|

Proprietary Data Insights Financial Pros’ Top Gold Miner Stock Searches in the Last Month

|

|||||||||||||||||||||

A Cheap, Stable Gold Miner |

|

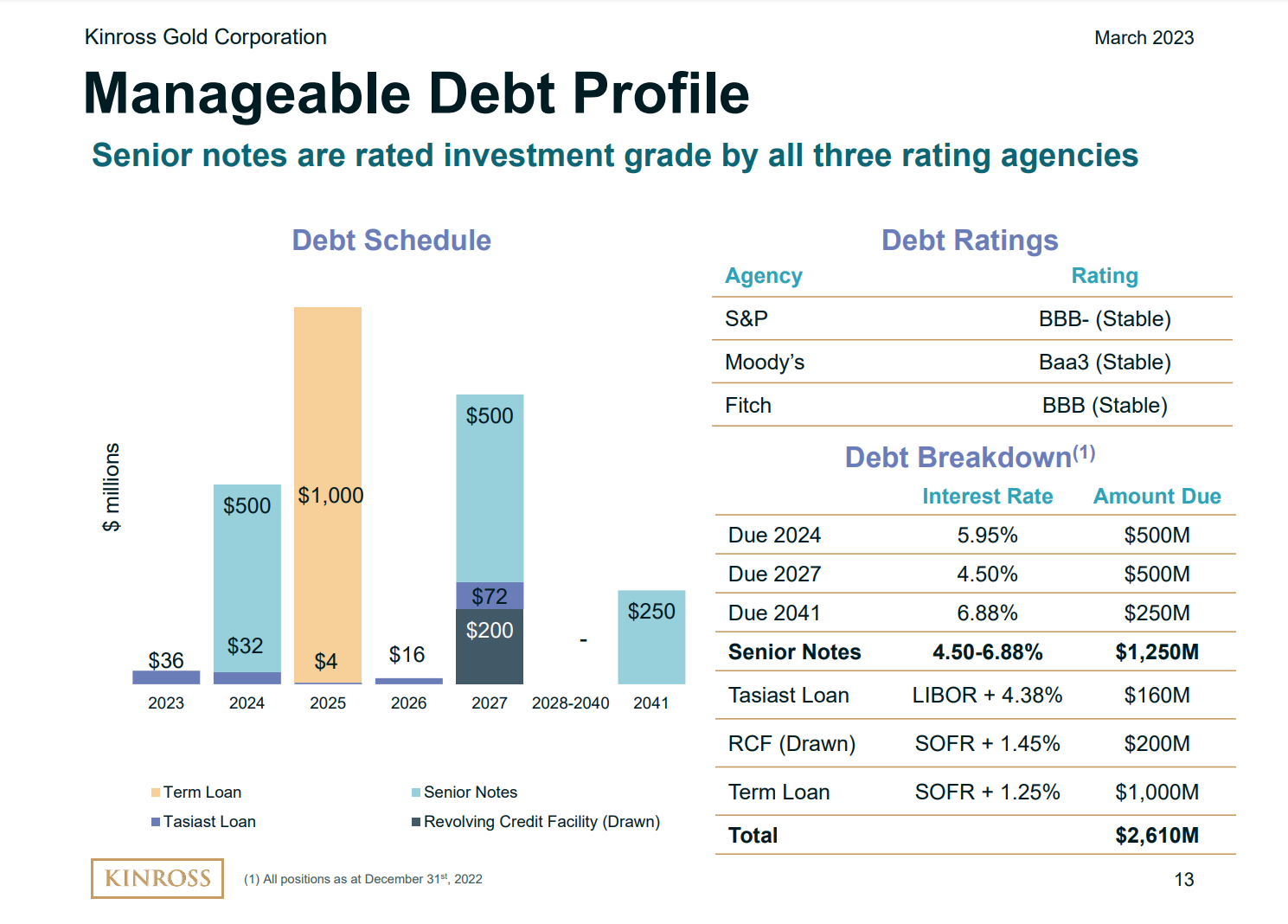

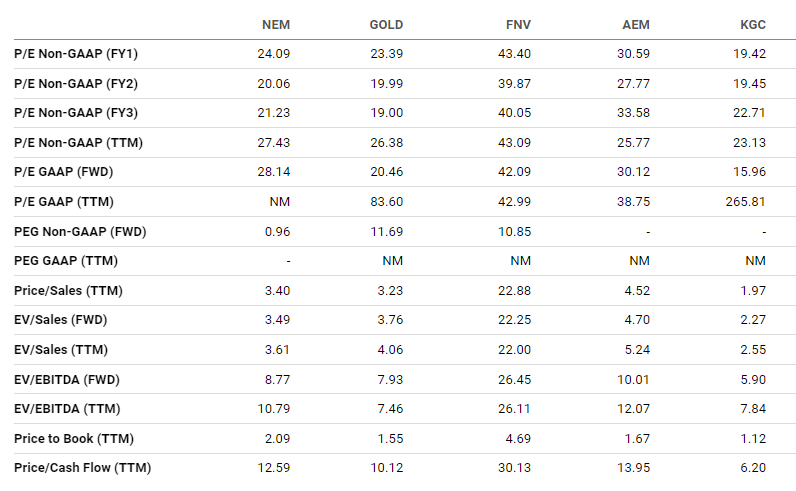

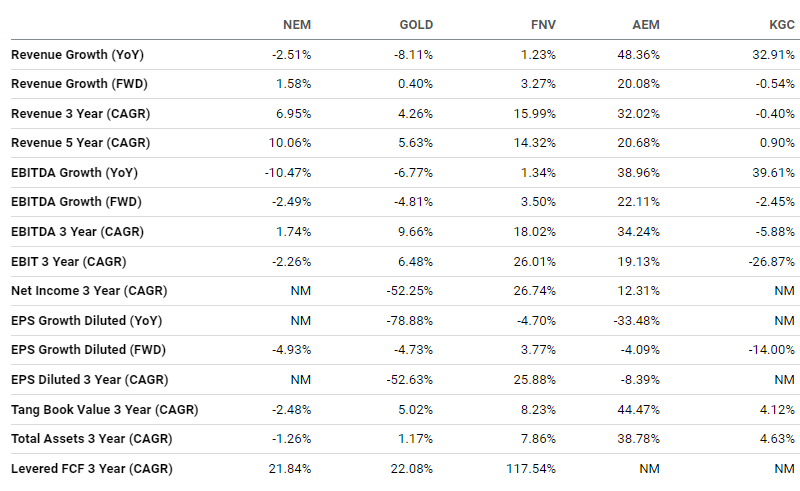

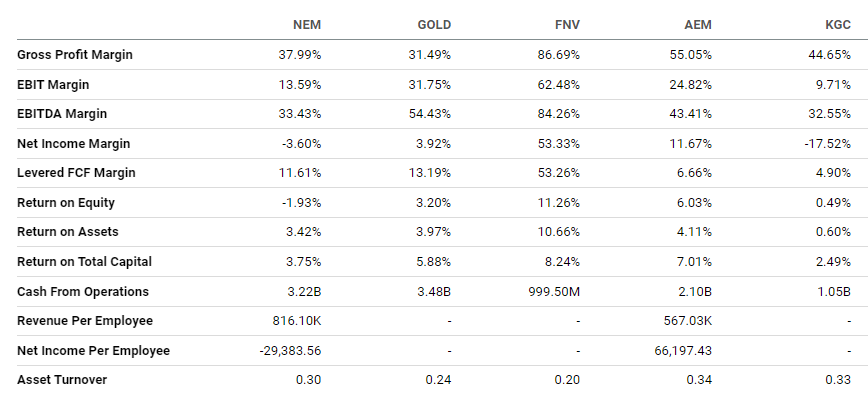

Break out grandma’s jewelry… Gold is one of the top-performing assets this year, with spot prices now comfortably over $2,000 an ounce. Gold miners haven’t fared as well. Higher financing, energy, and labor costs offset many of their gains. When we looked into gold miner stock searches in our proprietary Trackstar database, it wasn’t financial pros’ top search that stood out, but #5. We’d never heard of Kinross Gold (KGC) before today’s write-up. But as we looked under the hood, we realized these financial pros might be onto something… Kinross Gold’s Business Kinross is a Toronto-based senior gold miner founded in 1993. It has a diverse portfolio of mines and projects in the U.S., Canada, Brazil, Chile, and Mauritania. It’s focused on delivering value through stable production, ESG responsibility, and shareholder returns via a steady dividend and share buyback program. Source: Kinross Gold In addition to $510 million in maintenance capital expenditures, management plans to spend another $490 million in 2023 to expand, leveraging existing infrastructure and experience in operating jurisdictions to minimize execution risk. Financials Source: Stock Analysis Kinross’ revenues largely depend on gold prices. Hence why sales improved in the last few years. Both top-line prices and energy costs drive profitability. Unsurprisingly, KGC’s best year was 2020, when gold prices skyrocketed and oil plunged. The company prides itself on an excellent balance sheet with plenty of liquidity and extremely well-managed debt. Valuation Source: Seeking Alpha Part of why we like KGC is its solid valuation. Compared to other players such as Newmont (NEM) and Barrick Gold (GOLD), KGC is cheaper in price-to-earnings, price-to-sales, and price-to-cash-flow ratios. In fact, KGC’s closest competitor in cash-flow ratio is nearly twice as expensive. Growth Source: Seeking Alpha KGC’s valuation is surprising given its fantastic growth last year. Although its forward growth isn’t stellar, none of its peers expect much either, save for Agnico Eagle Mines (AEM). Profitability Source: Seeking Alpha KGC falls apart on profitability. Expenses have been steady. It comes down to realized gross profit margins, which were near or above 50% in 2020 and 2021. Last year, they were about 38%. But given KGC’s steady cash flow of $1 billion per year, we aren’t too concerned with the profit variance. Our Opinion 8/10 Kinross delivers surprisingly steady results. We expect its investments in project expansion will help improve margins soon. We feel KGC is the gold miner best suited to take advantage of higher gold prices in the near term. |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |