|

Proprietary Data Insights Financial Pro >$1M AUM Top Stock Searches This Month

|

What we’re watching

|

|

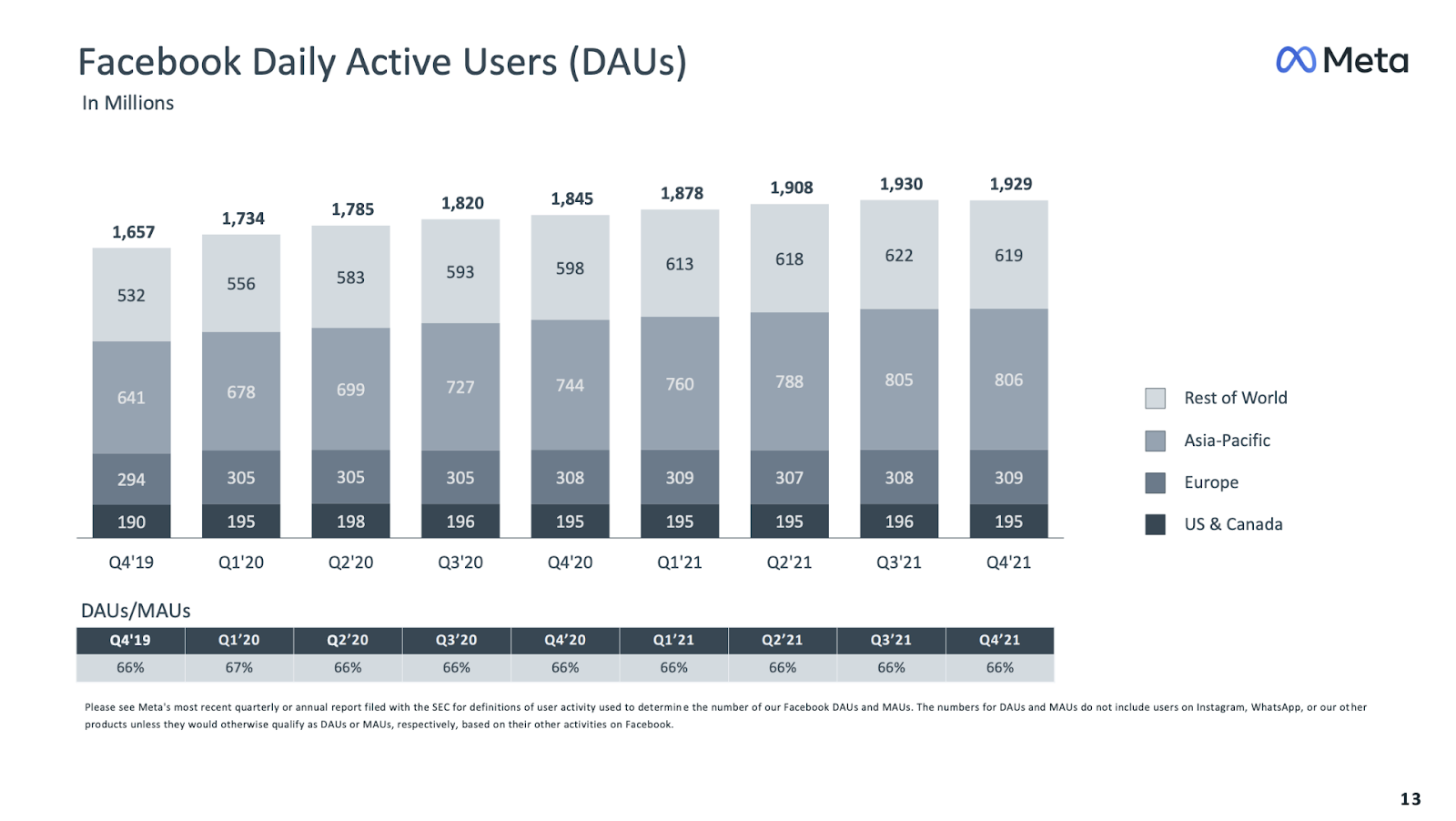

Meta shares have dropped following a decrease in Facebook’s daily active users over the last quarter.

