With the rash of mergers and acquisitions, you would think bigger is always better.

Sleep Number (SNBR) proves that’s not true.

They do one thing and they do it darn well.

With no relevant news, the +200% spike in financial pros search volume the last two days stood out like a sore thumb.

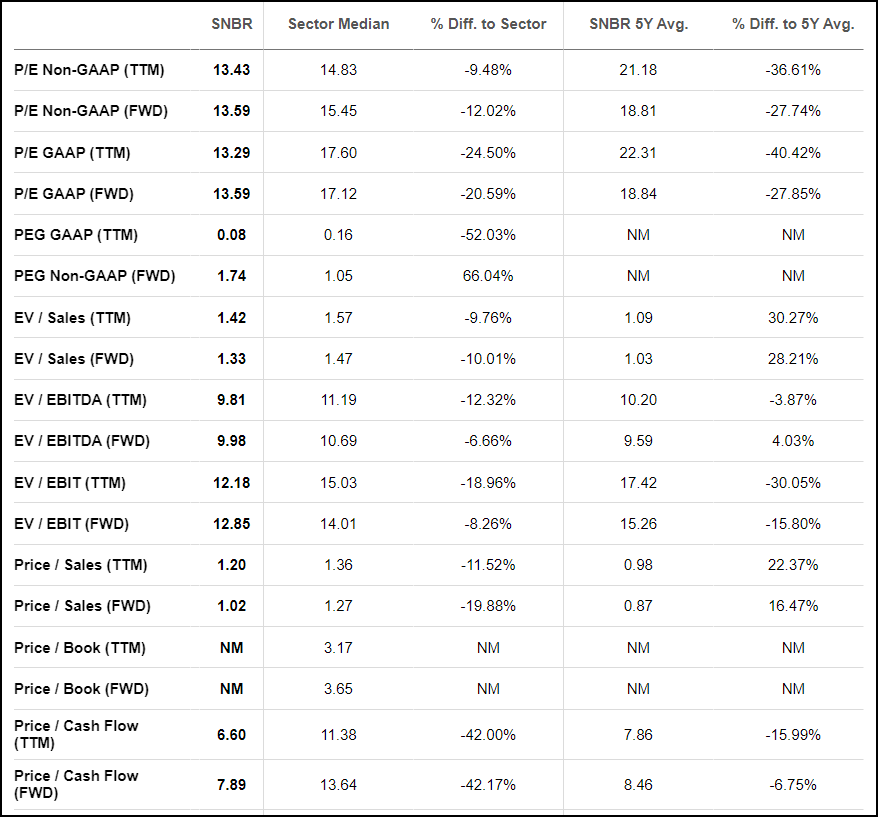

Right now the stock trades at a 13.29x price to earnings (P/E) ratio.

And that’s just the start of the good news.

Sleep Number Basics

Sleep Number makes mattresses. That’s it.

It just so happens their mattress are freaking awesome.

Despite running 602 retail stores across the U.S., Sleep number managed to increase revenues every year for the last decade including 2020.

However, Sleep Number offers direct-to-customer sales online and over the phone.

Sleep Number seels 99.7% of their volume through retail. Only a small sliver comes from Wholesale. Of retail sales, 85% comes from the stores.

The company spends a bit more than 2% of revenues on research and development to maintain their competitive edge.

That’s helped them develop the 360 Smart Bed’s SleepIQ technology. The integrated app expands on the internet of things while providing information to help users enhance their sleeping experience.

Growth & Value

Bears would have you believe that supply chain issues are much worse than they are.

And with some difference to them, management often over promises and underdelivers.

But that doesn’t change their performance.

Here are some key growth facts worth noting:

- 5-year average revenue growth = 8.87%

- 5-year average net income growth = 22.47%

- 5-year average EPS growth = 38.26%

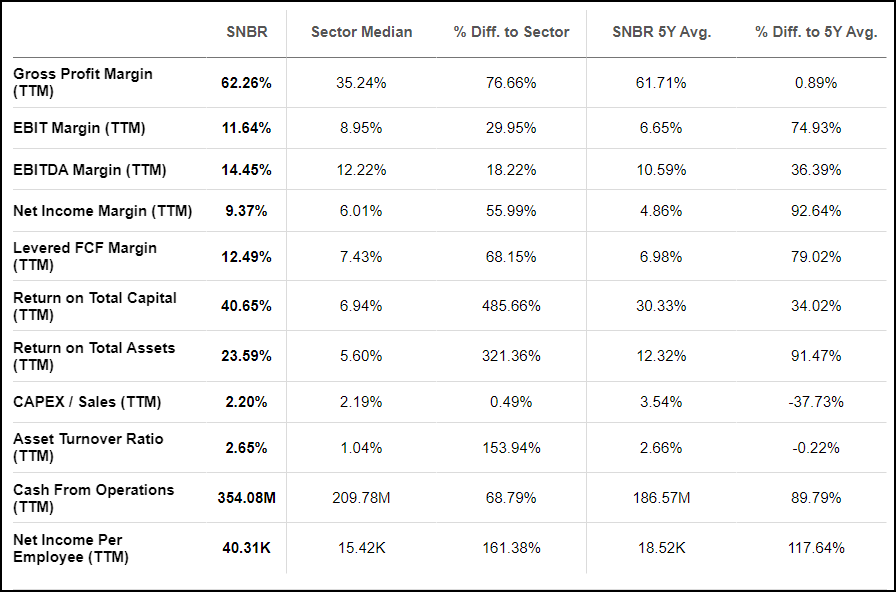

On top of that, their margins are fantastic, beating the sector median in every category. In fact, current margins are better than their 5-year average in all but one category.

Turning to value, we already noted their P/E ratio of 13.29x.

Currently, their forward P/E ratio of 13.59x would suggest headwinds either in revenue growth or operational costs.

Given the myriad of supply chain issues, we believe it’s the latter.

Still, the company comes in better than the sector median in every category and most categories against their 5-year average.

