Steen Jakobsen has some interesting comments on China and Japan in his latest email.

Steen discusses China’s “official” PMI which is different than the Markit PMI on China that I covered earlier (see Weaker China PMI, Especially New Orders and Exports).

Emphasis in italics mine.

Steen Writes …

Greetings,

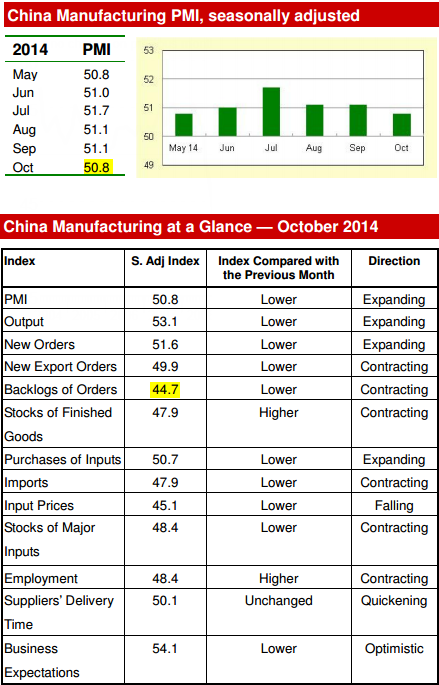

China’s official manufacturing PMI report just came out – and it’s weaker than projected. The print was 50.8 vs. 51.2 expected. Orders backlog looks especially weak.

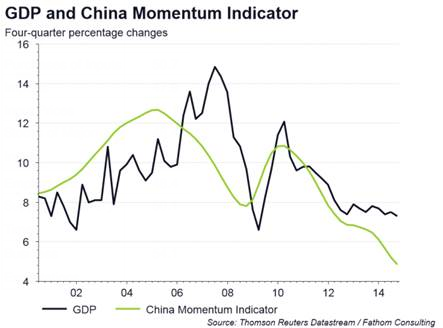

Fathom Consulting in London is calling for China’s growth to slow to 5 percent over next year or so. Not sure I fully agree, but it’s certainly possible.

China Momentum

The world is now reduced to:

Japan QE Infinite (Helicopter money next) – BOJ is buying more than 100% of issuance from Ministry of Finance now! ECB can’t move needle, but can talk… Fed now voicing EUR concerns again (MNI news)…. US house market cooling, shale gas industry bankrupt German/EZ GUARANTEED recession (just updated SENTIX ECO vs. growth showing -2% by Q2 if nothing changes) Disinflaton/deflation trends accelerating to downside w. commodities, energy (which is excellent lead for “anchored” inflation expectations..)

Yes, world should rejoice, take stocks & US dollar higher making sure EM engine is killed totally…. the “surprise” will be that China gets desperate before ECB does, as China clearly has voiced unhappiness with Japan’s policy of devaluations.World only has two engines of growth: EM and US… both are running out of fuel…..US corporates enjoyed 14 years straight years of weaker US dollar – in S&P 500 46% of sales is from overseas, profit has risen 3x faster than sales since 2009, 2y money up considerably in price.

End of financial engineering? Good news is – soon there is NO alternative but for companies to invest – but there are only two things which is certain:

Volatility will rise Government bond prices will continue down (10 Yr US to hit 1.5% – and November is in our models indicating significant lower yield – so be forewarned)

Being the simple man I am – I have only one trading view: Lower yields (since Q4-2013), one economic view: Disinflaton/deflation will be the catalyst for asset sell off as Fantasy-land is replaced by Reality-land. FX view: US dollar will peak in Mid-November……one timing view: LOW in this economic/inflation/Nonsense is Q2-Q3 2015Derivative views of that being: Sharp sell-off in UK housing (and Middle East, Norway, Australia – where lending to mortgages is close to 70% of lending in many banks), Low in inflation expectations by Q1 early (signal buy on Gold and metals)…….

Working on Outrageous Predictions 2015 – input very welcome.

Safe travels,

Steen

Three Key Steen Opinions

- Japan QE Infinite (Helicopter money next) – BOJ is buying more than 100% of issuance from Ministry of Finance now!

- Disinflaton/deflation will be the catalyst for asset sell off as Fantasy-land is replaced by Reality-land.

- China to get desperate before ECB does, as China has voiced unhappiness with Japan’s policy of devaluations.

Mike “Mish” Shedlock

http://globaleconomicanalysis.blogspot.com