It’s not easy being a mainstream economist. You spend your life building models that become your professional identity. And when those models fail to describe and predict reality, you’re left wondering about the meaning of it all.

The latest case in point is US housing. Keynesian economic models say that if you lower mortgage rates you get more houses bought, sold and built. A nice, simple piece of cause and effect. But today’s mortgage rates are at levels that would have incited a buying frenzy a generation ago and employment is rising. Yet home sales, home building and mortgage originations are all flat-lining.

Zero Hedge and Automatic Earth posted good discussions of the current state of the housing market recently. See:

Economists Stunned By Housing Fade

US Housing is Down For the Count

Both articles make a compelling case that housing is weak and getting weaker. The broader question is what it means for the rest of the economy. Is housing a discrete sector going through its own stuff, or is it connected to traveling a path that the rest of the economy will soon follow?

The case for the latter scenario is based on the idea that newly-created currency pouring into the financial system pumps up asset prices, which convinces people that they’re rich enough to indulge in new cars, new clothes and nice vacations — and more stocks and houses.

But this “wealth effect” only works when the amount of debt in the system is low enough for new debt to have the desired effect. If there’s already too much debt, then people don’t feel comfortable borrowing even at historically low interest rates and asset prices turn out be hard to levitate. Either they stall or start moving lower, which shifts the wealth effect into reverse and sucks the air out of the economy.

The reason why most economic models didn’t see housing rolling over and don’t think it will affect the rest of the system in any event is that most Keynesian models don’t pay attention to society’s balance sheet. A certain amount of new debt is supposed to increase “aggregate demand” by the same amount whether the government and consumers are debt-free or buried under a mountain of obligations as they are today. The fact that debt levels, especially student loans, are hitting records probably explains why the housing isn’t behaving according to script.

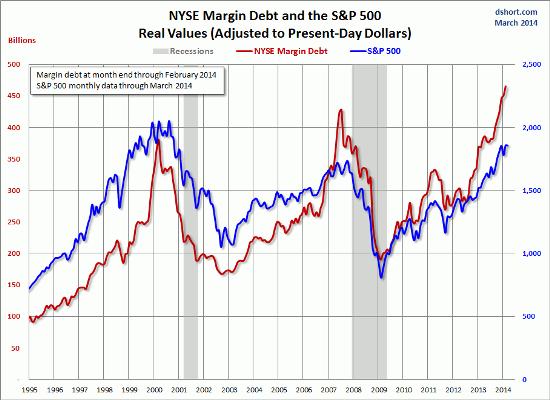

The other fuel for a wealth effect-driven boom is the stock market. Here again, a nice pop has coincided with a big jump in margin debt, which investors take on when they borrow against stocks to buy more stocks. Late last year margin debt hit a new record and since then it has just kept going. Now it’s at levels that, based on history, imply less bang for each new borrowed dollar. Going forward it will be harder for investors to generate big returns by borrowing money and buying more. And therefore harder to justify more buying.

Click here for a great explanation of why pretty much every stock market valuation measure is now flashing either yellow or red, from John Hussman.

Assuming that the stock market joins housing and either stalls or corrects, what does that do to the strategy of using asset bubbles to pump up the consumer economy? Probably it derails it. The question is when.

Hussman notes that periods of extreme overvaluation like today are highly predictable indicators of average returns over the next decade, but not so great as a trading signal. Stocks might get more overvalued before they’re through. But that would raise the risk of a crash, which would have an even more serious impact on investor psyches. So either way, this year or next, the wealth effect is about to turn into the poverty effect, and the asset-owing classes are about to get very nervous.