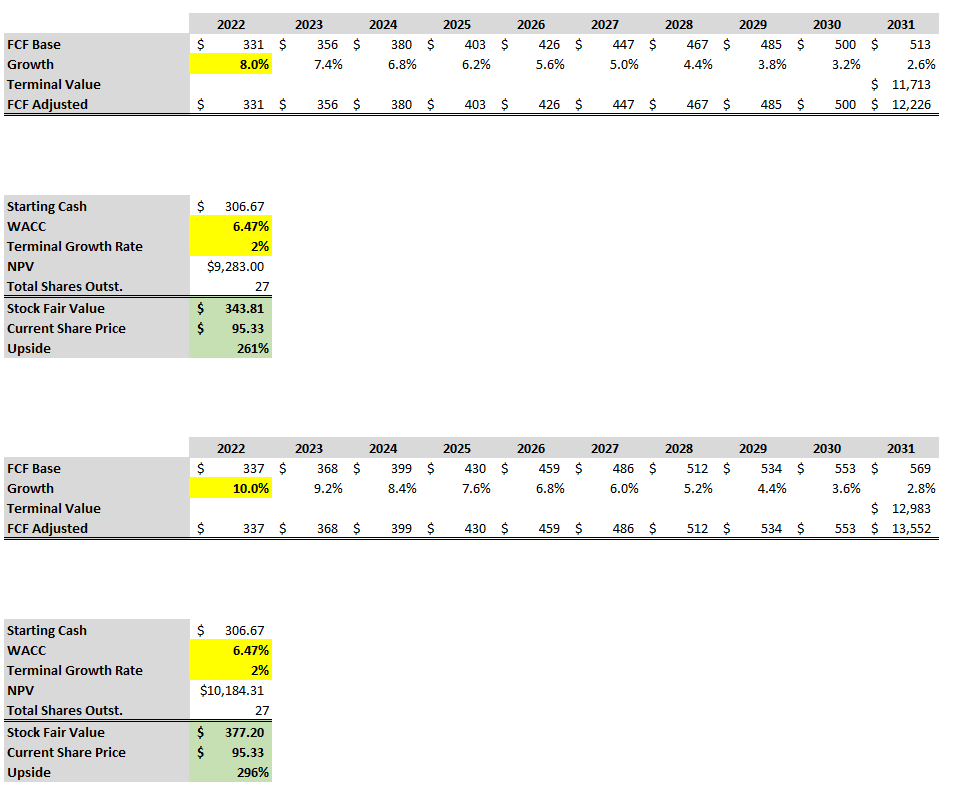

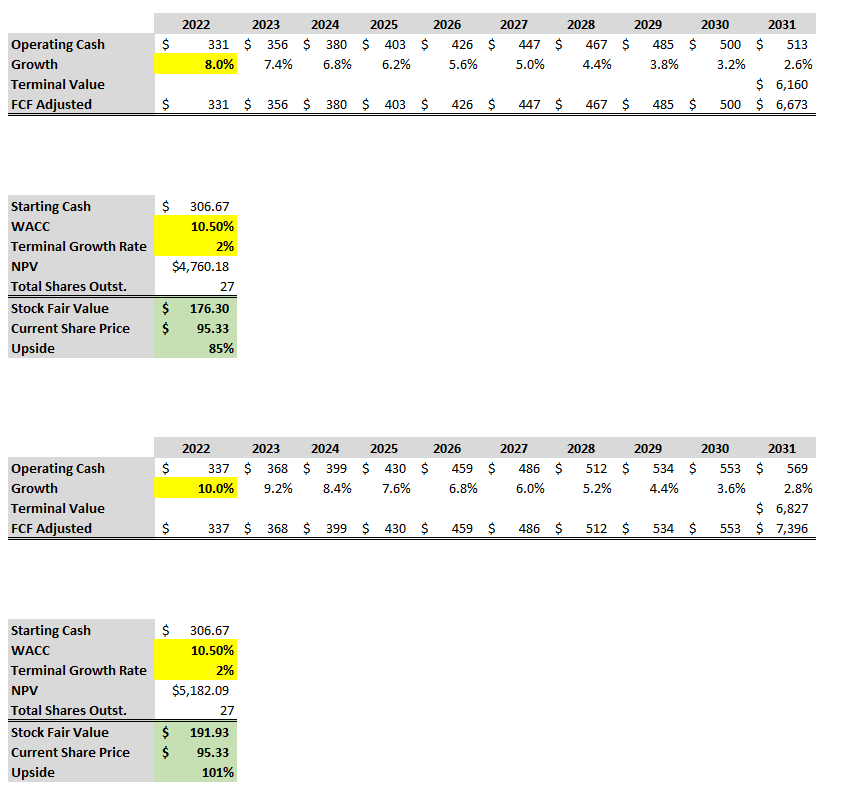

Discounted Cash Flow Analysis

Things get a bit tricky when trying to determine the company’s cash flow growth.

As we noted above, revenue only grew at around 8%, while EPS and margins were well into the double digits.

When we looked into their cash flows, it appeared that a few acquisitions and investments played with the free cash flow calculations.

So, we used operational cash flow and then took out Capex.

Let’s try looking at 8%, and 20%, growth rates that decline each year for 10 years with a 2% terminal value growth rate.

We also want to run the same scenarios with a 6.47% WACC and a higher 10.5% WACC to get a well-rounded look.

No matter how you slice it, the DCF model says the stock is undervalued.

Even with a starting FCF at half the current level, you’d only be slightly overvalued using the 10.5% discount rates.

Technically Speaking

Sleep Number’s daily chart looks pretty awful.

After the stock peaked back in Q1, it slid almost 50%, finally dropping below the 200-period simple moving average (the average of the closing prices for the last 200 days).

Unfortunately, there aren’t any support levels until you get to around $80.

While that’s bad for traders, it would be great for investors who want to buy the stock for the long-term.

Our Opinion – 👍👍👍👍/5

Sleep number’s financials are fantastic.

It’s really tough to make a case against the stock other than a bad-looking chart.

Short-term, it’s possible they could see issues related to supply chain disruptions.

So far, that hasn’t happened. And we prefer to go by what we know.