|

Proprietary Data Insights Financial Pros Streaming & Entertainment Stock Searches in the Last Month

|

|||||||||||||||||||||

|

Consumer Discretionary |

Is the Worst Behind Netflix?

|

|

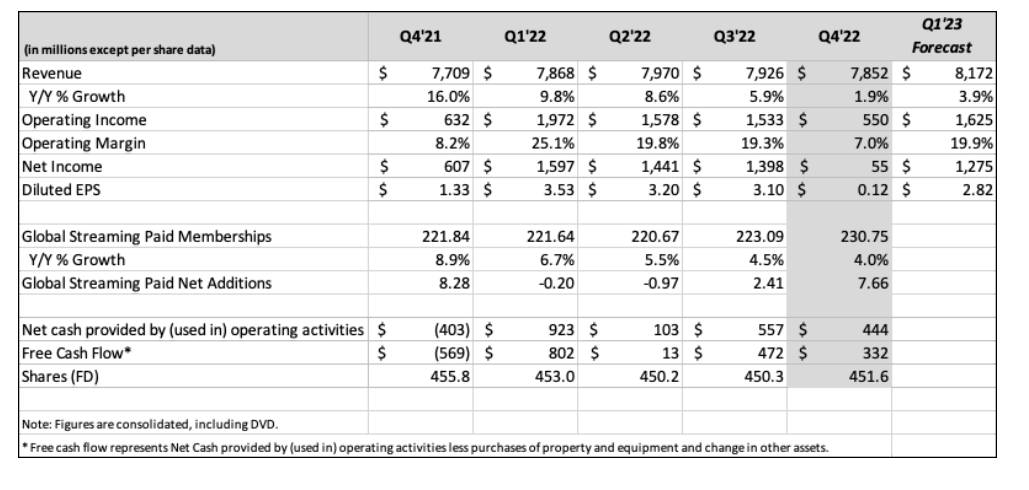

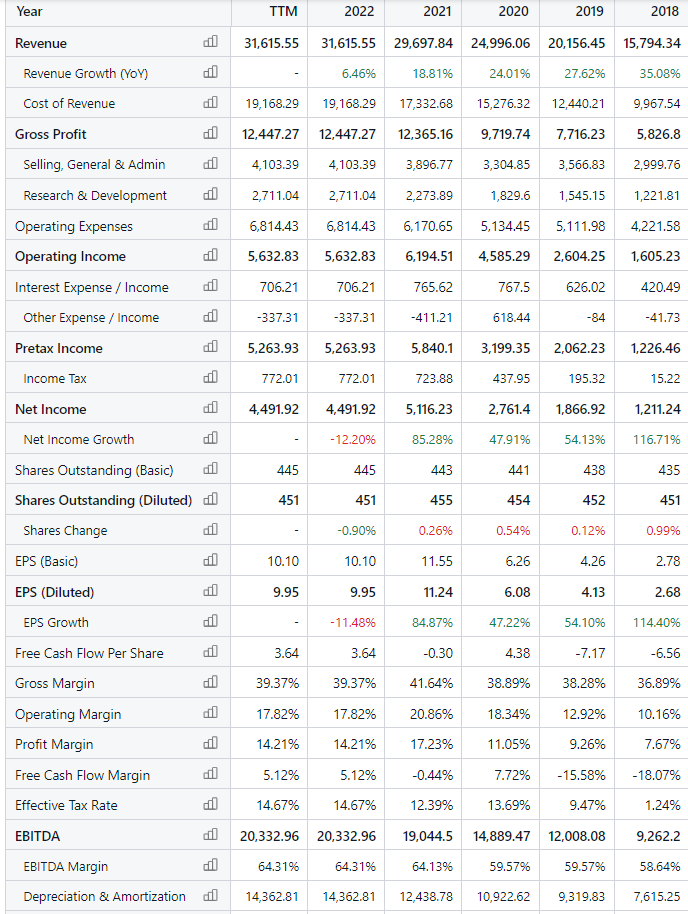

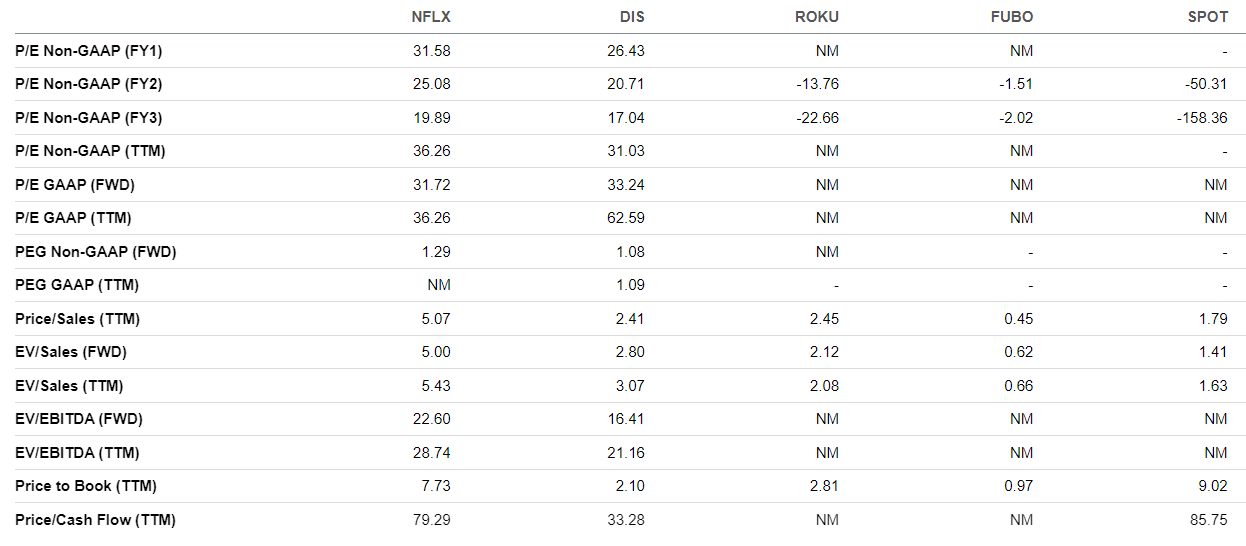

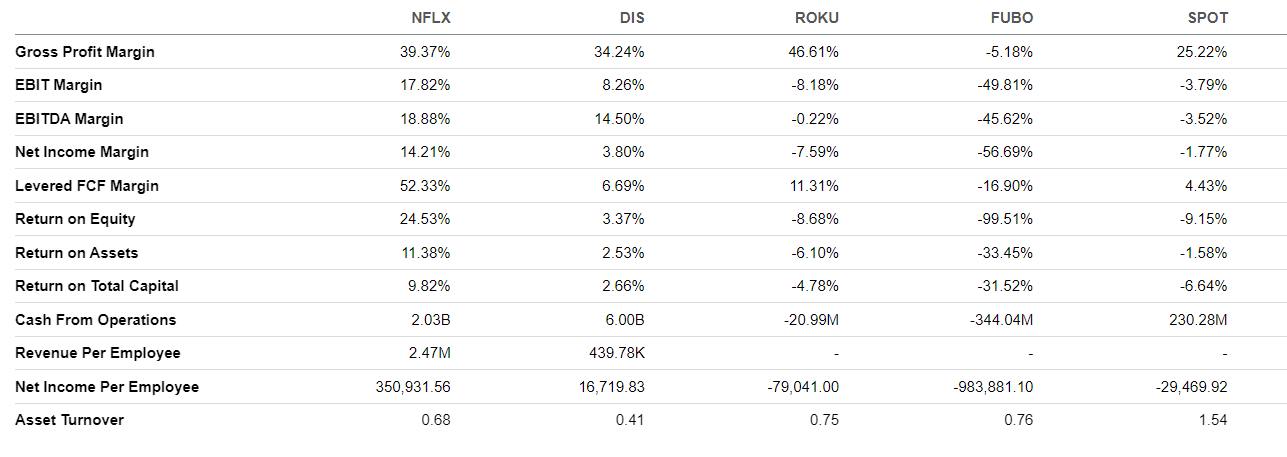

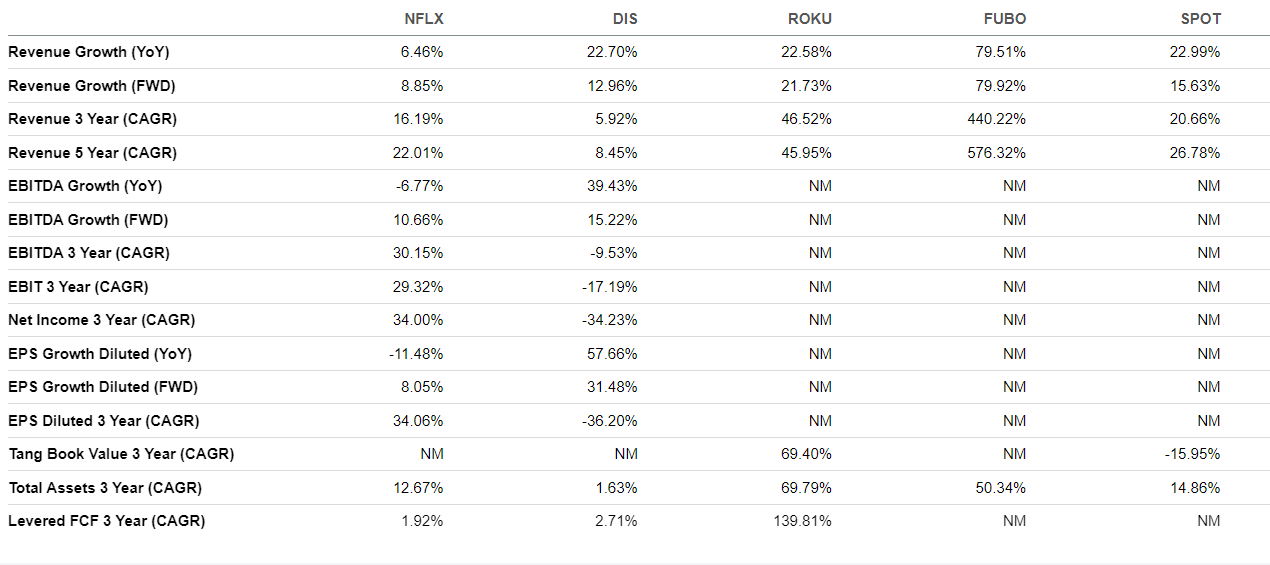

In 2001, Blockbuster Video offered $50 million to buy Netflix (NFLX). Netflix said no. Today, the content giant is the most popular streaming service, with nearly 231 million subscribers. It boasts a market cap that rivals Disney (DIS)’s. Since we wrote about Netflix in April, the stock has rallied more than 60%. After NFLX rocketed post-earnings, it shot up to the top spot among financial pros’ streaming and entertainment stock searches, according to the latest data from Trackstar, our proprietary sentiment indicator. In fact, it’s pulled in nearly twice the search volume as the House of Mouse. After the stock disappointed shareholders in 2022, financial pros are reevaluating it, as it appears the worst may be behind it now. The company’s latest quarterly results exceeded many of Wall Street’s expectations. Some believe Netflix can accelerate revenue growth. Netflix’s Business A decade ago, a Netflix subscription meant hundreds of B-rated movies that no one wanted to watch. Or you could rent DVDs through the mail. It wasn’t until the company began creating its own content, starting with House of Cards and Orange Is the New Black, that everything changed. Today, Netflix is an entertainment company that offers a video-streaming subscription service for its TV series, documentaries, and feature films, many of which are exclusive to the Netflix