|

Proprietary Data Insights Proprietary Data Insights

|

What we’re watching

|

|

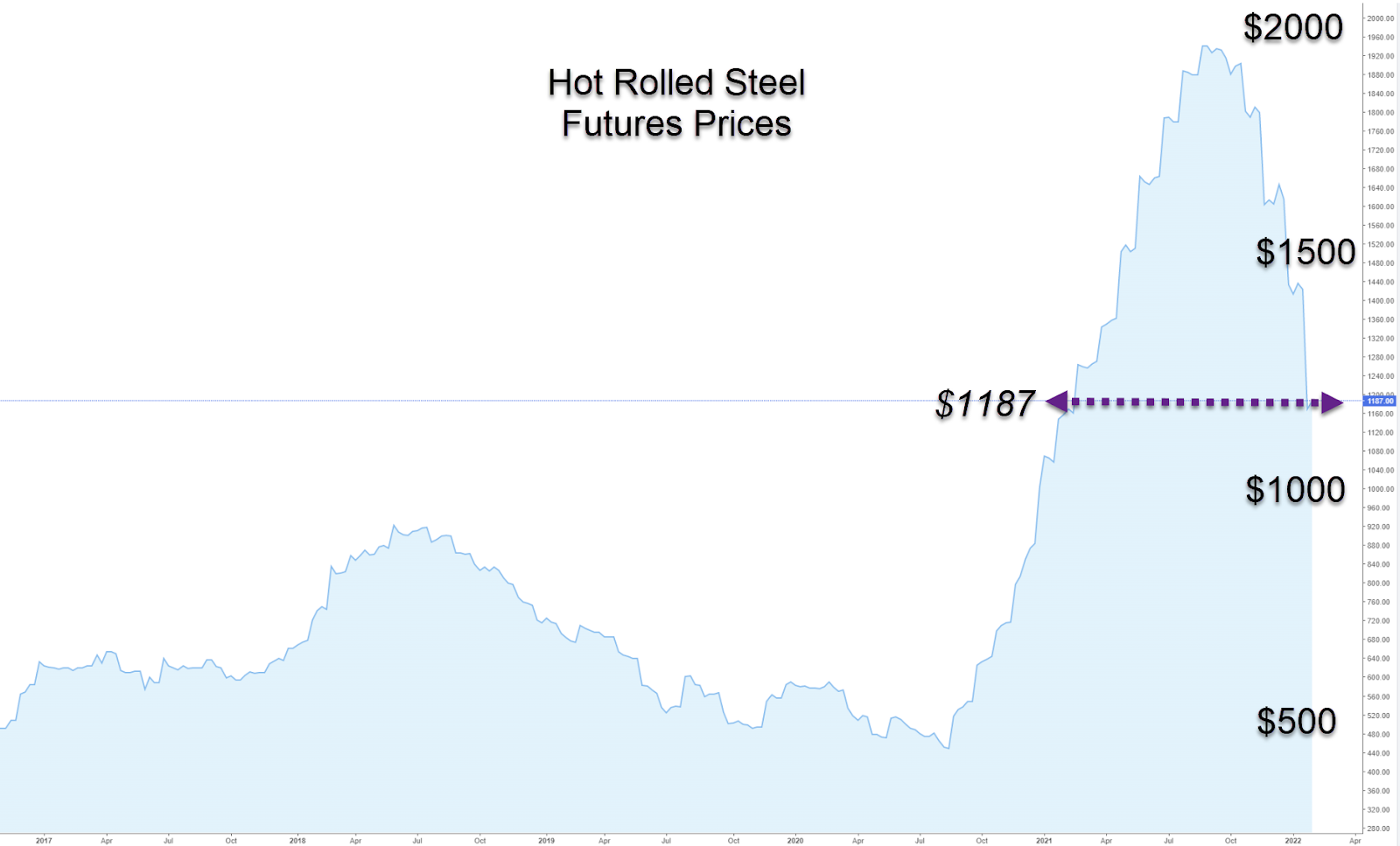

With steel prices through the roof one of the USA’s oldest companies is having a renaissance.

|

|

Stock Analysis |

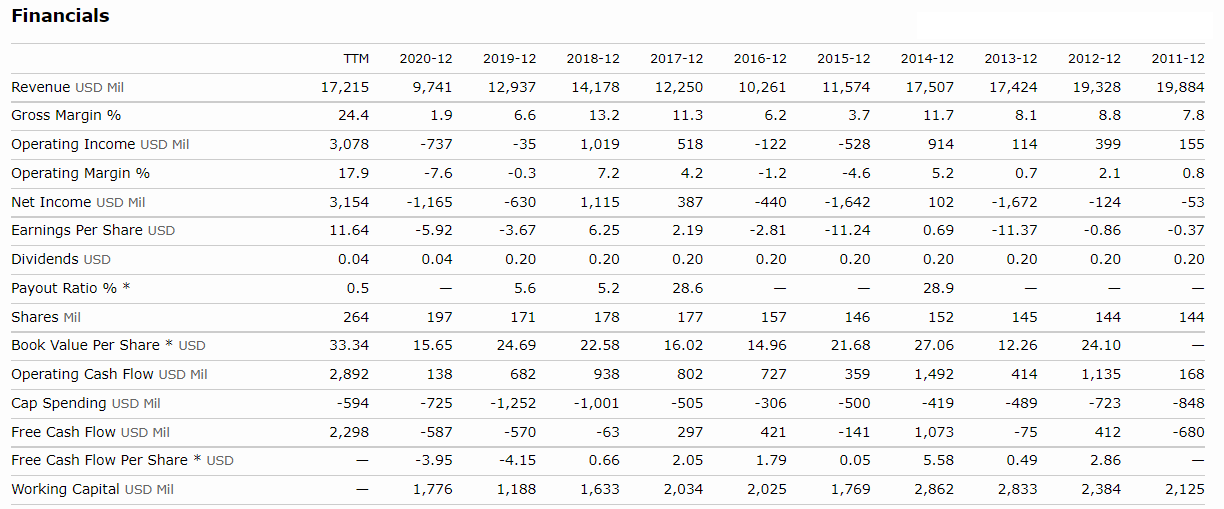

US Steel Oozes Cash |

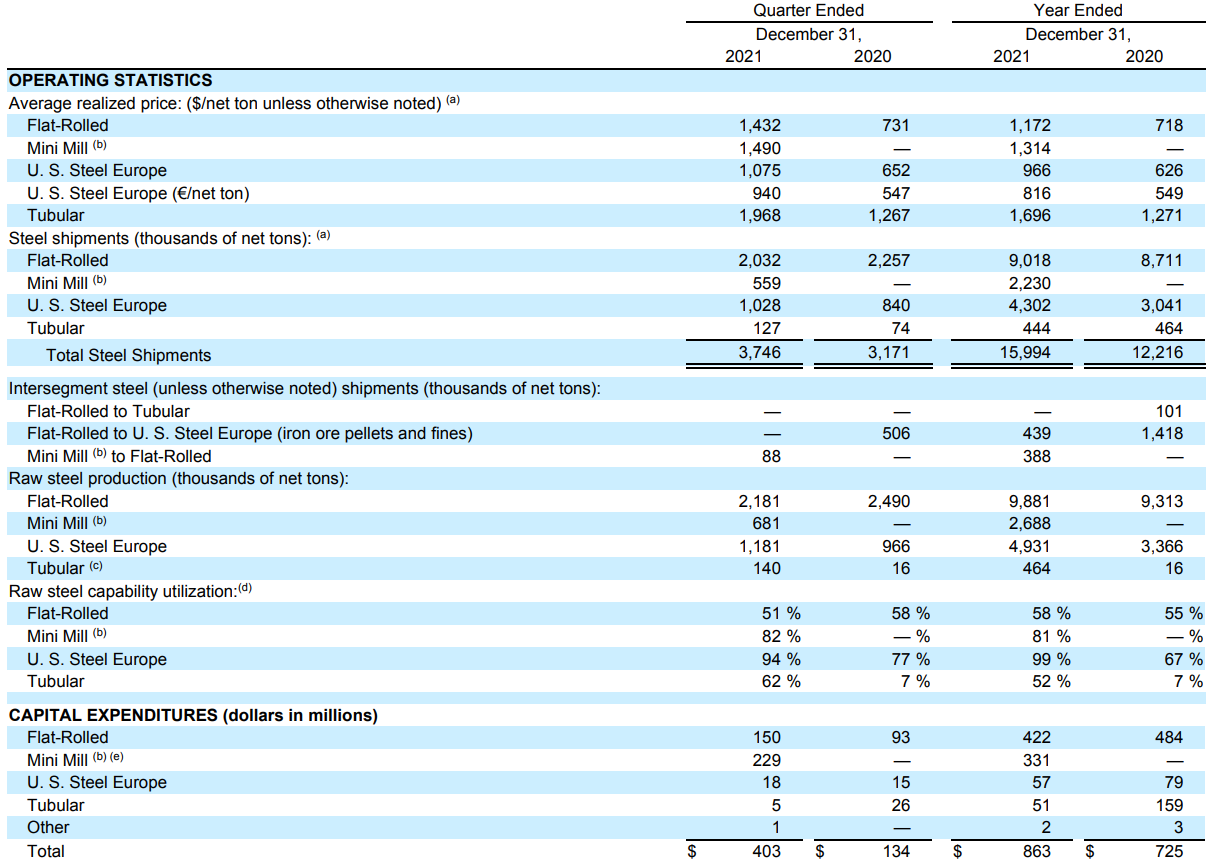

One of the oldest companies in America is having a renaissance. With steel prices through the roof and unabating demand, US Steel (X) generated $4 billion in operating cash flow and $3.2 billion in free cash flow. Per share, that comes out to $15.26 and $12.21 per share respectively. Right now, the stock trades just above $22. Basically, with all the cash the company generated last year, if it pulls off the same feat this year, it could buy back all its stock! That’s why we’re surprised that financial pros only searched for this stock 128 times in the last month, less than half the searches for Cleveland Cliffs (X). And that’s not to say Cleveland Cliffs is a bad stock. But as we’ll show in our valuation section, it doesn’t hold a candle to US Steel. US Steel’s Busines The nation’s first $1 billion-plus company, US Steel Corp was started bty JP Morgan and Andrew Carnegie more than a century ago, becoming a symbol of industrial America. The company was added to the Dow Jones Industrial Average on April 1, 1901, the same day it began trading on the New York Stock Exchange. Fast-forward to July 1, 2014, and the company was removed from the S&P 500. Today, the company has benefited from skyrocketing demand for steel sending prices for the gray metal up across the board. US Steel reports in five major segments:

