|

Proprietary Data Insights Retail Investors Top Car Dealer Stock Searches in Nov.

|

What we’re watching

|

|

With car demand higher than ever, AutoNation looks a great buy.

|

|

Stock Analysis |

Why AutoNation Is A Buy At All-Time Highs |

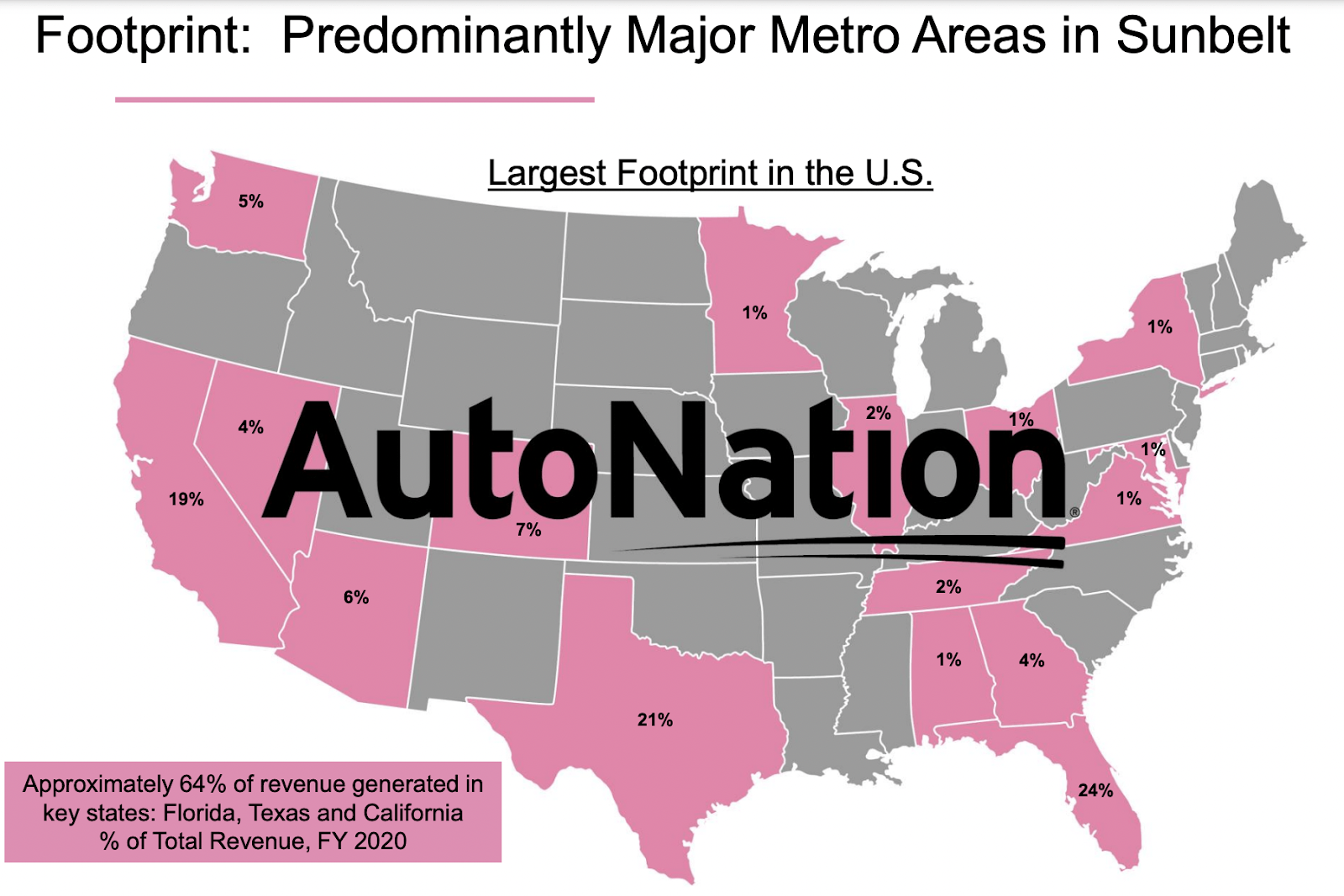

Car demand is higher than ever. Yet, supply chain problems limit car manufacturers from realizing their potential. AutoNation (AN) doesn’t have this problem. As the largest car dealer in the U.S., AutoNation sells whoever gets them cars, be it Ford (F), General Motors (GM), or Toyota (TM). We picked up on the stock when it came in as the #2 car dealer stock search amongst retail investors in November. With auto inventories so low, we expect a multi-year cycle to play out through 2025. And even though AutoNation’s stock is near all-time highs, we think shares might still be a bargain. AutoNation’s Business Despite Tesla’s push to sell directly to consumers, car dealers still hold a ton of juice. AutoNation operates 315 new vehicle franchised from 230 stores in the U.S. Additionally, the company owns 74 collision centers, 5 used vehicle stores, 4 auto auction houses, and 3 parts distribution centers. Core brands account for 89% of the new vehicles the company sells: Toyota, Ford, Honda, General Motors,FCA US, Mercedes-Benz, Nissan, BMW, and Volkswagen. The company operates three segments:

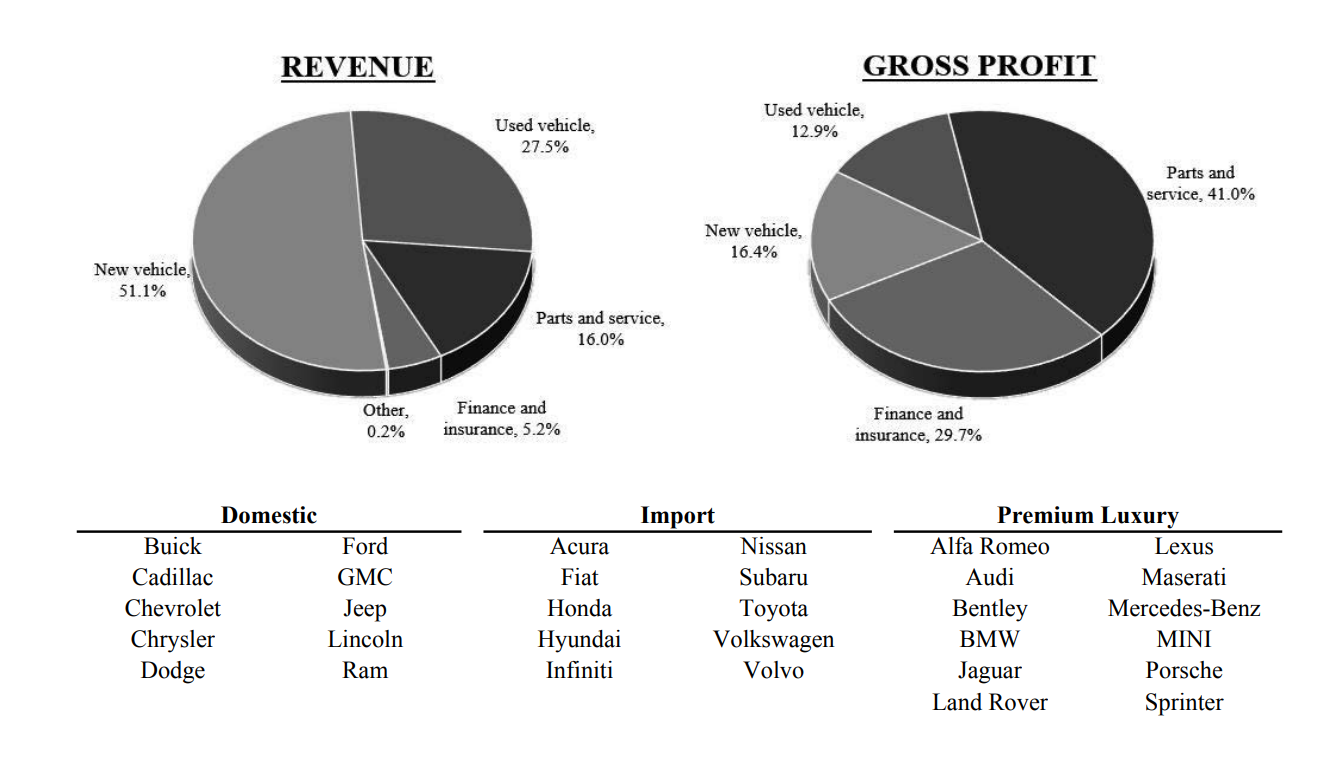

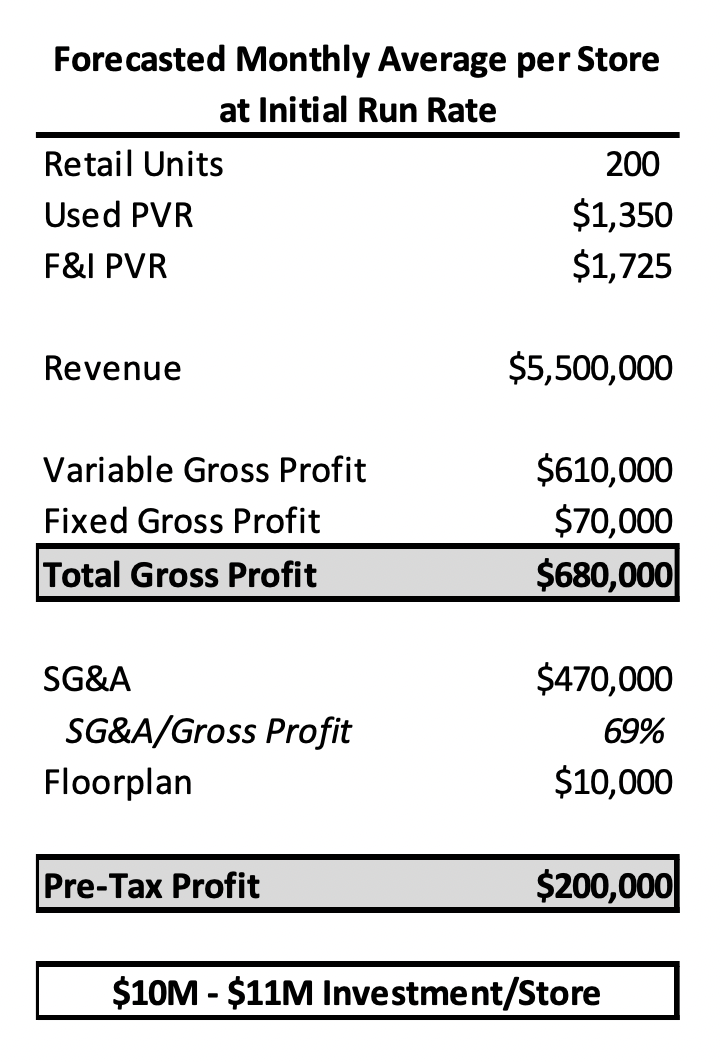

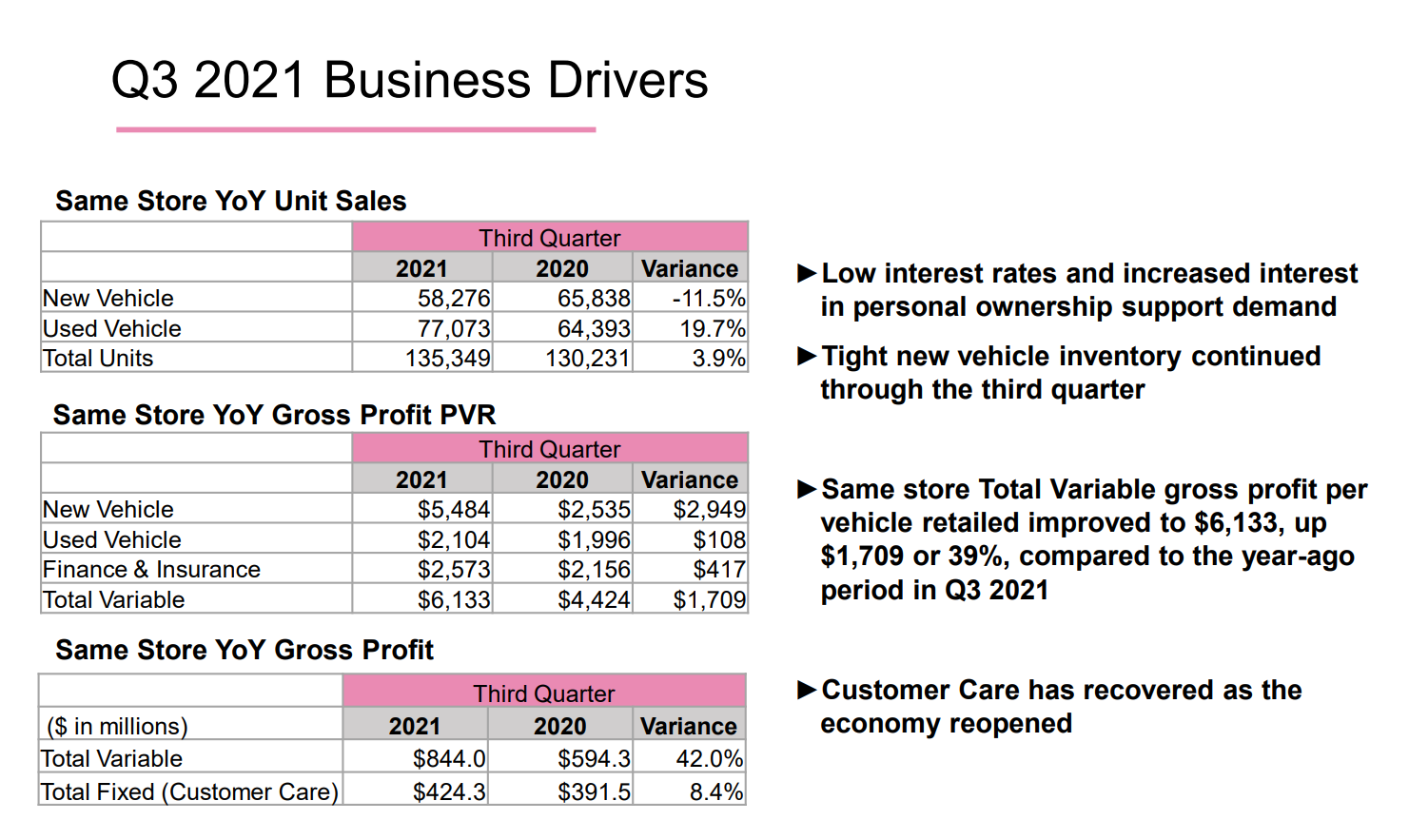

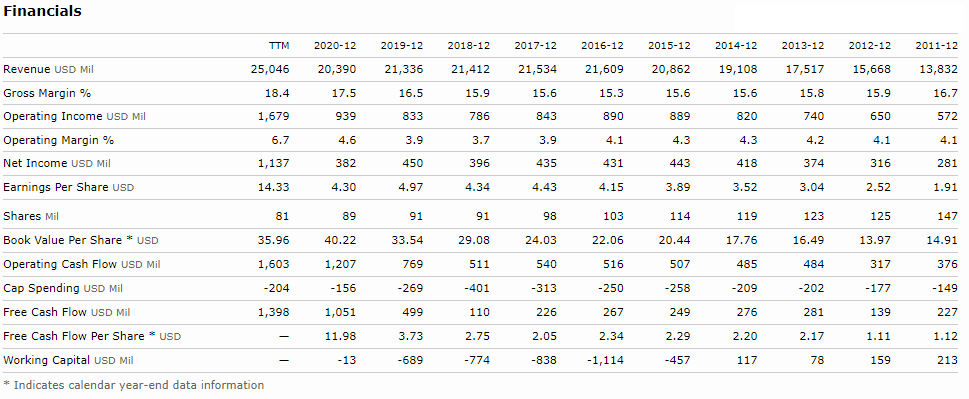

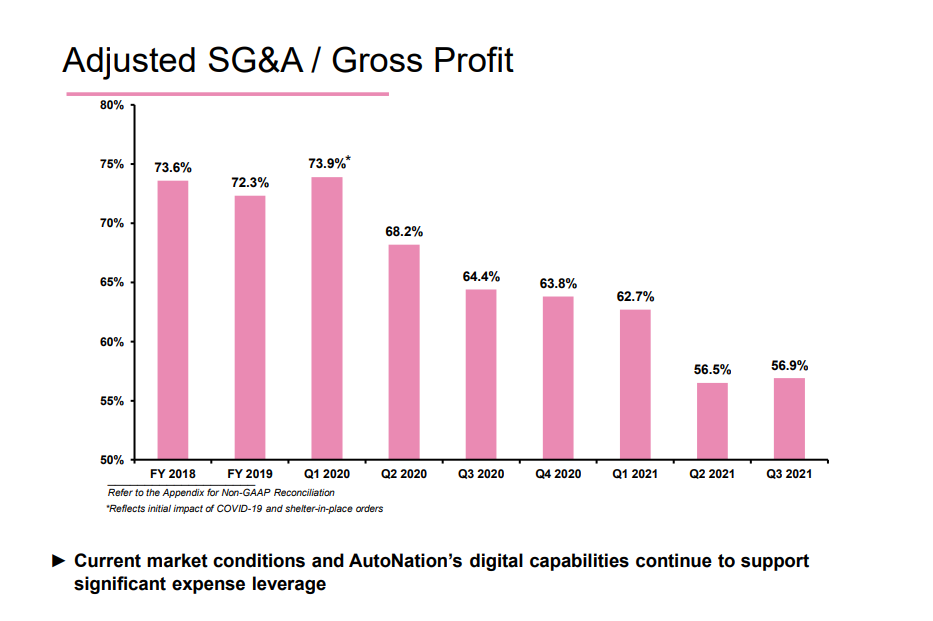

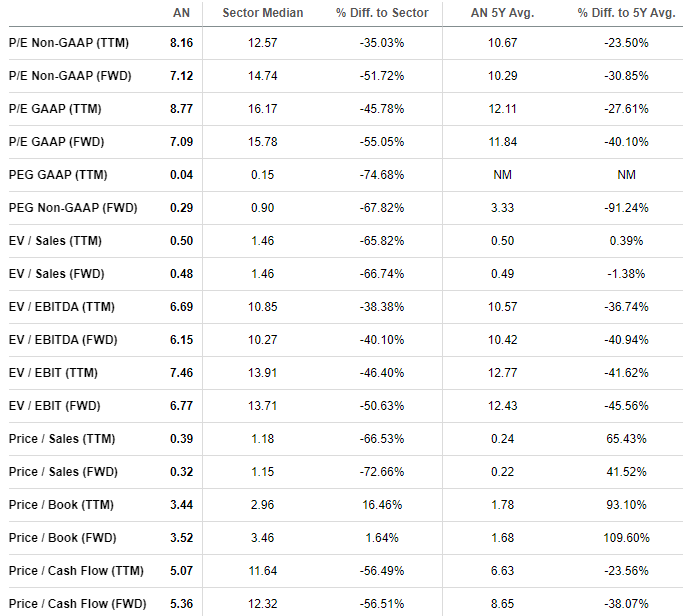

What’s interesting is despite new vehicle sales accounting for over half the revenue in 2020, they only made up 16.4% of gross profits. On the other hand, finance and insurance made up 5.2% of revenues but 29.7% of gross profits. Currently, management is focused on expanding their AutoNation USA. These retail locations are focused on selling and servicing used vehicles. This year, the company has opened six of these with another 12 by the end of the year and 130 by 2026. The proforma for these locations is as follows: Essentially, each store costs $10-$11 Million and would generate ~$2.4 Million in pre-tax profit annually. In Q3, the company saw lower new vehicle sales and higher used vehicle sales. This change in mix led to a massive shift in overall profitability for the quarter. Going forward, as the company expands its sales and service of used cars, we expect margins to continue improving along with earnings. Financials AutoNation’s stock didn’t move much over the last decade as revenues stagnated since 2015. What’s notable is the consistent cash flow and earnings through the years. As margins expanded, cash flow exploded, climbing 5x-6x in the last several years. That puts the company into a strong position to increase their capital spending to fund their future growth. We consider this the most appealing aspect of the stock right now. We’ve also been impressed with management’s commitment to lowering SG&A costs over the last three years. That’s a big reason why EPS has more than doubled over the same period. And yet, as you’ll see in a minute, shares remain incredibly cheap. Valuation Check out these metrics. The only place AutoNation comes up short of the consumer discretionary sector is the price to book, and barely so. Otherwise, from price-to-earnings to price-to-cash flow, the stock appears incredibly cheap. Heck, at 5x cash, the company could buy back all outstanding shares in 5 years. Yet, we expect these numbers to improve as the company invests in AutoNation USA locations and expands its digital presence. Our Opinion – 9/10 Even though shares have quintupled off the lows from last March, we see enough value at the current share price. If anything, the round $100 level would be a nice spot to build a bigger position. |