platform. Subscribers can gain access to Netflix via computer, TV set-top boxes, mobile, and other internet-connected devices. The company boasts 230.75 million paid subscribers, who generated $32 billion for it in 2022. Source: Netflix In Q4 2021, Netflix reported 221.84 million global paid streaming subscribers, coming off a gangbuster year courtesy of COVID-induced housebound customers. In Q1 2022, that number fell to 221.64 million. It was the first time in over a decade that Netflix’s subscriber growth dropped. That worried investors… a lot. Thankfully, Netflix bounced back in Q3 and Q4 2022, finishing the year at 230.75 million global paid streaming subscribers. When subscriber growth slowed, the company added a cheaper, ad-supported subscription plan. It’ll soon roll out a sharing plan to yank back some lost revenues from people who use the platform but don’t pay because they use someone else’s account. Netflix continues to lead the industry in streaming engagement, revenue, and profit, with its Q4 content slate outperforming even high expectations. During its Q4 2022 earnings release, it announced that longtime CEO and cofounder Reed Hastings would be stepping down from his role. Current co-CEO Ted Sarandos and COO Greg Peters will take over. Financials Source: Stock Analysis NFLX grew explosively from 2016 to 2021, going from $8.8 billion to $29.6 billion in revenue. Even as membership declined in early 2021, the company hit record revenues. Investors feared the worst after Q1 2022, sending shares into a death spiral. But management buckled down and boosted global paid streaming members from 221.8 million in Q4 2021 to 231 million in Q4 2022. In addition, Netflix recorded its highest revenues in company history in 2022, $31.6 