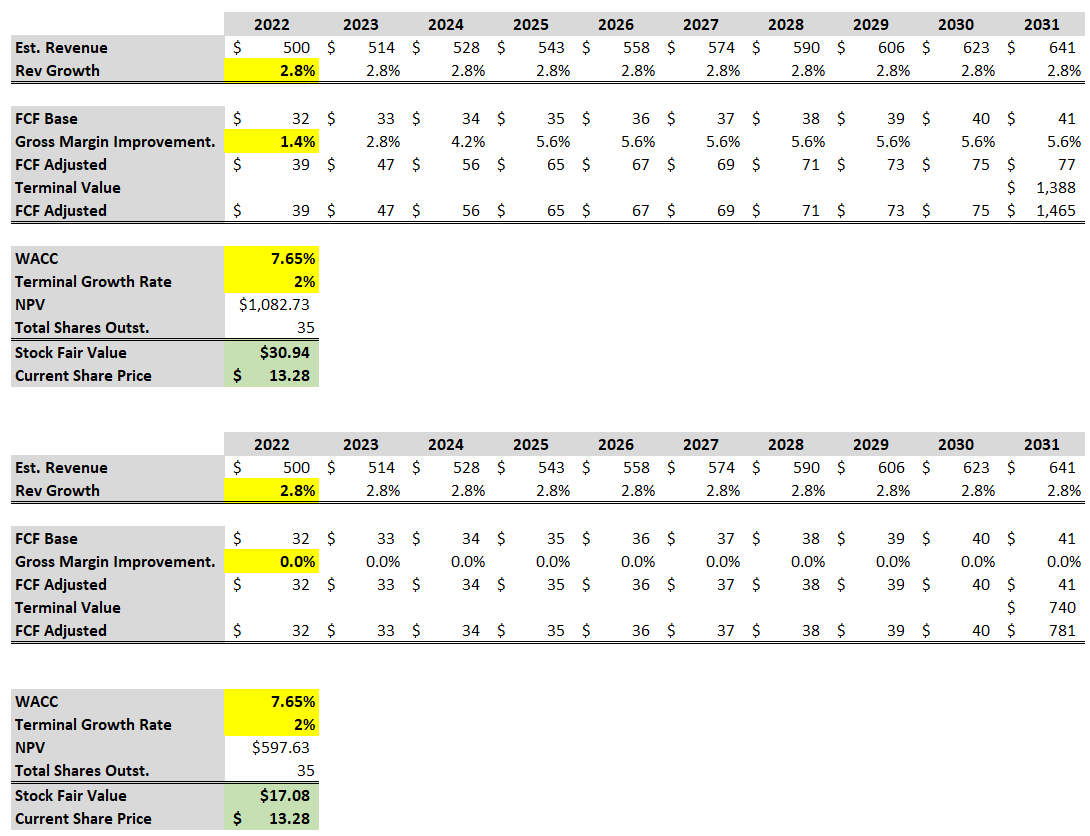

Caeserstone gives us a chance to do some interesting DCF analysis.

Globally, the countertop market is expected to grow at 2.8% per year.

We can use that as our growth rate baseline with a terminal growth rate of 2%.

What we want to model is the value of the stock with and without improved margins.

So, let’s see what that looks like assuming they slowly improve margins until 2026.

Our WACC is 6.42%.

The analysis is quite clear.

Based on current market valuations, not a lot of investors expect Caesarstone can pull off its turnaround.

However, even if they just float along at the same profit year after year, there’s upside potential in the stock.

Technically Speaking

The weekly chart for CaesarStone gives us a clear picture of what happened to this company.

You can see a clear decline in 2017-2018 as margins fell apart.

Since then, shares traded between $13-$20.

Currently, they’re at the lower end of that range with $13 as the key support level.

As long as that support holds, it’s an ideal spot to enter a trade or investment.

The bottom line

Even without a turnaround, CaesarStone looks woefully underpriced.

In this market, it is one of the few stocks priced for value investors.

Top-trending tickers, market-moving news alerts: Straight in your inbox!

See the pulse of the market as researched by Wall Street Elites and receive top-trending tickers and other market intelligence to inform your trades.Sign up for Wall Street Connected – our free daily newsletter that leverages our TrackstarIQ Data.