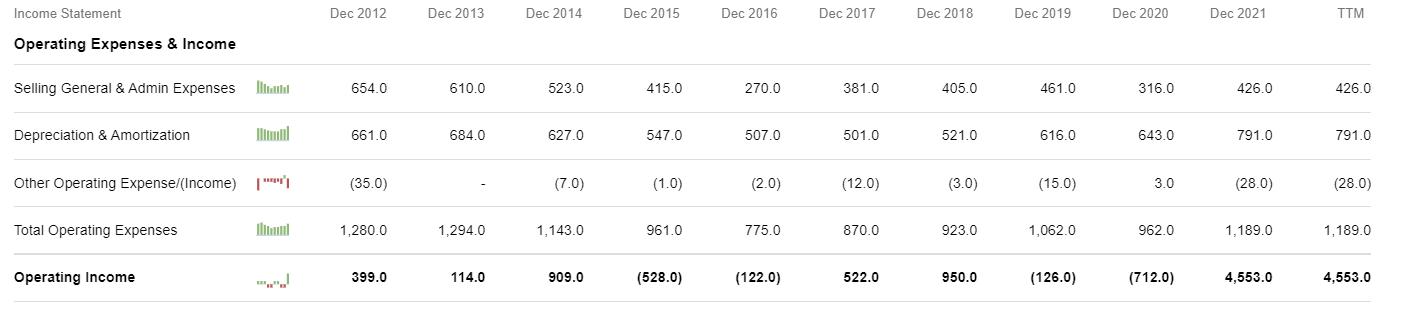

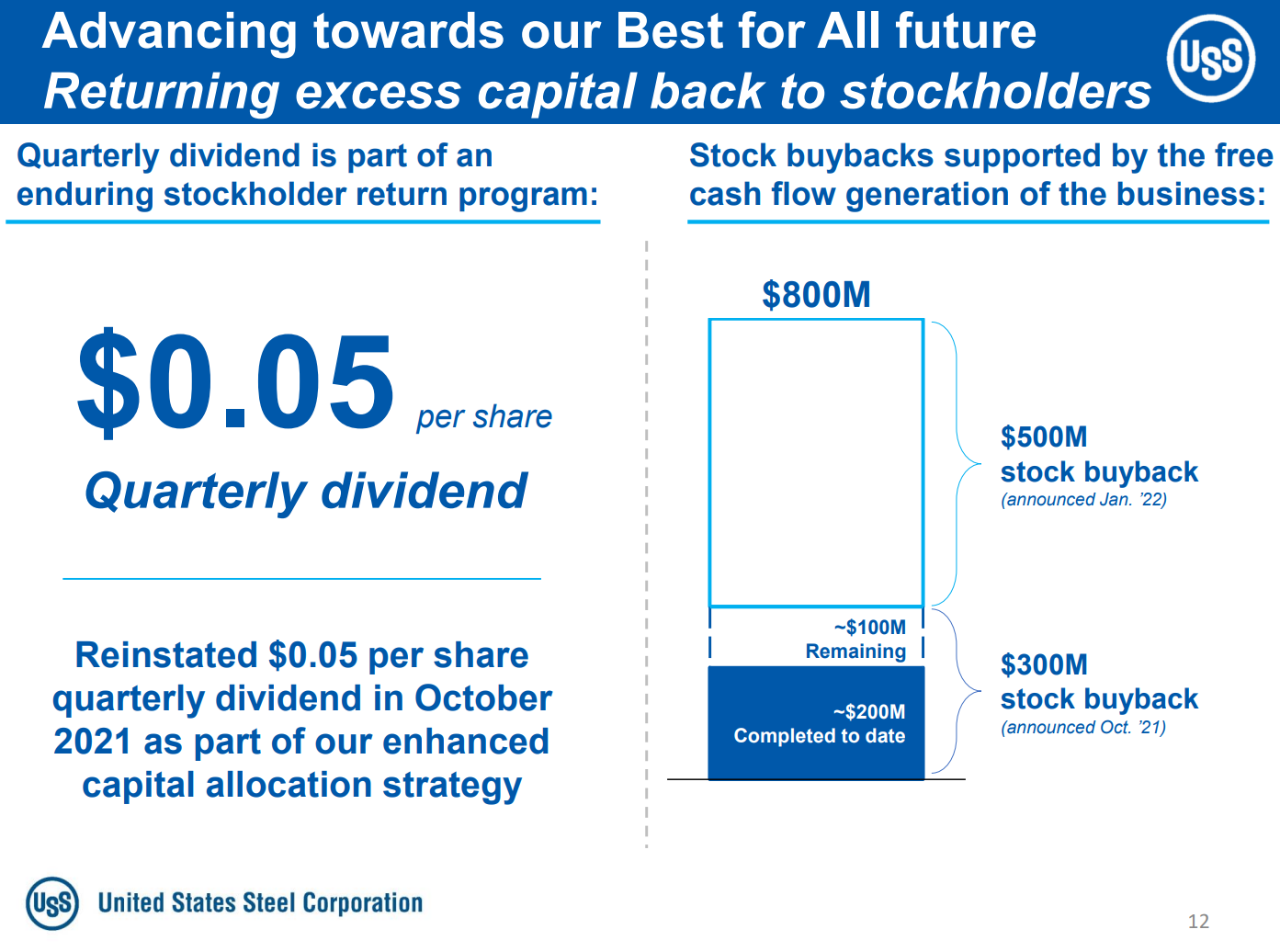

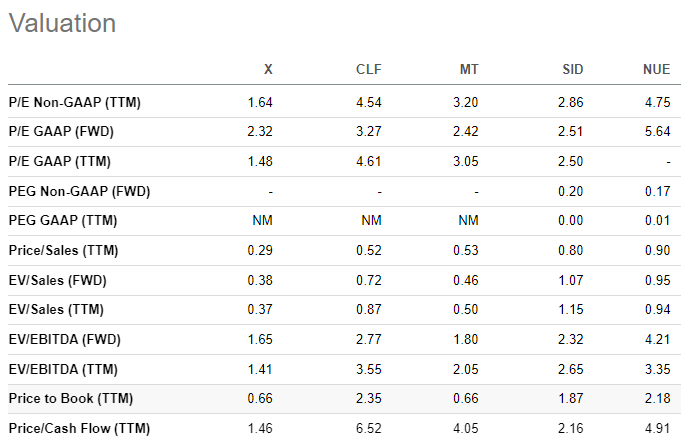

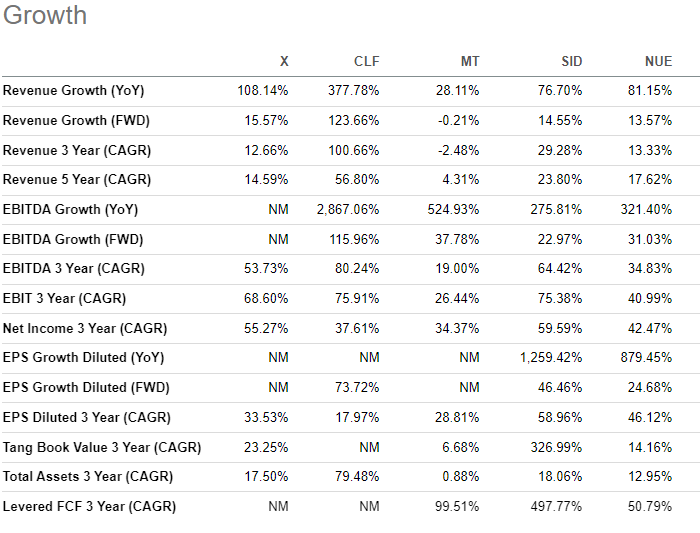

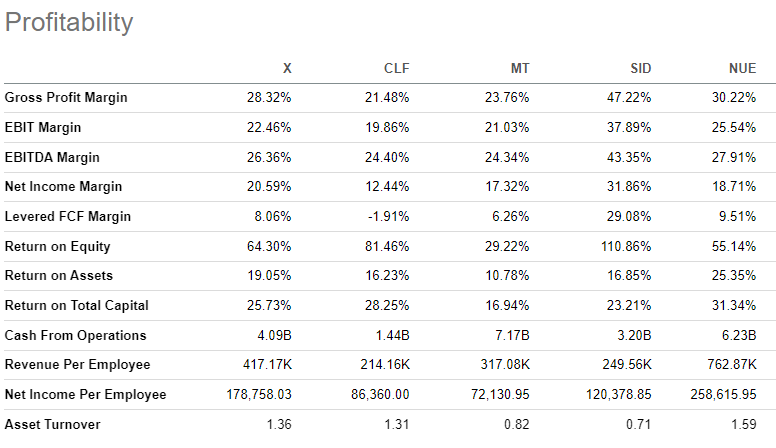

Despite a recent selloff, steel prices for hot rolled steel, and all other steel products really, remain at historically high levels. With the infrastructure plan passed in the US and a push to build more domestic manufacturing capacity, we expect steel prices to continue to remain high even if China’s economy falters. We also want to point out the incredible amount of volume pushed out in 2021 as well as the excess capacity that still exists in the flat rolled segment. That leaves significant room to boost production in the coming year. Financials When we look at US Steel’s financials, it becomes plainly obvious that the higher sales prices helped push operating margins to historic levels. Yet, it should be noted that management’s focus on operational efficiency and cost measures have pushed SG&A expenses below 2019 levels despite higher output. With the high amount of cash being generated, management reinstated a modest quarterly dividend while planning to spend nearly $500 million on stock buybacks. Lastly, we want to highlight $2.522 billion in cash on the balance sheet against modest long-term debt of $3.863 billion. Valuation At the start of the article we claimed US Steel demolished its peers. Here’s the data. In every category US Steel is the cheapest or tied for the cheapest. The PE ratios looking at the last 12 months and forward are insanely cheap, even with the steel stocks themselves trading at a huge discount. On the growth side, US Steel doesn’t necessarily have the top metrics for revenue or EBITDA. But then again, this isn’t a high growth industry. It’s driven entirely by supply and demand. What we feel is more telling are the profitability measures. Although US Steel isn’t the top stock on every margin, they still boast fantastic gross and net income margins as well as incredible returns on equity, assets, and capital. Our Opinion – 9/10 We love everything about US Steel. As long as steel price remain elevated, they’ll continue to generate oodles of cash. Our ideal stock price is $20. |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |