|

Proprietary Data Insights Financial Pros’ Top Large Bank Stock Searches in the Last Month

|

||||||||||||||||||||||||||||

The $100 Billion Question: Can Citigroup Get Its Mojo Back?

|

|

Of the big Wall Street banks, Citigroup bills itself as a global player, connecting customers around the world. However, CEO Jane Fraser wants a leaner company focused on its core markets. To that end, Citigroup:

Source: Citigroup Q4 2023 Earnings Presentation Citigroup’s current business is divided into:

Source: Citigroup Q4 2023 Earnings Presentation Financials

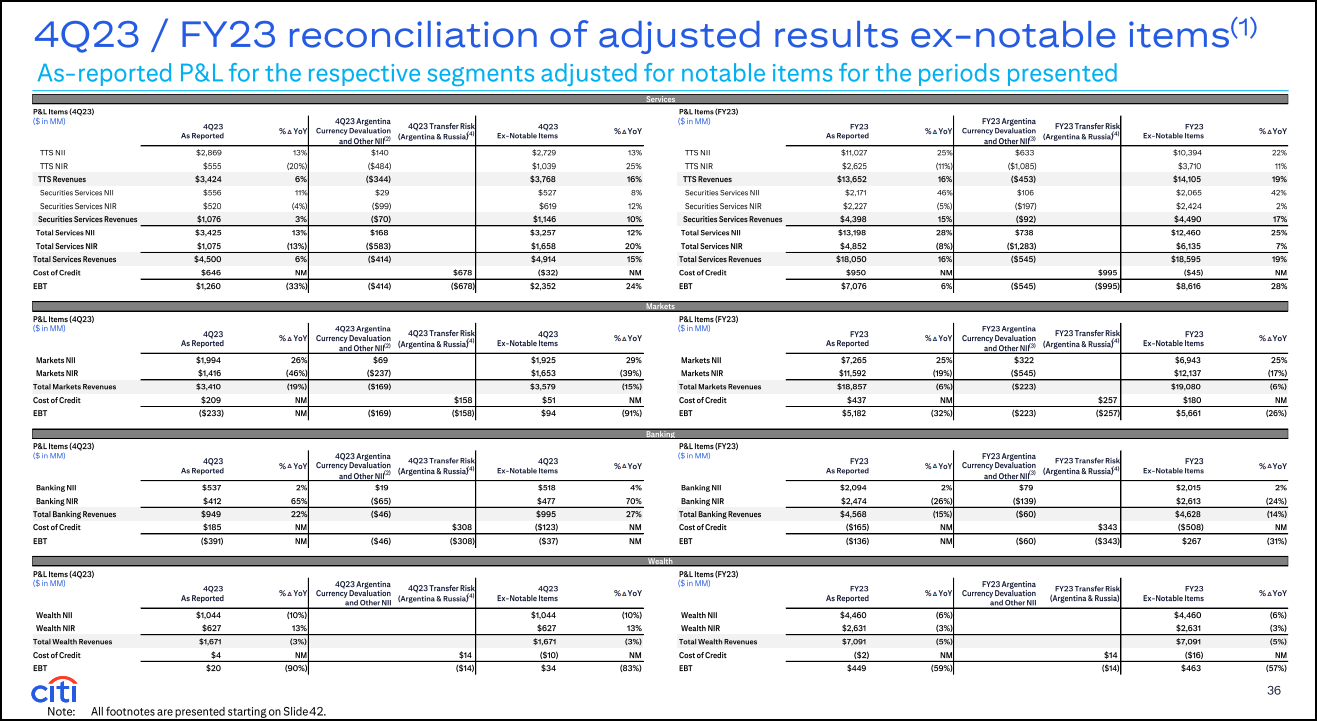

Source: Stock Analysis Citigroup benefited tremendously from higher interest rates, with net interest income (the difference between the rates they pay depositors and the rate they lend) up 4% YoY in Q4 and 13% for all of 2023. However, non-interest revenue tanked 43% YoY in Q4 and was down 12% in 2023 compared to 2022, about a third related to divestitures. Excluding one-time items, revenues slipped by 3% while operating income declined by 20% compared to Q4 2022, as corporate lending dropped 26% and lower year-end volatility negatively impacted fixed-income trading. The good news is roughly $4.7 billion this quarter was tied to one-time items, from restructuring charges to a special FDIC assessment. And all the restructuring charges are expected to deliver $2.5 billion in annual cost savings by 2025. Plus, CFO Mark Mason outlined projections for 4%-5% compounded annual growth through 2026. Valuation

Source: Seeking Alpha With many changes in the works, it’s not surprising to see Citigroup trade at a discount to its peers. Interestingly, JP Morgan trades at a lower trailing P/E ratio but a slightly higher forward P/E ratio. With banks, we also like to look at the price-to-book ratio to see how investors value the loan portfolio. Here, Citigroup looks dirt cheap. However, the market is likely discounting expectations for Citigroup to achieve its transformation by 2025-2026. For comparison, it took Wells Fargo (WFC) nearly five years to complete its turnaround and had a far less complicated business model. Growth

Source: Seeking Alpha Unsurprisingly, Citigroup’s revenue growth is negligible. We don’t know yet whether they’ll achieve the 4%-5% average growth in 2024, coupled with more cost savings. Comparatively, all the other banks have seen net income growth well into the double-digit range, save for US Bancorp (USB). Profitability

Source: Seeking Alpha Right now, Citigroup’s profitability falls well short of its peers. Its future relies heavily on its ability to deliver on its planned turnaround. Our Opinion 9/10 We believe Citigroup’s transformation plans will succeed, though they will likely take longer than is being forecast. Nonetheless, we don’t believe the 4% dividend is in danger of a cut anytime soon, providing investors with a nice cushion while you wait. However, be prepared for pullbacks as possible rate cuts would eat into net interest income and overall profitability in the near future. |

|

News & Insights |

Just Spilled

|

|

Want to get content like this directly to your inbox? |