Is it time to short the dollar?

Saxo bank chief economist Steen Jakobsen thinks so. Via email from Steen …

What is wrong with changing your mind because the facts changed? But you have to be able to say why you changed your mind and how the facts changed. Lee Iacocca

My biggest call all year has been for global lower rates, and in particular lower core country (Germany, Denmark, and US) yields led by this magic trinity of factors:

1. China and Asia rebalancing growth away from nominal to quality growth

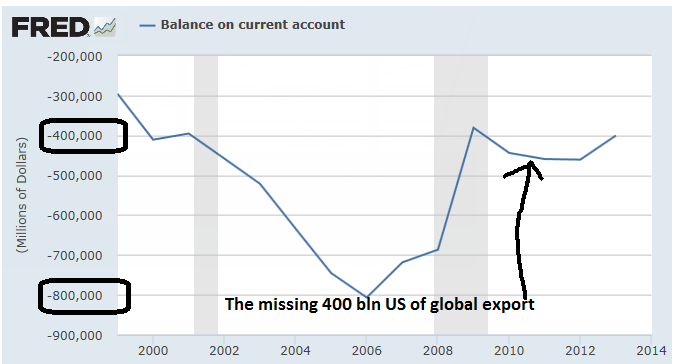

2. US current account deficit reduced by 50% (see chart below)

3. A Europe where Germany will pay the price for the first two factors with a lag of six to nine months.The headline call was and remains that Germany will be close to recession by Q4-2014 or Q1-2015 setting up a desperate ECB and a Europe once again close to zero growth instead of the “escape velocity” everyone and their dog promised you and me in December and January.

This past week we went through the important floor of 1% on ten year German Bund yield and I took profit on my long held position.

A position I established back in Q4-2013. Feeling “naked” I did some additional work and heavily supported by our Saxo JABA model we have changed the asset mix-up and also our yield call:

• Highest conviction call remains for lower global yields (Low in Q1-2015), but for rest of 2014 I see US yields falling more than European equivalent – this will lead to Bunds underperforming Ten year Treasury and set up the second call:

• US Dollar will significantly weaken from mid-Q3 into Q1-2015. Market remains overexposed to US dollar and US equities relative to norm – Furthermore with mid-term election on November 4th the coming budget talks will have a hard time producing convincing and long-term results needed. Bunds will not be able to follow the re-pricing of Fed (away from early 2015 hike) and growth in the US (It’s not the weather) as Q2 gets revised back down to 2.25-2.50% and geo-political risk and lag of global earnings for S&P-500 companies reduces margin and cash-flow. The US average GDP the last five years has been 2.0%……

I am presently almost square in fixed income – alpha model – from very long, but will use a any correction in US bonds to activate medium term long. (Again Bunds yields will continue to fall but less than US rates remains the new call…) hedging any US dollar exposure back into JPY and EUR. EUR/USD could trade 1.4000+ and USDJPY below 97.00.

Global growth is slowing down – World Growth in 2014 was in January expected to be higher than 3.1% – Today my learned colleagues have revised their “guess-estimates” down to 2.53% – a “small” drop of 0.6% – which is not only concerning but also put at risk the coming budget talks – certainly in Europe but also in the US.

This is of course relatively bold calls considering the market and consensus have short EUR/USD, long USDJPY and overweight US stocks as their main risk vehicles when VaR (value at risk) is allocated. It’s important to underline that major US investment houses, and certainly every single sales person I talk to, believe US is about to accelerate in growth not slow-down. Q3 could be ok but the real damage will come in Q4 as the lead-lag factor of geopolitical risk, lack of reforms and excess global supply leads to low inflation and despite Fed recent optimism about an exit strategy the fact remains few institutions is worse than the FED in projections even their simple target goals:

Fed is simply terrible in predicting. Why would they be right this time?

They will not be – Q2 will be revised down to 2.5-ish by third correction – the standard correction is 1.5% from 1st to 3rd reading:

… And largely ignored, the US consumer remains on strike despite “lower” unemployment:

No, hope and lack of alternatives is ruling the markets…..the major call is:

Short US Dollar Index and soon also long commodities as the weak US dollar and soon lower US yield sets up great value trade.

Yes, it’s time to be defensive … very defensive.

Safe travels,

Steen Jakobsen

Short the Dollar?

I think so. Rate hikes are priced in that I do not believe will happen. And if they don’t, it would be dollar negative.

Of course the ECB could go ape with QE, and that would be negative for the euro (thus dollar supportive). On balance, I think Steen has this correct.

Long commodities?

Not so sure. If global growth is slowing why shouldn’t oil, copper, and base metals do poorly?

Yet, I do like gold here. It’s priced as if the Fed will hike and QE will never start again.

Those are likely bad assumptions.

Mike “Mish” Shedlock

http://globaleconomicanalysis.blogspot.com