|

|

Stock Analysis |

What is Meta Really Worth? |

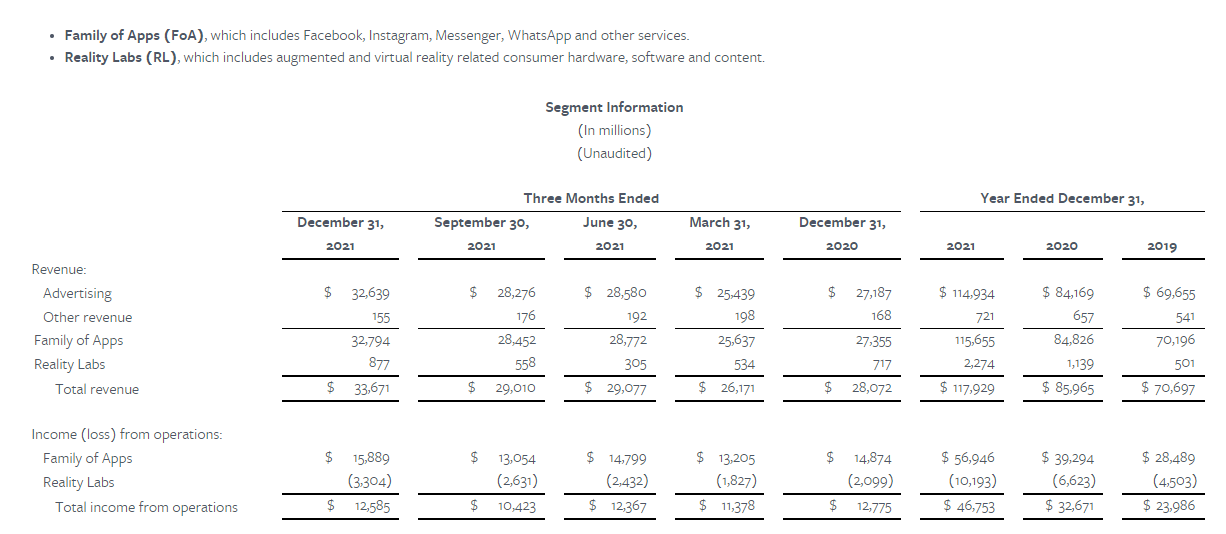

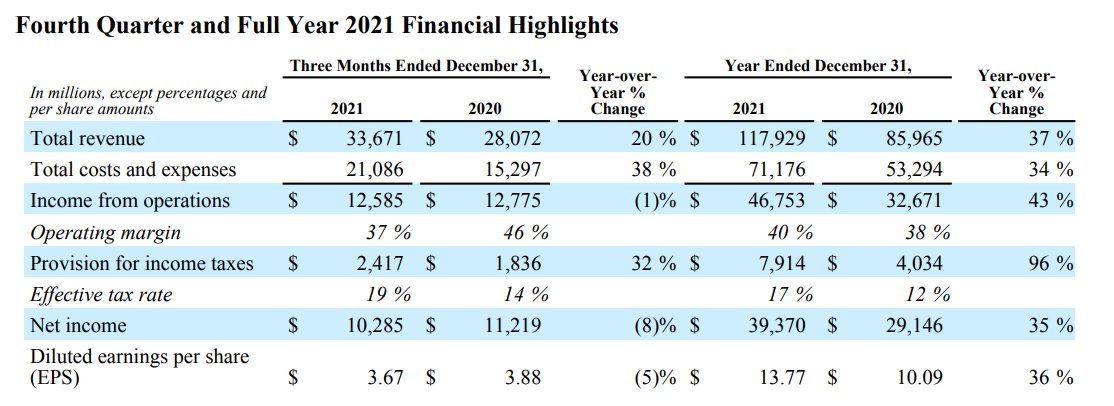

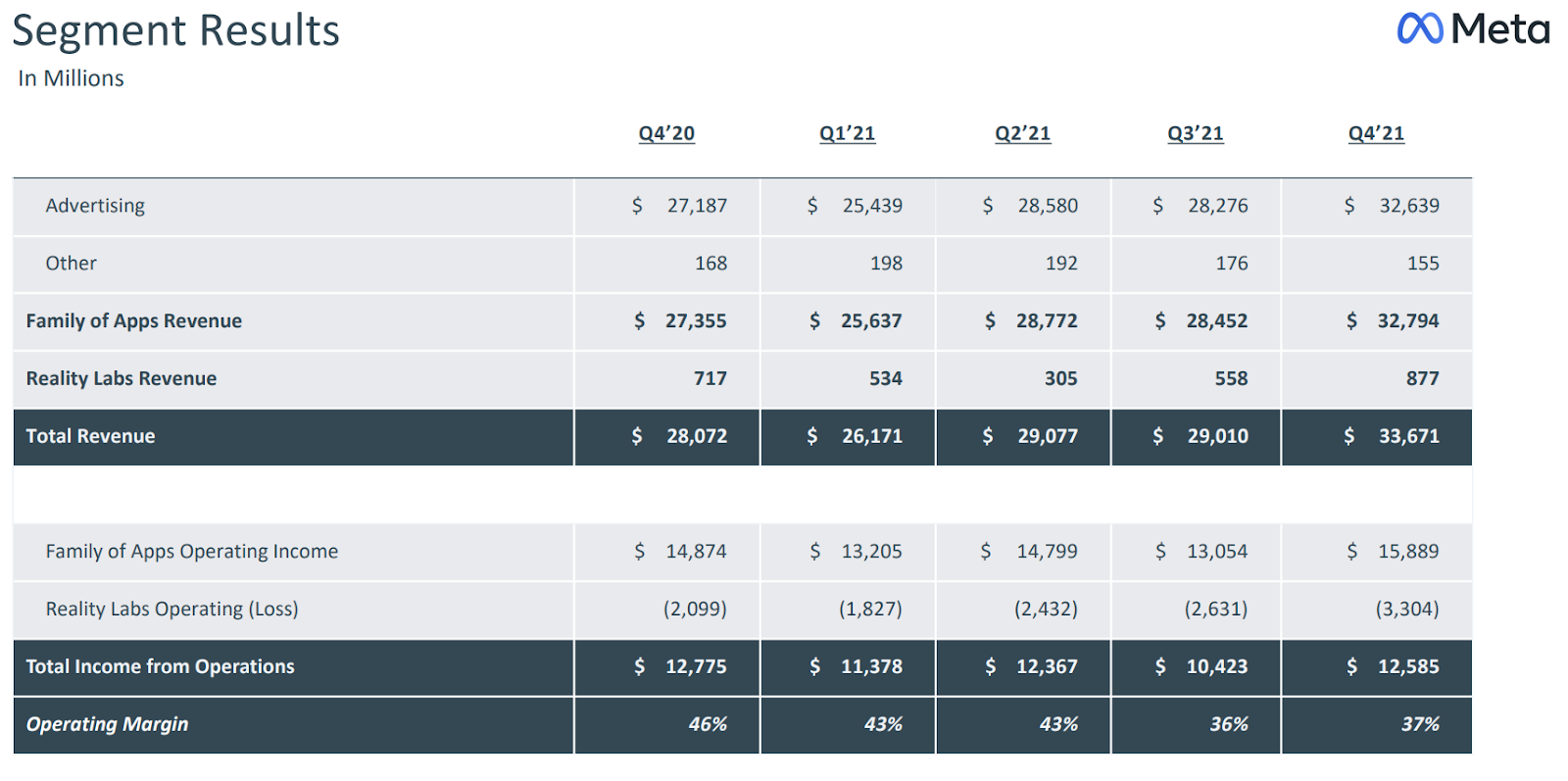

Facebook/Meta (FB) didn’t win over investors with its recent quarterly report. Despite revenue growth of 37% year-over-year, Facebook’s Daily Active Users (DAUs) declined quarter over quarter for the first time in the company’s history. Subsequently, shares sold off more than 25% by the next day’s open. The selloff likely won’t end anytime soon. But where does it make sense to start dipping into shares? Let’s start by understanding what the company’s current business looks like and where it’s heading over the next several years. Facebook’s Business In less than two decades, Mark Zuckerberg took Facebook from a private company that connected college kids to one of the largest companies in the world by market capitalization. Although the company broke out its VR/AI/Metaverse business Reality Labs, nearly all the revenue is generated from advertising. Facebook recently changed its corporate name to Meta as it begins to transition itself towards the new reality. This has led to heavy investments in Reality Labs with growing losses as shown above. These losses are expected to increase in 2022 with that segment unlikely to turn a profit for the next decade. The company also faces significant headwinds including:

