The Urban Institute has an interesting 14-page synopsis on Delinquent Debt in America.

By percentage, the number of people in collections is largely concentrated in the South, while amount owed shows no geographic pattern. The Urban Institute uses 2013 credit bureau data from TransUnion to measure how many Americans are reported as at least 30 days late, not including late payment of mortgages. The institute also examines how many Americans have debt in collections and the amount of this debt.

In order to have credit card debt, one first must have credit. However, some without traditional credit show up as delinquent on account of late utility, medical, or other bills.

Study Findings

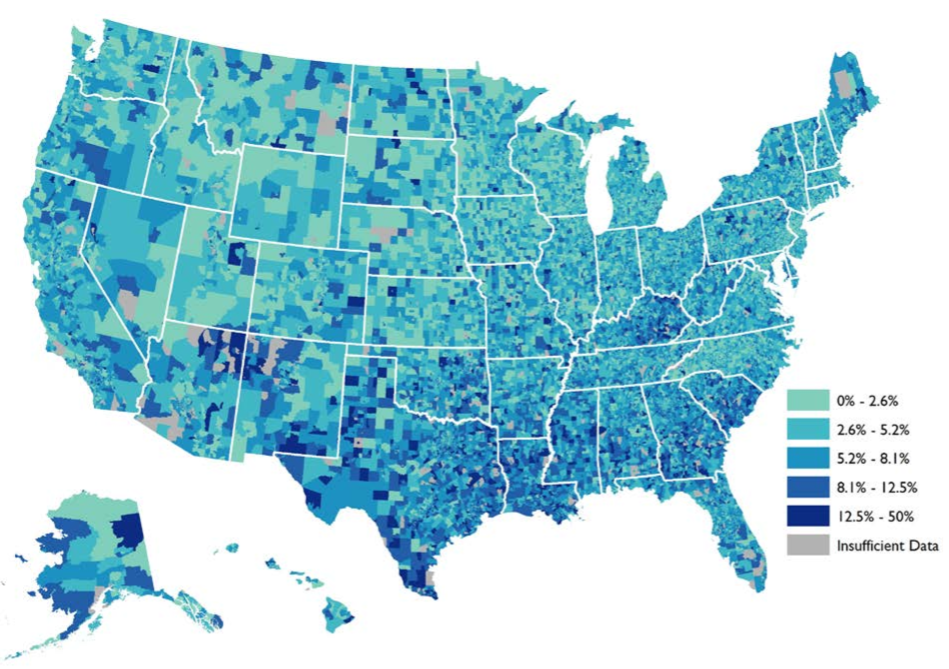

- 5.3% (Roughly 1 out of 20) of people with a credit file are at least 30 days late on a credit card or other non-mortgage account (e.g., automobile loan, student loan). In other words, they have debt that has been reported as past due to the credit bureau.

- The share of people with debt past due ranges from 4.6% in the West, North Central, and Middle Atlantic divisions to 7.5% in the West South Central division.

- Three states have less than 4% of the population with debt past due: Utah, Washington, and New Jersey.

- Three states have more than 7% of the population with debt past due: Louisiana, Texas, and Mississippi.

- Nearly 40% of the high-concentration census tracts in the country are in Louisiana or Texas.

- Areas with lower household incomes have more people with debt past due, but the correlation is only -0.3. So, while income matters, the concentration of delinquent debt is not simply an income story.

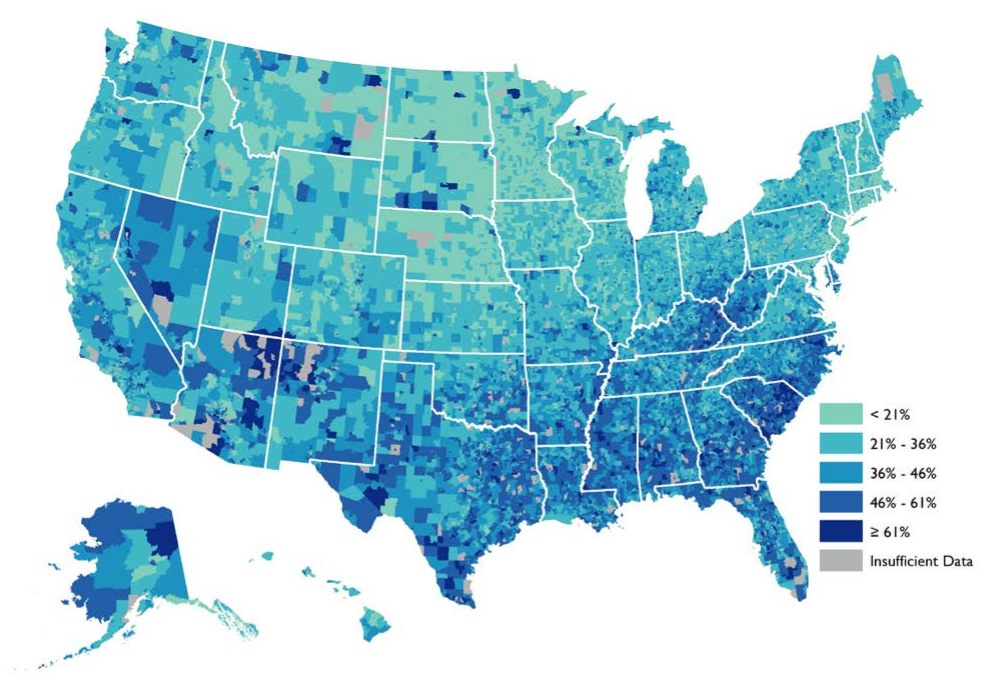

- Of those with credit files, an alarming 35% have debt in collections.

- Debt in collection ranges less than $25 to more than $125,000. The average amount owed in collections is $5,178.

- Nevada, which was hard hit by the housing crisis, tops the list of past-due states: 47% of people with a credit file in Nevada have reported debt in collections. The District of Columbia and an additional 12 states (11 in the South) are over the 40 percent mark: Alabama, Arkansas, Florida, Georgia, Kentucky, Louisiana, Mississippi, New Mexico, North Carolina, South Carolina, Texas, and West Virginia.

- At the low end are three Midwestern states – Minnesota, North Dakota, and South Dakota, with 20% of the people with a credit history now reported debt in collections.

- Among the largest 100 MSAs, only six have fewer than a quarter of people with debt in collections reported i n their credit file. None are in the South: Minneapolis – St. Paul, Minnesota (20.1%), Honolulu, Hawaii (21.0%), Boston, Massachusetts (22.4%), Madison, Wisconsin (22.6%), San Jose, California (23.0%), and Bridgeport, Connecticut (24.5%).

- At the other extreme, five MSAs have at least 45 percent of people with collections debt reported in their credit files : McAllen, Texas (51.7%), Las Vegas, Nevada (49.2%), Lakeland, Florida (47.3%), Columbia, South Carolina (45.2%), and Jacksonville, Florida (45.0%).

- An astonishing 70% of census tracts have at least 25% of people with reported debt in collections. In comparison, less than 1% of census tracts (40) have at least 25% of people with debt past.

Debt Past Due

Debt in Collections

Average Debt in Collections

click on any chart for sharper image

The report concludes …

Financial distress is a daily challenge for millions of American consumers. Nearly 1 2 million adults — 5.3 percent of Americans with a credit file — have non-mortgage debt reported past due, and they need to pay $2,258 on average to become current on that debt.

Further, an alarming 77 million Americans — 35 percent of adults with credit files — have debt in collections reported in their credit files, with an average debt amount of nearly $5,178. Debt reported past due, and in particular reported debt in collections, is more concentrated in the South.

In addition to creating difficulties today, delinquent debt can lower credit scores and result in serious future consequences. Credit scores are used to determine eligibility for jobs, access to rental housing and mortgages, insurance premiums, and access to (and the price of) credit in general (Federal Trade Commission 2013; Traub 2013).

High levels of delinquent debt and its associated consequences, such as limited access to traditional credit, can harm both families and the communities in which they live. This brief contributes to our understanding of financial distress in America by exploring the spatial patterns of delinquent debt in the United States. Future work will explore the drivers of financial distress and those factors influencing its spatial patterns.

Interestingly, the concentration of delinquent debt to income has a negative 0.3 correlation. In a footnote the study reports “The correlation between average household income and average amount of debt past due (amount required to become current on that debt) is even lower at -0.1.”

Mike “Mish” Shedlock

http://globaleconomicanalysis.blogspot.com