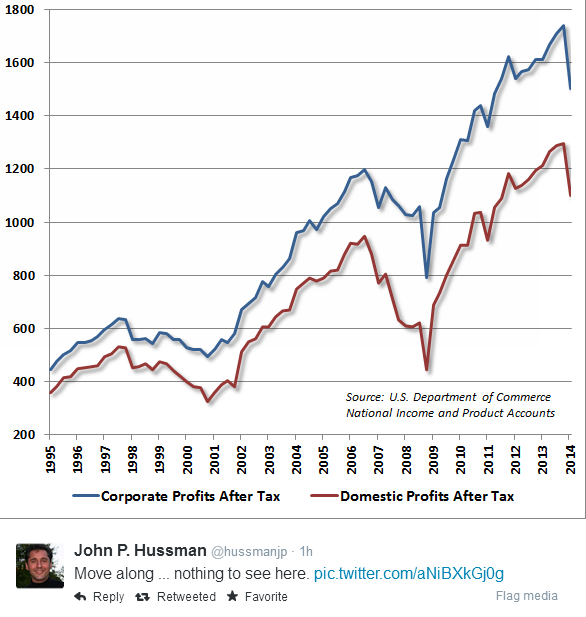

Did you notice the collapse in corporate profits?

John Hussman, Steen Jakobsen, and Albert Edwards at Society General did. Hussman tweeted the following chart this morning.

Steen Jakobsen, chief economist at Saxo bank passed on the above tweet this morning along with an attachment from Albert Edwards and this comment: “John – who I met at the Wine Country Conference – is not only great economist and fund manager, but also a remarkable Gentleman who lives to support Autism. This is his link Hussman Funds.”

From Society General – No Link Available

Smoke and Mirrors Stop Us Seeing a Slump in US Profits

During the excitement of the downward revision of Q1 US GDP from +0.1% to -1.0% investors seem not to have noticed a $213bn, 10% annualised slump in the US Bureau of Economic Analysis’s (BEA) favoured measure of whole economy profits, defined as profits from current production. Also known as economic profits, the BEA makes adjustments to remove inventory profits (IVA) and to put depreciation on an economic instead of a tax basis (CCAdj). We show below the stark difference between the BEA’s calculation for post-tax headline profits (up 5.3% yoy) and economic profits (down 6.8% yoy). In this note we try to explain what is happening and why the 10% annual slump in economic profits really does matter.

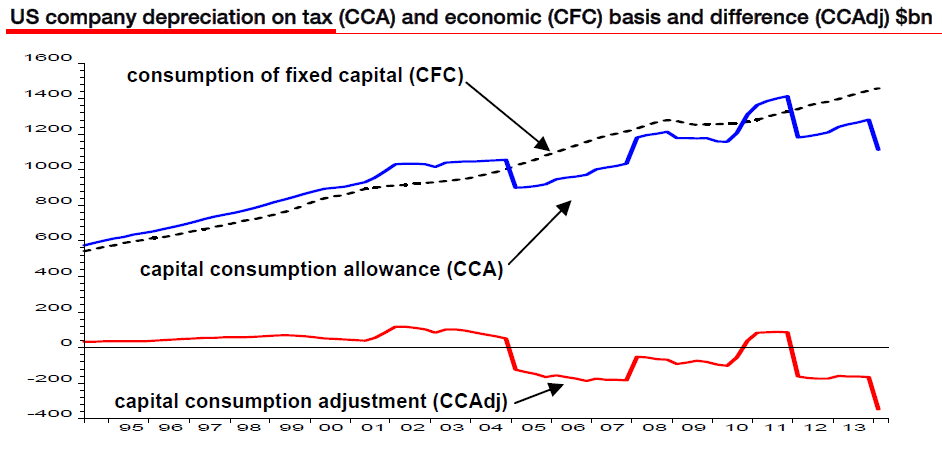

Having spent the best part of 25 years following US whole economy profits I feel I have a good understanding on what exactly is going on. I was however most surprised at the divergence in the two key series shown on the front page chart. After a very long chat with a very helpful person from the BEA, she emailed me to “note this quarter, there is a substantial difference between profits from current production (that include IVA and CCAdj) and profits before tax (that exclude IVA and CCAdj) due to the expiration of investment incentives that allowed companies to accelerate depreciation over the past several years. As provisions of the tax acts from 2002, 2003, 2008, 2009, 2010, and 2012 expire, and as no new provisions are introduced, businesses are now expensing less depreciation for tax purposes. As a result, tax based depreciation expense, measured as CCA, is falling, while economic depreciation expense, measured as CFC, continues on a steady growth trend (see charts below). The difference between these two measures is the CCAdj. With economic depreciation expense higher than tax based depreciation expense, BEA’s measure of corporate profits with CCAdj shows a decline, while profits excluding CCAdj show an increase.”

So headline reported profits are currently artificially inflated upwards to show a roughly 5% yoy increase, which is incidentally the same pace that the MSCI trailing reported stockmarket profits are rising by – both are misleading investors as to the underlying strength of profits.

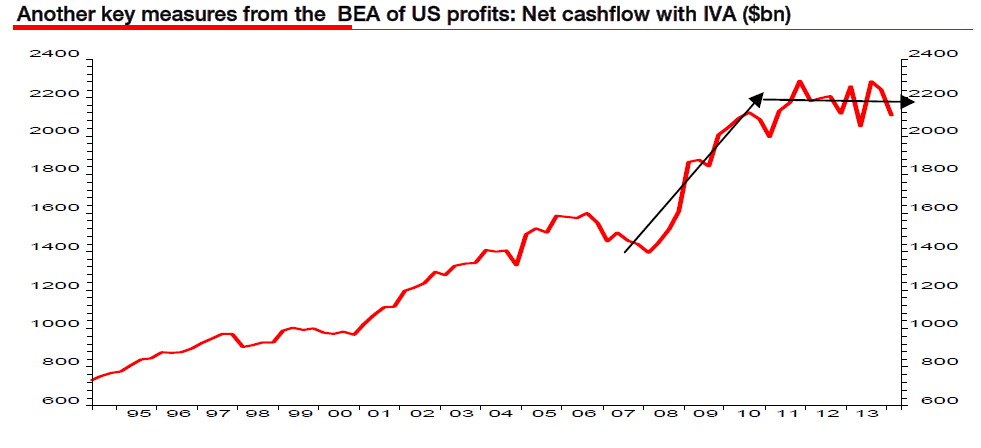

Net cashflow with IVA ($bn)

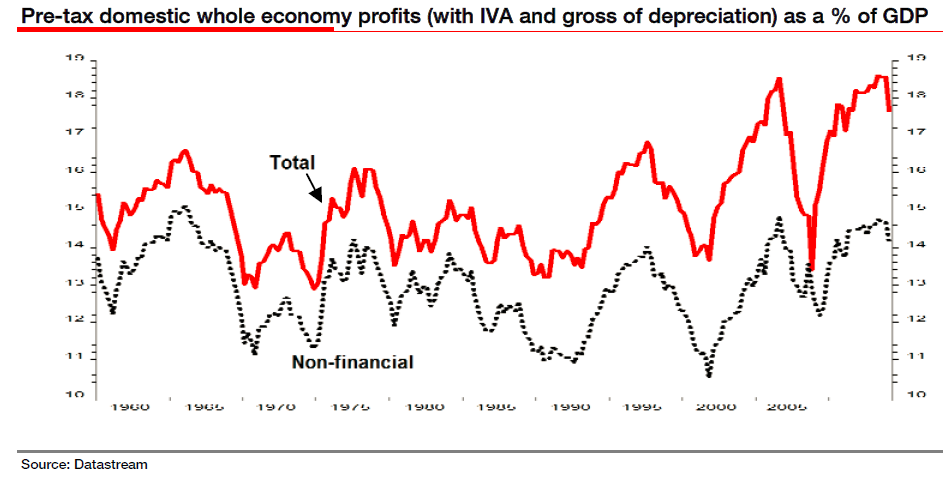

The BEA press release itself describes net cashflow with IVA as “the internal funds available to corporations for investment (calculated as after tax profits with IVA and CCAdj, net of dividend payments but plus depreciation on an economic basis (CFC))”. We can see from the chart above that this decreased by $132bn in Q1 following a decrease of $43bn in Q4. This key measure of internal funds available for investment has stalled badly over the last two years (see chart above). No wonder US business investment has been struggling recently. The bottom line is that the US profits margin cycle has begun to turn down at long last (see chart below). It is doing so from elevated but not unprecedented levels – especially the nonfinancial part of the economy (my former colleague Leo Doyle always told me I had to add depreciation into the profits numerator as the denominator GDP was also measured gross of depreciation – i.e. the G in GDP!)

Thanks to Albert Edwards via Steen Jakobsen for the above charts.

There is more in the report, including a discussion of why a renminbi (yuan) devaluation will crush US and European corporate profits.

If I can get an online link I will post it.

Wine Country Conference Videos

Here is a link to the 2014 Wine Country Conference Videos. Steen Jakobsen’s, Chris Martenson’s, and my presentation will be out later this week.

Inquiring minds should also take a look at Hussman’s post today, Market Peaks are a Process. John speaks of the Wine Country Conference Presentations and the cause.

Here is John’s blurb on the cause.

Last month, the second annual Wine Country Conference was held in Sonoma California, this year to benefit the Autism Society of America. As many of you know, my 20-year old son JP has autism, so the cause is close to my heart. The conference website has both PowerPoint slides and videos of the presentations and Q&A sessions (and more will be added over the coming weeks). The title of my presentation was “Very Mean Reversion”

My hope is that if you appreciate the conference materials, you’ll consider making a donation – in any amount at all – to the Autism Society of America. The proceeds of the conference will go to support programs and chapters at the local level throughout the United States (we’ve also put up a $50,000 matching grant to encourage donations). I appreciate your generosity.

Thanks – John

Please Consider Making a Donation

More presentations are yet to come! And if you enjoyed the presentations (or even if you didn’t), please Make a Donation to the Autism Society.

On behalf of John and the Autism Society, thanks to all who make donations. Any amount helps.

Mike “Mish” Shedlock

http://globaleconomicanalysis.blogspot.com