|

Proprietary Data Insights Financial Pros’ Top Chinese Stock Searches in the Last Month

|

||||||||||||||||||||||||||||

Pros Top 5 Chinese Stock Searches in August

|

|

|

Pinduoduo (PDD) is shaking up e-commerce with its “team purchase” model and direct-to-consumer approach. With its launch of Temu in 2022, the company targeted American consumers with cheap products during a time of raging inflation. Sales exploded as the app became the #1 downloaded platform. Yet, only 10% of customers said they would return after their first purchase compared to 90% with Amazon. The company’s latest earnings report caught the attention of financial pros, making it their top Chinese stock search in August. By all appearances, the company is immensely profitable. Yet, investors are still cautious about any Chinese company. But at 6.8x forward cash, and forward growth expectations of 56.7%, is this too good of a deal to pass up? Pinduoduo’s Business PDD thrives on volume. The company cuts out middlemen by connecting consumers directly with manufacturers. Essentially, manufacturers list everything they could make and their prices for consumers to purchase. Once the customer buys the items, the manufacturer produces and ships them, not before. This creates long lead times but keeps prices down. Most products are low quality, with defects that can’t be remedied. So, it’s a bit of a crapshoot in terms of what you get. Its signature “team purchase” feature encourages users to recruit friends for group buys, unlocking deeper discounts. This viral, gamified approach has propelled PDD to over 900 million annual active buyers in China alone. PDD Holdings segments its business into two main revenue streams:

PDD’s latest quarter showcased its knack for hypergrowth, with revenue rocketing 86% to $13.36 billion. Yet, management raised eyebrows by warning of fiercer competition and potential profit squeezes ahead. This dour outlook, despite stellar results, sent investors into a tizzy. While PDD has a track record of sandbagging guidance, the stark warnings about eroding profitability hit a nerve. The company now faces the challenge of maintaining its meteoric rise in China’s cutthroat e-commerce arena while expanding its international footprint through Temu. Financials

Source: Stock Analysis PDD isn’t one to lack growth. Sales grew between 50%-100% in the last five years, save for 2022. However, gross margins dropped from 75.9% to 62.4% in recent years, while operating and profit margins improved from single digits to nearly 30%. Free cash flow margin improved to 39.1% as the company built up $39.2 billion in cash with negligible debt. Yet, like many other Chinese companies, PDD hasn’t returned cash to shareholders through dividends or buybacks. So, for now, all wealth creation is on paper. Valuation

Source: Seeking Alpha By standard valuation metrics, PDD is cheap. It trades at just 7.2x trailing operating cash flow, 10.4x trailing earnings, and 2.8x sales. That’s cheaper than every other stock on this list, including Alibaba (BABA). Growth

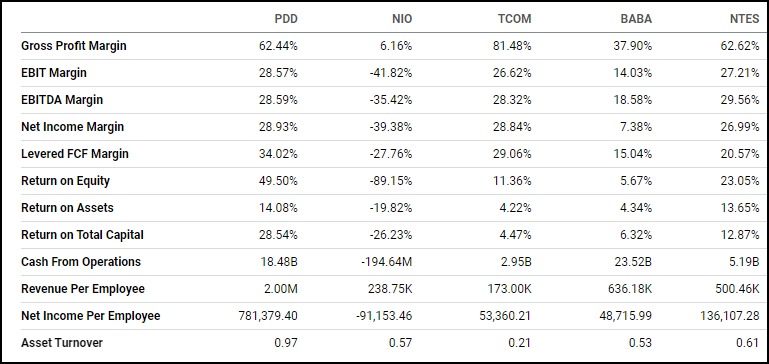

Source: Seeking Alpha Despite its discounted price, PDD has growth rates far above its peers. Its three and five-year average sales growth exceeds 58% and 74%, respectively, while its average free cash flow growth over the last three years exceeds 130%. Few, if any, American companies can boast these kinds of numbers. Profitability Source: Seeking Alpha Even with its high growth, PDD delivers fantastic margins, with an EBIT of over 28% and a free cash flow margin of 34%. The only reason its return on assets is at 14% is because it keeps stashing cash on its balance sheet.

Our Opinion 8/10 We aren’t fans of Chinese companies. The governmental risk with them is extremely high. Yet, PDD is so cheap it’s worth taking a shot. Don’t expect to get paid through dividends anytime soon. But we could see share buybacks in the near future. This is a high-risk investment, but we think it is worth taking a shot at. |

|

News & Insights |

Just Spilled

|

|

Want to get content like this directly to your inbox? |