billion. But net income declined 12.2% from 2021 to 2022. While profit margin declined from 2021 to 14.2% in 2022, it’s considerably higher than where it was in 2019 at 9.3% and in 2020 at 11.1%. The company is committed to igniting growth and believes it can do that through its new initiatives, including paid sharing and ad offerings. It’s in an excellent financial position to execute its plan, as it did $5.6 billion in operating income in 2022 and has $2.0 billion of net cash from operating activities. Valuation Source: Seeking Alpha NFLX trades at a P/E GAAP ratio of 36.3x, notably lower than its five-year average of 92.4x, as well as rival DIS at 62.6x. Other competitors in the streaming and entertainment space, like Roku (ROKU), fuboTV (FUBO), and Spotify (SPOT), aren’t even profitable and may not be anytime soon. Of course, NFLX faces competition from Apple (AAPL), Alphabet (GOOGL), and Amazon.com (AMZN), but they’re not pure streaming and entertainment companies, so we’re not including them in our comparisons. While a price-to-sales ratio of 5.1x may appear high for NFLX, it’s significantly lower than the stock’s five-year average of 8.2x. Nonetheless, its peers trade at much lower P/S ratios. DIS is at 2.4x, ROKU at 2.5x, FUBO at 0.5x, and SPOT at 1.8x. But there’s another way to look at this. A high P/S ratio shows investors are willing to pay a premium for NFLX because of its dominant position in the streaming market. As long as it continues to grow, maintain high profit margins, and lead its peers, it deserves to trade at a higher premium. Keep in mind, while Disney is big on streaming services, the company does so much more, from theme parks to movies, that it’s not an apples-to-apples comparison with Netflix. So consider