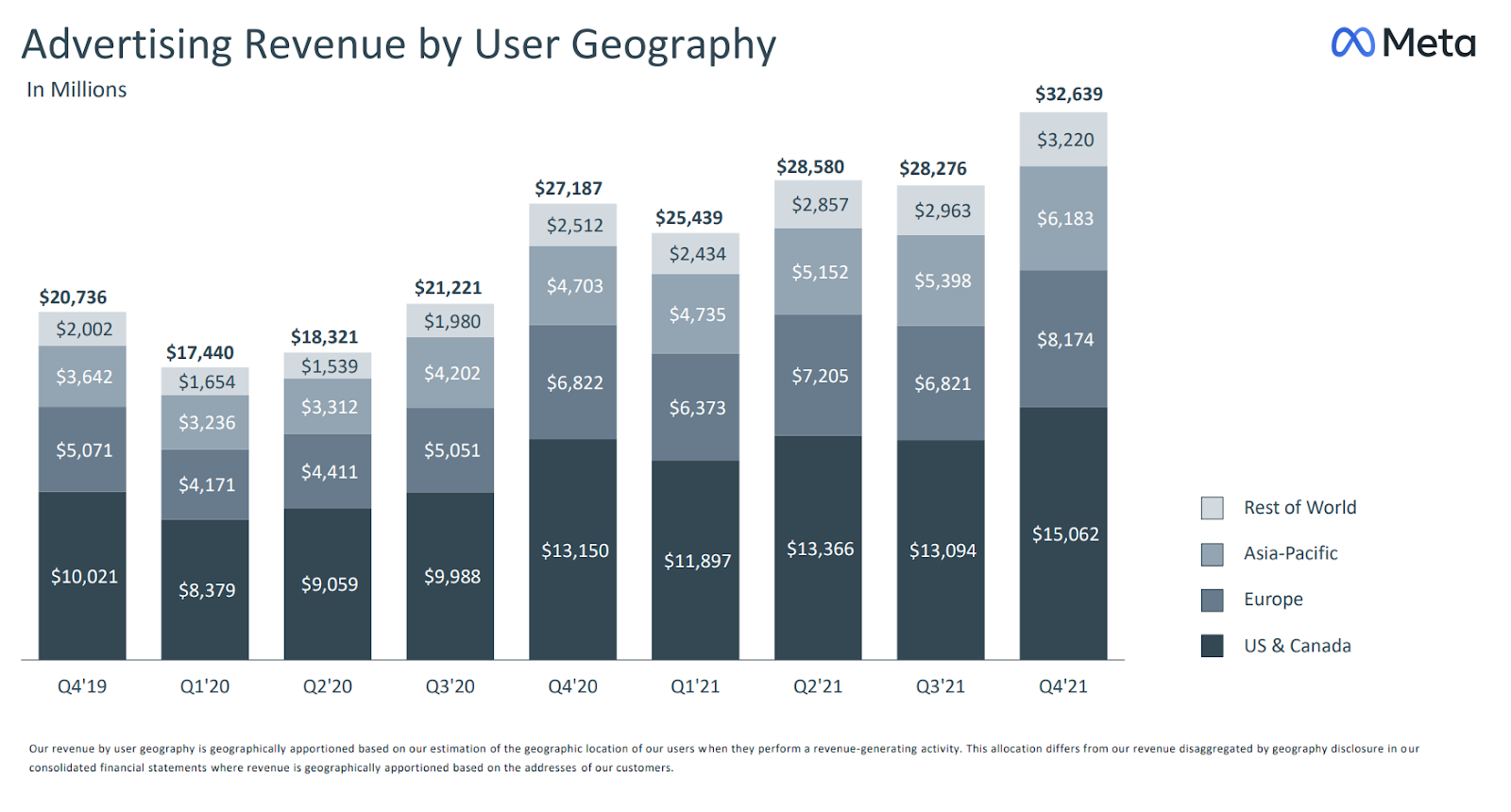

It’s also worth noting that Facebook’s revenues are geographically diverse even with nearly 50% of sales coming from the U.S. and Canada. Financials Analysts questioned future growth at Meta as expenses exploded in the most recent quarter by 38% and 34% for the year. Some of this comes from higher stock-based compensation which increased from $1.8 billion to $2.4 billion last Q4. The majority of it came from the cash burn to fuel Reality labs which are now projected to generate annualized losses of $13.2 billion. That’s led to operating margins getting absolutely obliterated over the last year. To give you an idea, from 2016 to 2018, Facebook regularly hit operating margins of over 45%. This excess operating expenses comes at a time when revenue growth is likely to slow to its lowest levels in years. Valuation With the company’s most recent earnings and major selloff, shares are trading at 17.4x earnings, which are expected to keep growing next year. All in all, that’s pretty cheap even if growth does begin to slow down. In the last year, Facebook generated $20 per share in operating cash flow and $13.33 per share in free cash flow. At current prices, that equates to 12x operating cash flow and 18x free cash flow. That said, we do expect free cash flow to decline some over the next several years as the company invests more in its Reality Labs segment. Our Opinion – 6/10 There’s a lot of near-term risk to Facebook’s stock. That said, it becomes cheap at $200 per share and an absolute steal at $150 per share. Keep in mind, Facebook isn’t going to disappear next year and advertisers will eventually begin to spend again. But, the company’s high growth days may be behind them. |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |