|

Proprietary Data Insights Retail Investors Top Department Store Stock Searches in Nov.

|

What we’re watching

|

|

Macy’s has turned things around through aggressive omnichannel growth.

|

|

Stock Analysis |

Macy’s Might Be Worth A Second Look |

Department stores were on the verge of collapse. Years of underinvestment in digital shopping left them woefully behind the curve. That’s all changed with aggressive omnichannel growth. And one company shines in particular – Macy’s (M). The stock topped our list of Department Store stock searches by retail investors according to our proprietary data. After we read through the company’s Q3 results, it’s easy to see why. Comp sales jumped more than 50% year-over-year with EPS flipping from -$13.20 per share to +$2.17. With online sales growth still in its infancy, we think there’s more room for this retailer to run. Plus, it’s pretty darn cheap at these price levels. Macy’s Business Known for its department stores, namesake brand, Bloomingdale’s, and Bluemercury, as well as its Thanksgiving Day Parade sponsorship in New York City, Macy’s faced serious threats in the last decade. Consumers shunned traditional department stores in favor of niche merchandise and online shopping. In February 2020, management outlined its three-year Polaris Strategy to makeover the entire business to better adapt to the new retail ecosystem. It included the following 5 pillars:

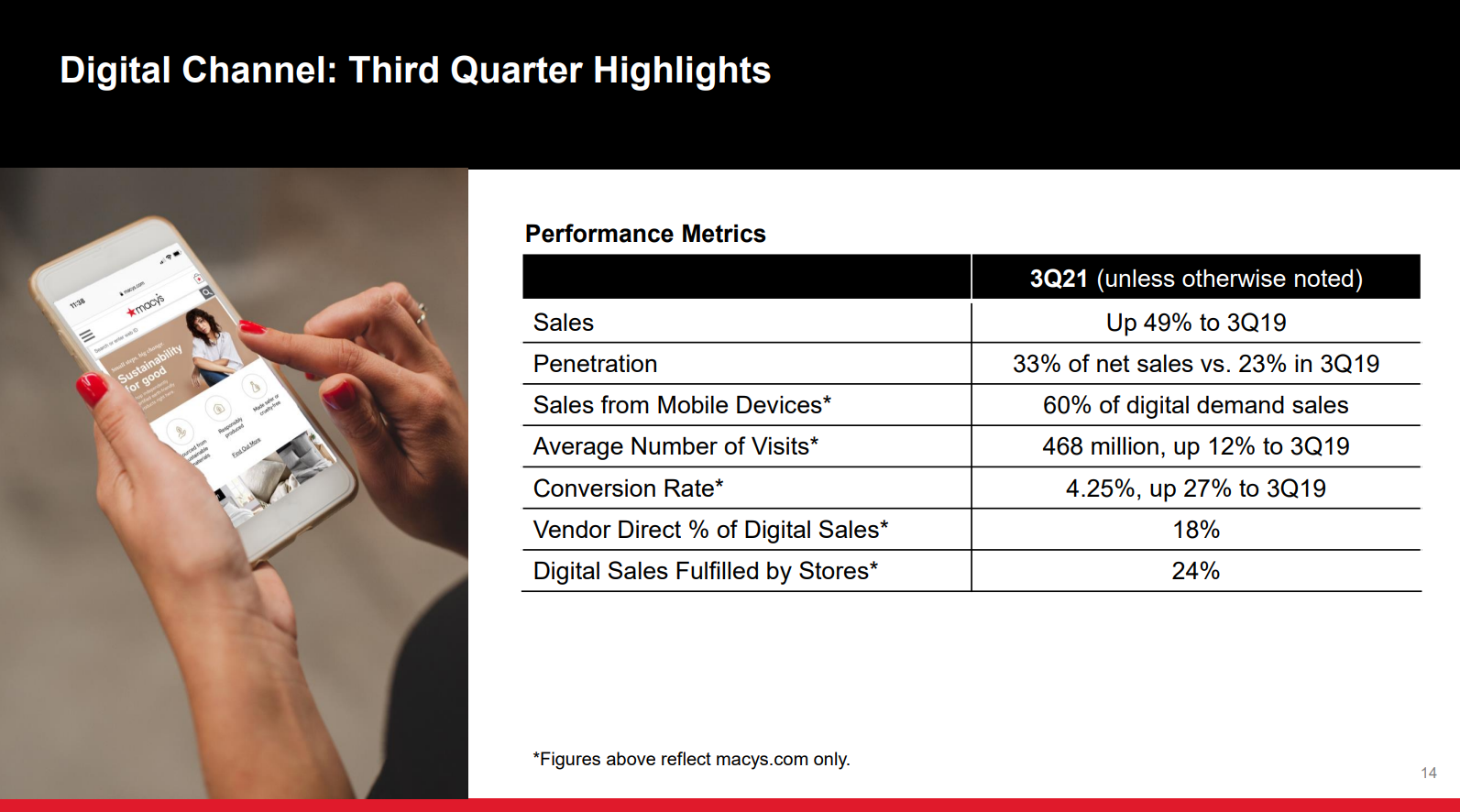

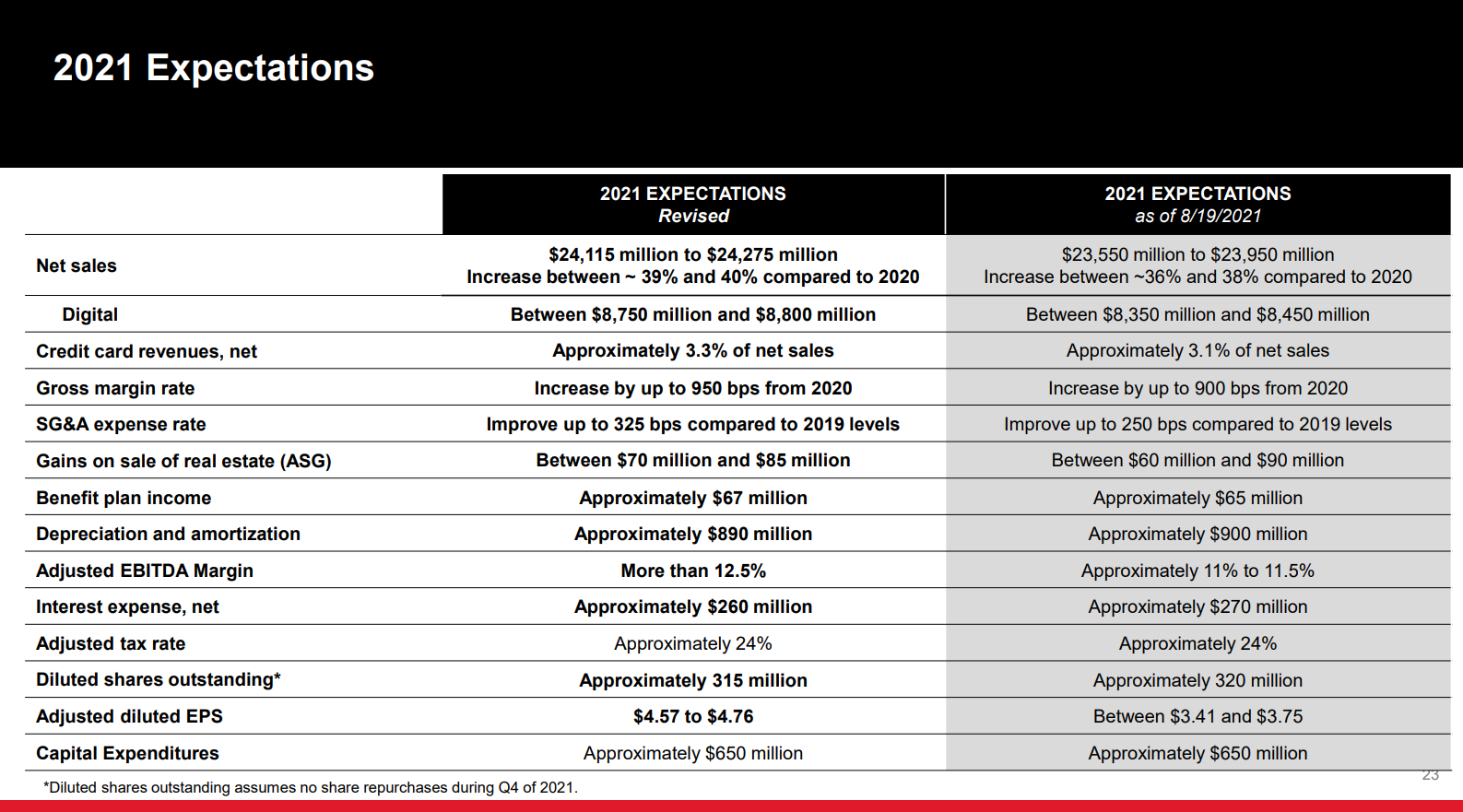

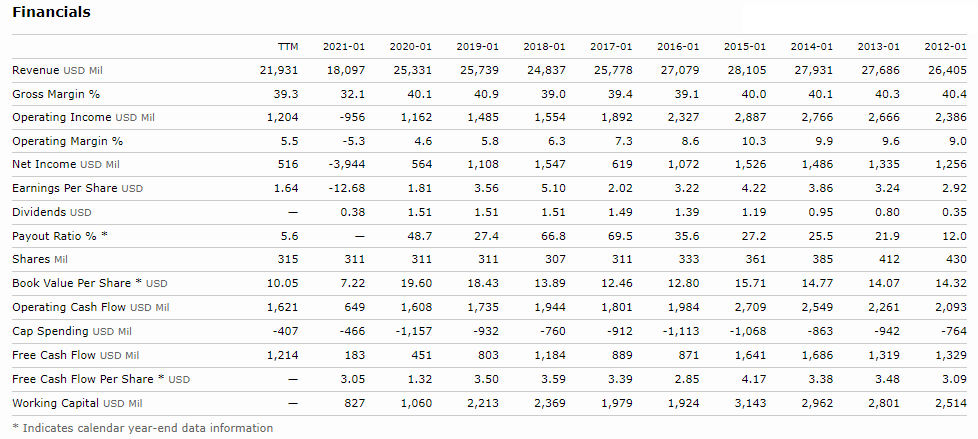

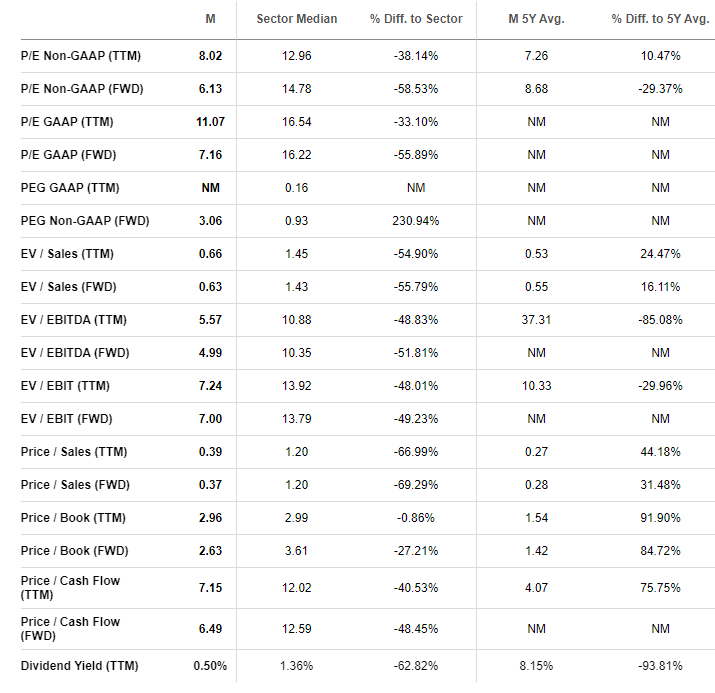

Within these categories, Macy’s is banking on its off-price Backstage locations, Vendor Direct shipments, as well as store pickups. Q3 results highlight strong gains in these areas. With digital sales only accounting for 33% of net sales, we see massive upside in this common growth vertical alone. Current omnichannel updates include everything from a 3D room planning to PayPal and Venmo payment options. Lastly, Macy’s raised its 2021 expectations in Q3 across the board. Adjust EPS are now expected to land between $4.57-$4.76, which would give the company an adjusted price-to-earnings (P/E) ratio of 6x-7x. Financials As we take a step back and look at the last decade, we find Macy’s revenue growth stalled in 2015. Along with many department stores, Macy’s found itself amidst a transition away from broad brand product offerings to exclusive online shopping. Yet, management didn’t take serious action for another 5 years. During that time, Macy’s shares plunged from $70 to $15 BEFORE the pandemic. As the market rebounded and the Polaris Strategy took hold, shares managed to stage a comeback from $4.38 to $37.95 before pulling back below $30. The Polaris Strategy already bore fruit as gross margins hit 42.62% and 43.27% compared to a high of 42% prior to the pandemic. Operating margins were really stunning as they climbed to 10.44% in Q2 and 8.67% in Q3. Hence the improved EPS forecast. One interesting point – cash flows haven’t necessarily improved. In 2019, cash from operations came in at $1.7 Billion. The last 12 months only generated $1.6 Billion. The big difference is revenues. As a percentage of revenues, operating cash flow jumped from 6.74% to 7.39%. Valuation Turning to the valuation measures, most of them speak for themselves. The only two metrics that don’t beat the sector average are price-to-earnings growth (PEG) forward forecast and dividend yield. The forward PEG likely has uncertainty built into it given that management hasn’t offered guidance for 2022. We’re ok with the lower dividend payout since the company is investing in its transition. However, it should increase in 2024 and beyond as the Polaris Strategy winds down. Now, many of the metrics do appear higher than the 5-year average for the company. That’s to be expected as it went through a significant downturn during Covid as well as a massive restructuring. Our Opinion – 8/10 Macy’s management has a strong plan to transform the company and a clear timeline. With the recent run in shares, we see somewhere around $20 as the optimal entry spot for an investment. |