that as we review these metrics. Profitability Source: Seeking Alpha Netflix’s subscription revenue model has helped increase its overall financial stability and profitability. It’s evident when you look at the company’s EBIT margin of 17.8%, which is double that of DIS at 8.3%. Meanwhile, ROKU is at -8.2%, FUBO at -49.8%, and SPOT at -3.8%. Furthermore, NFLX’s net income margin of 14.2% is nearly 4x greater than DIS at 3.8%. And it’s head and shoulders above ROKU at -7.6%, FUBO at -56.7%, and SPOT at -1.8%. Netflix generates a hefty cash flow, which provides a cushion for unexpected expenses and allows for future investments. The company pulls $2.0 billion in cash from its operations. DIS does even better at $6.0 billion. On the other hand, ROKU is at -$20.9 million, FUBO at -$344.0 million, and SPOT at $230.3 million. Growth Source: Seeking Alpha Make no mistake, 2022 was hard for NFLX. The company grew revenues only 6.5%. Meanwhile, its peers had double-digit growth numbers. FUBO led at 79.5%, followed by SPOT at 22.9%, DIS at 22.7%, and ROKU at 22.6%. NFLX’s EBITDA growth of -6.8% in 2022 is a disappointment, to say the least. But as we mentioned, the company has a plan to boost revenues. Our Opinion 6/10 When we wrote about Netflix in April of last year, it traded at around $215 per share. We said that shares were depressed, but that the company had several levers it could pull before Wall Street wrote it off. Shares have since risen by more than 60% to over $353. Competition still remains stiff. And the company forecasts revenue growth to be modest in Q1 2023, which could lead to a better entry price. We’d buy around $280 to $300. |

|

News & Insights |

Just Spilled

|

|

Want to get content like this directly to your inbox? |