|

Proprietary Data Insights Financial Pros Top Inflation Protected Bond ETF Searches This Month

|

What we’re watching

|

|

A look at some ETFs that investors often use to combat inflation.

|

|

ETFs |

Why you shouldn’t invest in inflation protected securities |

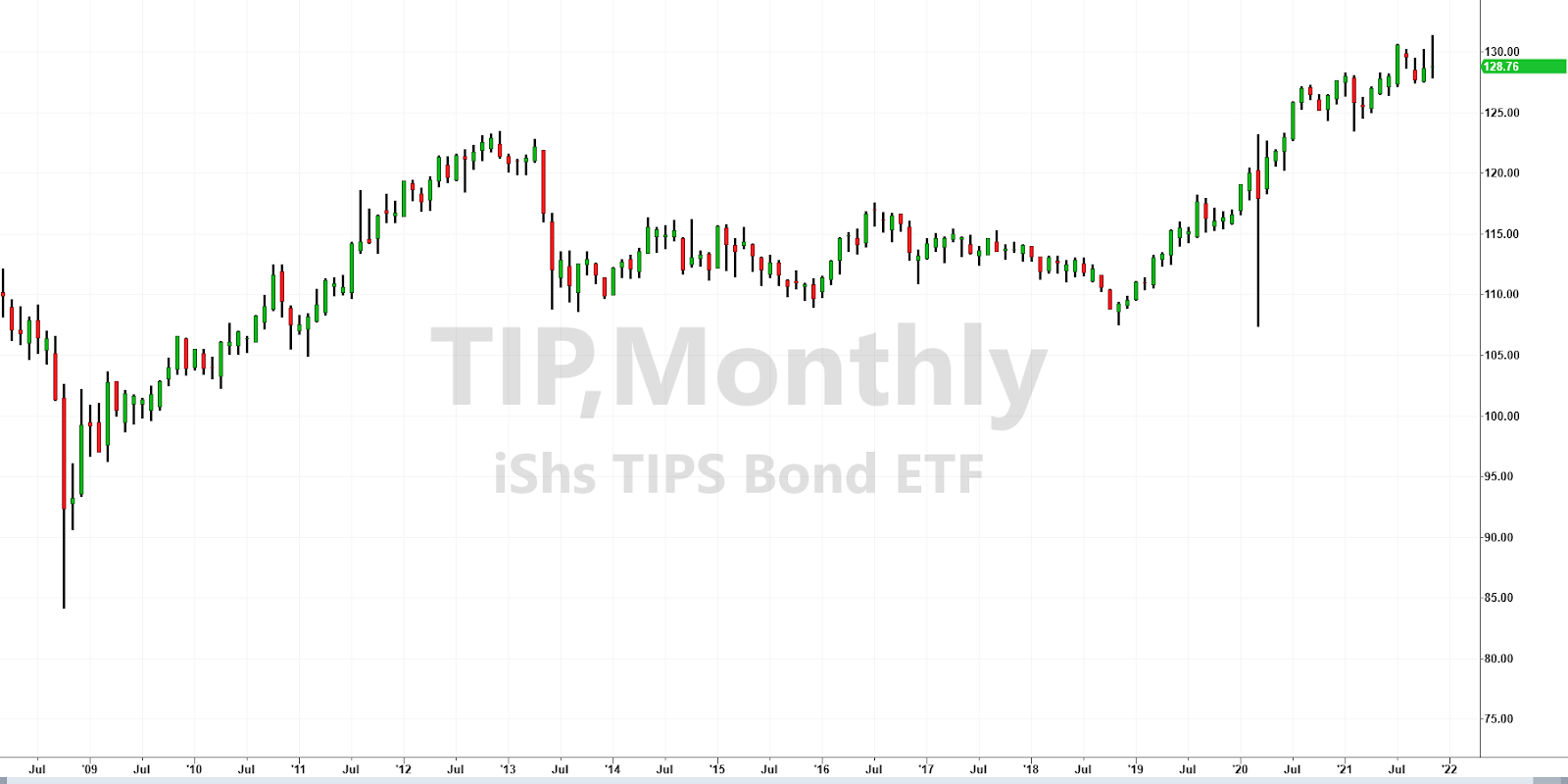

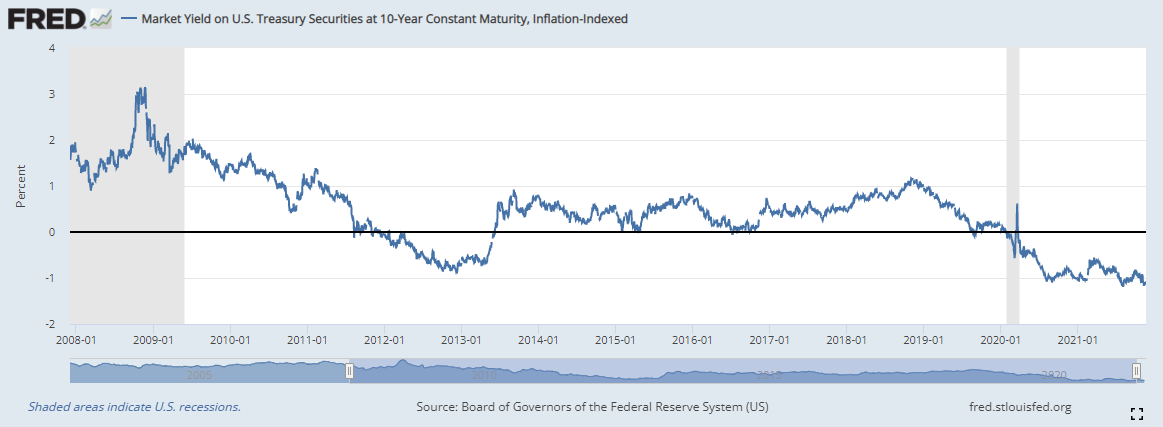

We know that a lot of you are worried about inflation. It was the single biggest topic discussed at Thanksgiving this year other than Jennifer’s new boyfriend who refuses to shake hands. Normally, we cover one individual stock in each issue of The Spill. But today, we thought we’d try something a little different. We wanted to dive into an exchange traded fund (ETF) that investors commonly use to fight inflation: iShares TIPS Bond ETF TIP While most people think you want to buy this ETF to protect against inflation, we’re going to make the exact opposite case. So stick with us because it’s about to get wild in here! iShares TIPS Bond ETF TIP For those who aren’t aware, the US Treasury issues Treasury Inflation-Protected Securities (TIPS). These are US treasury bonds that adjust their coupon payments based on the consumer price index (CPI). The TIP paid a dividend yield of 3.65% over the last 12 months and currently yields 2.45%. So, you would think you would want to own these since they protect against inflation. The problem is you would be late to the party. Take a look at the monthly chart of the TIP. Apparently, a lot of folks have bid up the prices of TIP to some of their highest levels. In fact, so many people have bought into the TIP that it actually yields negative real yield. What do we mean by this? We’re saying the yields provided by the investment don’t cover the current rate of inflation. You can actually see this in data provided by the Federal Reserve. Take a look at both charts in 2013. As real yields turned around the TIP ETF took a nosedive. Generally speaking, real yields are mean-reverting. That means they tend to correct back towards the average over time. Since we’re at historically and relatively negative interest rates, it’s reasonable to assume they would bounce back at some point in the next couple of years. And Fed raising interest rates is likely going to be the trigger for that. So, while TIP could go higher in the short-term, over the next couple of years, it’s very likely to fall from current levels. Here’s a better bet When interest rates increase, one sector does extremely well – financials. Regional banks actually benefit MORE than large ones. You see, banks pay depositors based on short-term interest rates. But they lend based on long-term interest rates. The spread is what’s known as net interest margin. And, when the Fed raises interest rates, longer-term interest rates tend to move more than shorter-term rates. That means banks make more money on their loans. So, why are regional banks better than the big guys like Citigroup (C) or Bank of America (BAC)? Because regional banks tend to make a larger percentage of their income from net interest margin. For example, JP Morgan (JPM) makes somewhere around 50-60% of its revenues from net interest. Small regional bank Heartland Financial (HTLF) makes a whopping 82% of its revenues from net interest income. That brings us to the SPDR Regional Bank ETF KRE. Rather than doing the homework on individual regional banks, the KRE gives you exposure to a wide set of companies. Year-to-date, the ETF is up nearly 45% and pays a nice 2.16% dividend yield. Heck, even though it trades at $75 it was down just above $50 in early September. The bottom line: Even though TIP is popular, the risk/reward is extremely poor. We prefer regional banks going into 2022. |