|

Proprietary Data Insights Retail Top Trucking Searches January

|

|

Stock Analysis |

USA Trucking Keeps on Trucking |

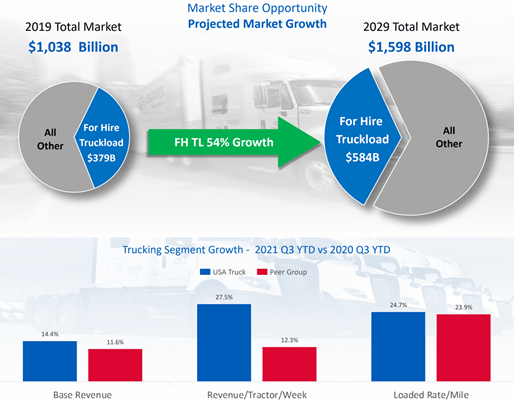

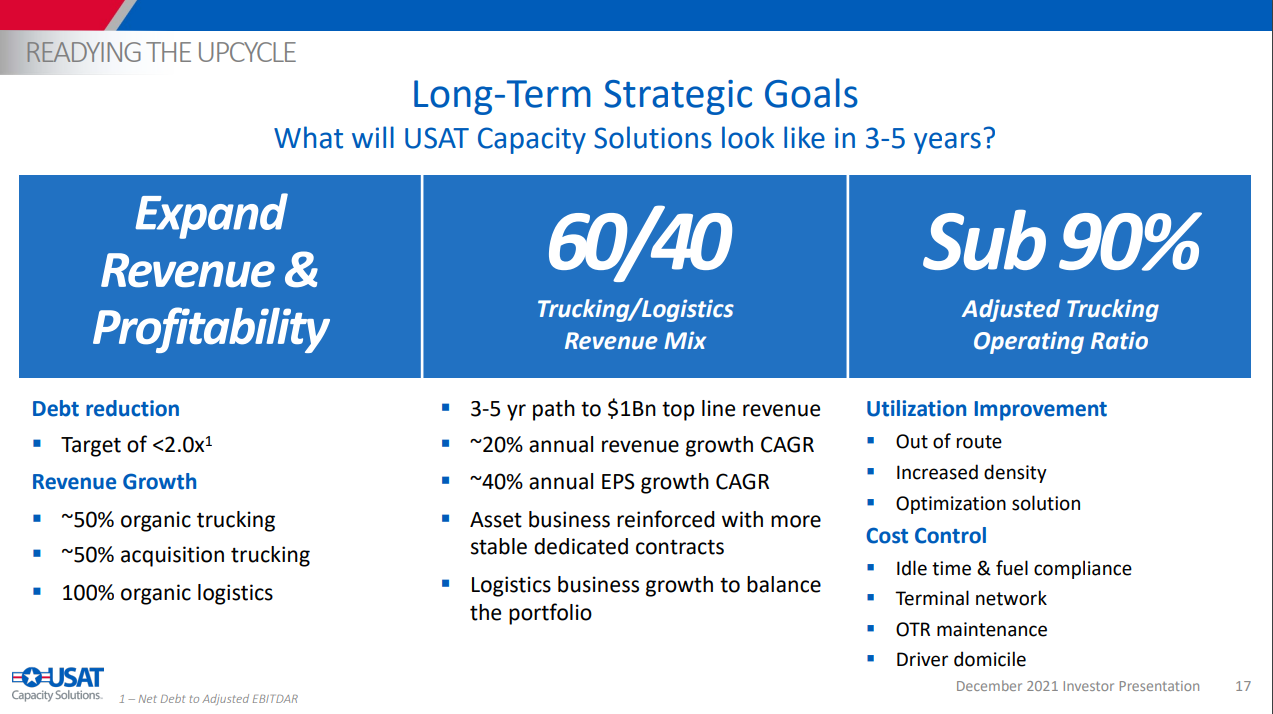

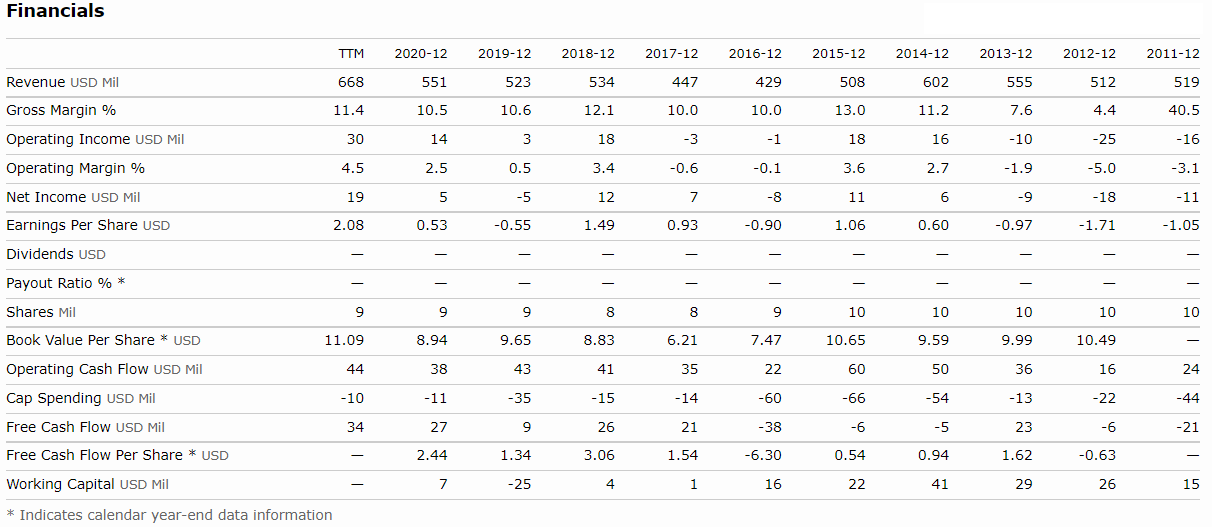

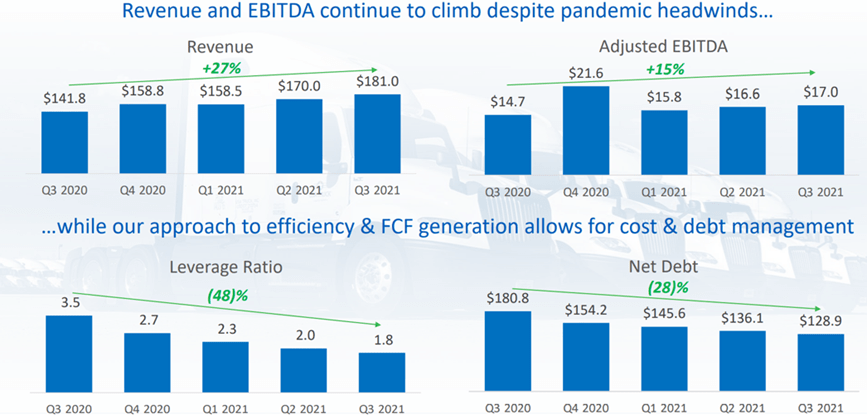

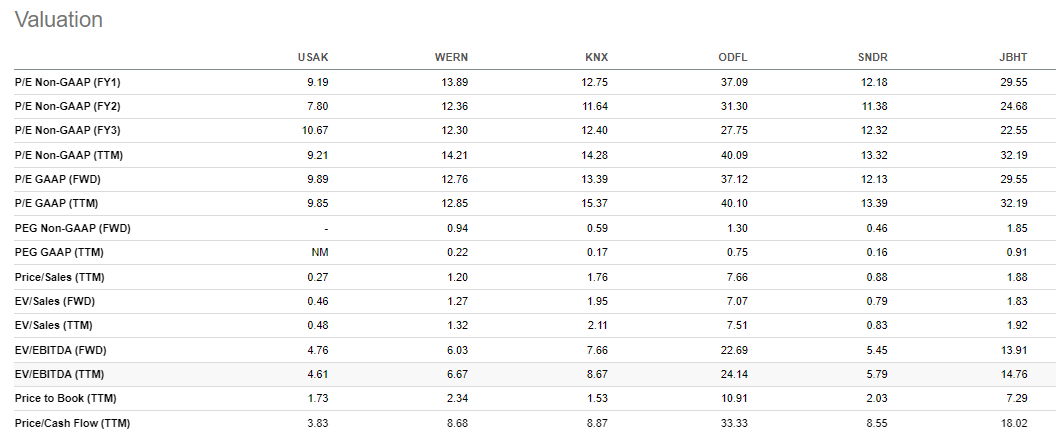

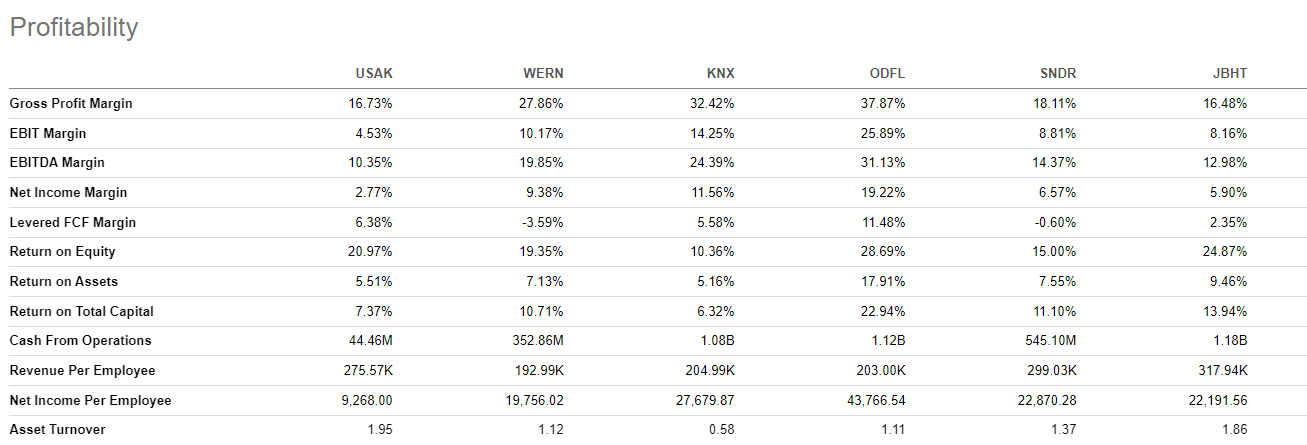

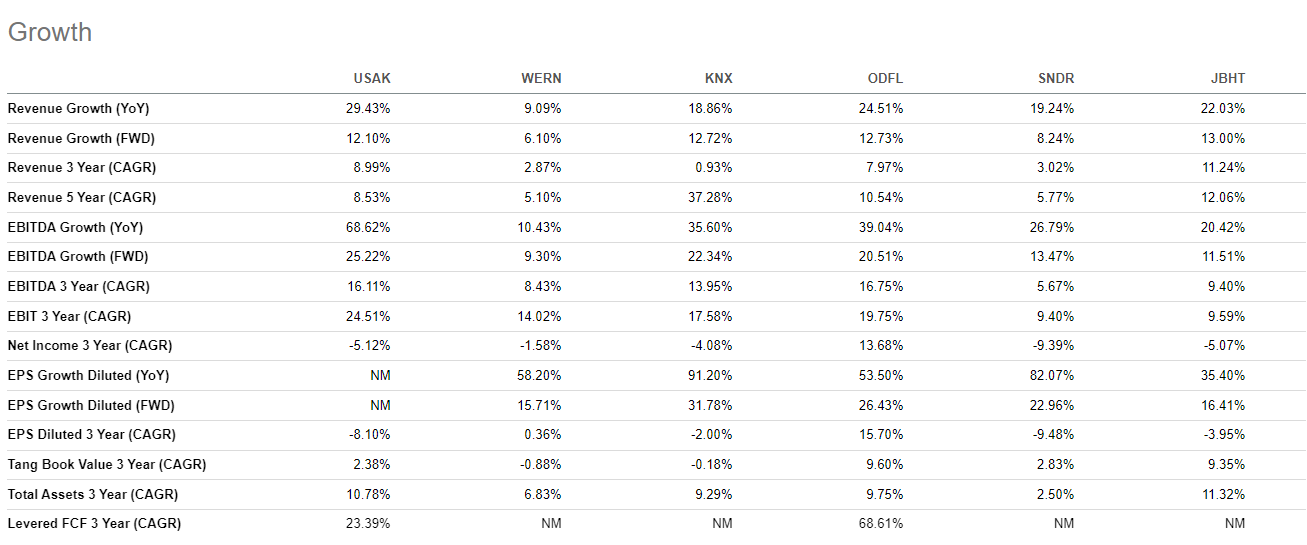

Trucking is in high demand these days. Freight rates have skyrocketed as goods clamor for fewer carriers to move goods. That’s allowed trucking companies to hit some of their best margins in years. With this trend expected to continue, we like USA Trucking’s (USAK) investment potential. As a mid-sized carrier, USA Trucking is large enough to generate operational efficiencies but not so large that it can’t beat average market growth. While it only came in 8th amongst retail’s top trucking stock searches this month, it had one of the best price-to-earnings (P/E) ratios at just 9.8x TTM and forward earnings. And that was just the start… USA Trucking’s Business USA Trucking provides logistics and trucking services within the U.S. and between the U.S. and Mexico. The company’s two reportable segments are trucking and logistics. Trucking includes long-haul and dedicated (local market contracted) services. Its fleet is known for its premium condition, with the average truck age around 29 months at the end of 2020. This segment operates at a 3.4% operating margin. The logistics segment is growing quickly for the company, now representing over 40% of total revenues. This segment operates as a 3rd party logistics operator (3PL) that brokers freight for customers. The logistics segment operates at a 4.3% margin. Looking forward, the company expects ample room for growth in for-hire truckloads. You can also see in the bottom portion where USA Trucking achieves higher revenues in general and on a per mile basis. We like the long-term growth plan set by management at the last meeting. Expanding revenue will be key to share price appreciation. Maintaining sub 09% adjusted operating trucking ratio (ratio of total trucking costs to revenues) will be key to overall profitability. Financials USA Trucking saw revenues fall off from 2014 to 2016 before climbing back to their current record levels. That said, gross margins are up, but not substantially so. This is largely due to higher fuel and labor costs. However, carriers typically adjust their ‘fuel surcharge’ over time, which should pad margins in the near future. But a shortage of drivers is an industry-wide problem that has no quick or easy solutions. Nonetheless, the company has done a remarkable job increasing revenues and earnings during and after the pandemic. We’re also pleased to see the company pay down its debt, giving it a strong balance sheet to make accretive acquisitions. Valuations As we mentioned earlier, the valuation metrics really tell the tale here. When we stack up USA Trucking against its peers, there’s no question its a better value. It’s cheaper than the majority of its peers on every metric. The price-to-cash flow ratio of 3.83 is equally as impressive as the forward P/E ratio of 9.89x. Why might this be? Well, USA Trucking doesn’t deliver the same margins as its competitors. While higher than JB Hunt’s (JBHT) gross margin, USA Trucking is half that of Knight-Swift (KNX) and Old Dominion Freight (ODFL). It also comes in dead last on net income margin. However, it does a decent job on return on equity and isn’t too far behind on return on assets or total capital. But, the company does have solid growth.

To be fair, KNX’s 5-year growth is out of whack because of a major acquisition. Otherwise, the comparisons of the YOY and forward growth do a good job of describing the industry’s current state. Our Opinion – 9/10 All it will take for USAK to get to that next level is better margins and growth. While sounds daunting,ut the company has already put plans in place to make this happen. If they come up short, it’s still a cheap stock. |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |