|

Proprietary Data Insights Financial Pros Surging Stock Searches This Week

|

||||||||||||||||||

|

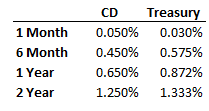

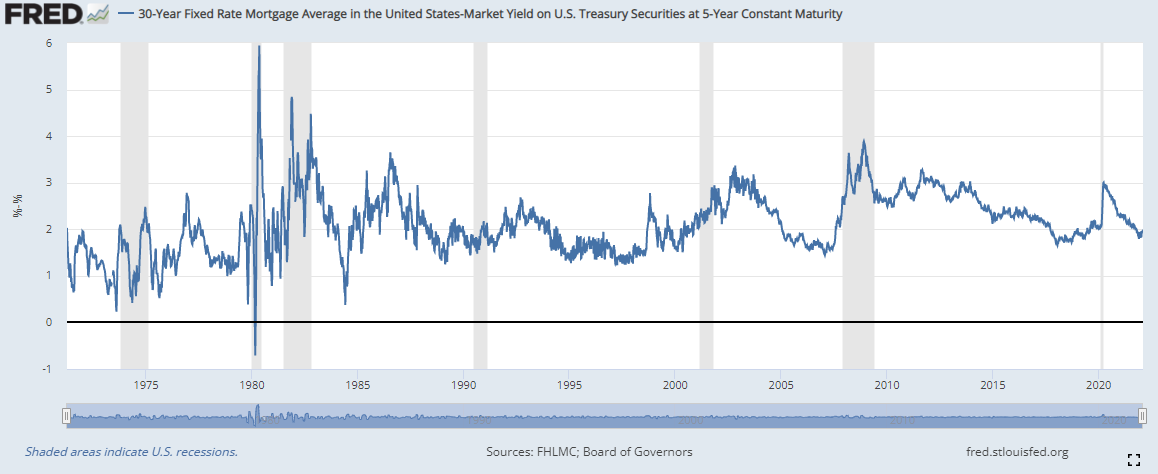

Screw Bank CDs If you’re one of those folks who likes to put extra cash in certificates of deposit (CDs) at banks…don’t. A 5-year CD pays 1.3% at best right now. It doesn’t take long and you can go out and purchase a 5-year US Treasury bond that pays 1.8%. That’s nearly 0.5% higher! True, it doesn’t come with the insurance you get with a CD account. But let’s be real here, has the US Government ever defaulted on its loans? No. If it does, outside of ridiculous political machinations, we have bigger problems. Plus, Treasuries are one of the most liquid markets in the world making it relatively easy to get in and out of your holdings. Don’t want to hold for that long? Here are some other rates to consider: Now, there are some pros and cons to each. CDs tend to lock you into the rate for the given period, have a minimum required deposit that can be as little as $500 up to tens of thousands and will charge you for ending the account early. But they come with FDIC insurance in most cases. Treasuries don’t have penalties for exiting your position early. However, they can require minimum purchases of lots that can be tens of thousands of dollars. Point is, don’t just go with the easy way out. Look beyond traditional finance for alternative options to enhance your returns. |

|

Inflation |

Interest Rates Soar Ahead of Fed’s March Meeting |

Interest Rates Soar Ahead of Fed’s March Meeting Key Takeaways

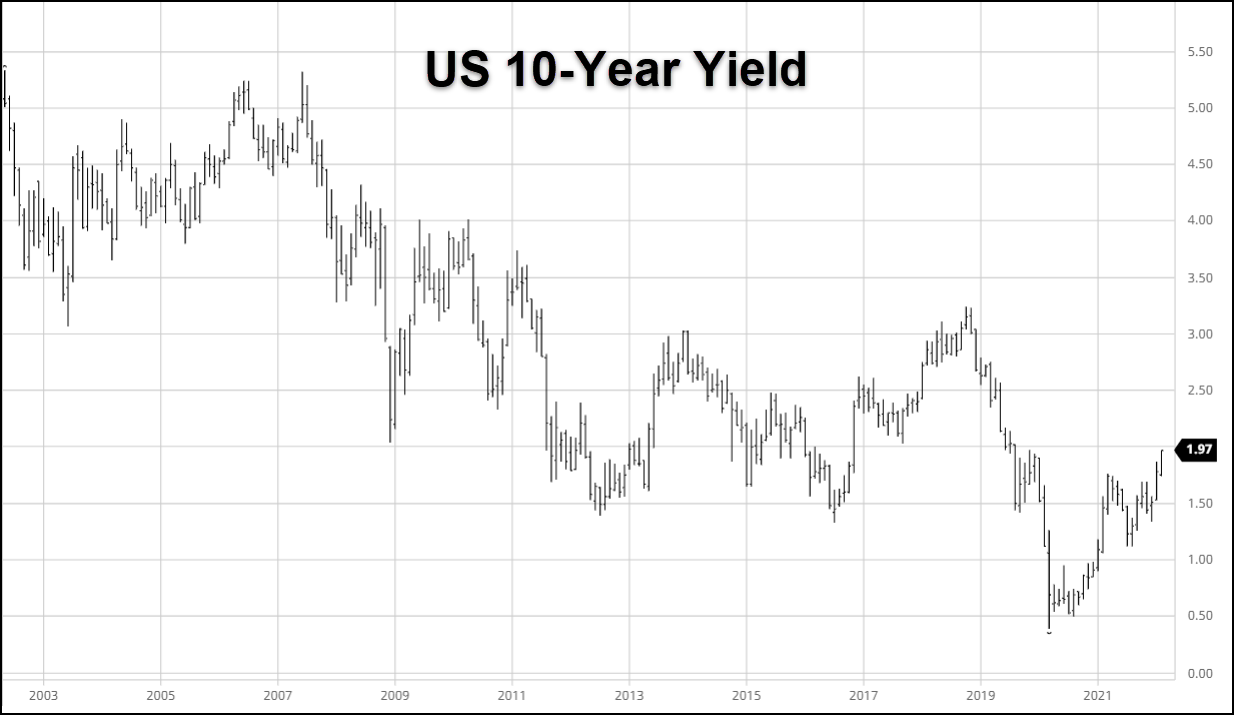

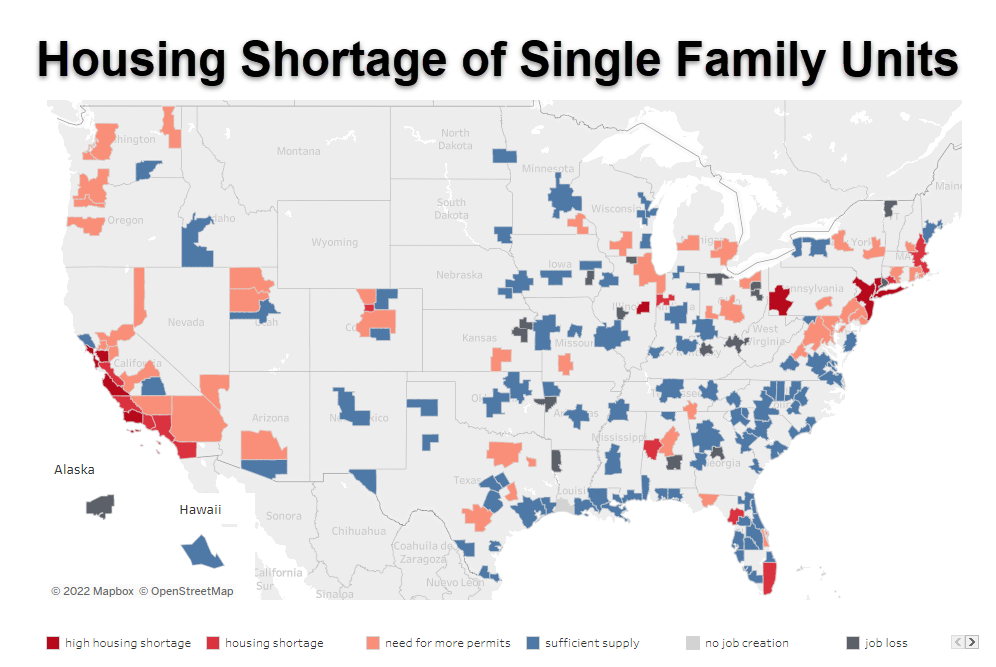

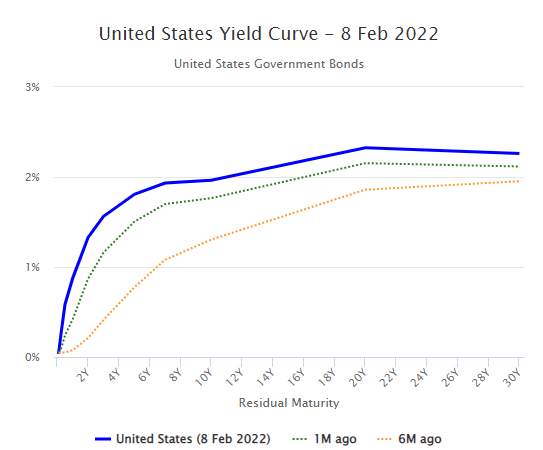

At 1.97%, the US 10-year yield hit i’s highest levels since the pandemic started. Is this something to worry about? Housing to Take a Hit Home mortgages are set based on the interest rate of the 10-year US Treasury plus a premium. As Treasury prices increase, so do the rates for home loans. Housing inventory is already in short supply, leading to YoY price increases in the double digits for home purchases and rent. Higher interest rates make this venture even more expensive and price some out of the market. We already face a severe shortage of starting home inventory for millennials and Gen Z. Source: National Association of Realtors Now, higher home loan rates mean higher monthly payments. Higher monthly payments mean those who can afford home loans will have less discretionary income, while others who qualified at lower interest rates no longer do. Interest Rate Big Picture Under normal conditions, US Treasury markets pay lower rates for short-duration debt and higher rates for long-duration debt. This creates the ‘yield curve’ which plots interest rates based on the duration or maturity of different US Treasuries. Typically, we see curves like the dotted orange line that plots rates from six months ago, where the curve is steep. Today’s rates are worrisome because the blue curve shows us that the difference between the 5-year and 30-year interest rates aren’t that big. In fact, it’s the lowest spread since early 2019. A flat curve like this implies the end of a high growth cycle that is leading to inflation and a subsequent slowdown. This makes sense since we expect the Fed to raise rates in the near future. The Bottom Line: Higher interest rates are needed to bring down inflation by cutting into demand. However, don’t let the headlines fool you. Prior to the pandemic, the 10-year yield was more than 3.0% in 2018. If we see interest rates crest that critical threshold, that’s when markets need to begin to worry. Until then, consider this a boon for banking stocks in the S&P Financials ETF XLF which includes stocks like Citigroup (C), Bank of America (BAC), and American Express (AXP) or the Regional Bank ETF KRE which includes Regions Financial (RF), Huntington Bank (HBAN), and Key Bank (KEY). But if you’re looking for a home, keep an eye for rising interest rates that could cost you more per month or price you out of the market entirely. |

|

News & Insights |

Freshly Squeezed |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |