Dr. Eric Dor, director of IESEG School of Management, in Lille, has an update on bank exposure to Greek debt liabilities.

The numbers are roughly in line with figures I have posted earlier, but the breakdowns and other details are interesting.

| IESEG | Bilateral loans | Guarantees on the borrowings of EFSF to fund its loans | Implicit share of TARGET2 claims of the Eurosystem | Implicit share in the SMP holdings of bonds by the Eurosystem | Total |

|---|---|---|---|---|---|

| Austria | 1.555 | 4.235 | 1.198 | 0.574 | 7.562 |

| Belgium | 1.942 | 5.291 | 1.512 | 0.725 | 9.470 |

| Cyprus | 0.11 | – | 0.092 | 0.044 | 0.247 |

| Estonia | – | 0.39 | 0.118 | 0.056 | 0.564 |

| Finland | 1.004 | 2.735 | 0.767 | 0.368 | 4.873 |

| France | 11.389 | 31.02 | 8.651 | 4.148 | 55.209 |

| Germany | 15.165 | 41.308 | 10.981 | 5.266 | 72.72 |

| Greece | – | – | – | – | – |

| Ireland | 0.347 | – | 0.708 | 0.340 | 1.395 |

| Italy | 10.008 | 27.259 | 7.511 | 3.602 | 48.380 |

| Latvia | – | – | 0.172 | 0.083 | 0.255 |

| Luxembourg | 0.14 | 0.381 | 0.124 | 0.059 | 0.704 |

| Malta | 0.051 | 0.138 | 0.040 | 0.019 | 0.247 |

| Netherlands | 3.194 | 8.699 | 2.443 | 1.171 | 15.507 |

| Portugal | 1.102 | – | 1.064 | 0.510 | 2.676 |

| Slovakia | – | 1.503 | 0.471 | 0.226 | 2.200 |

| Slovenia | 0.243 | 0.717 | 0.211 | 0.101 | 1.272 |

| Spain | 6.65 | 18.113 | 5.394 | 2.587 | 32.744 |

| Total | 52.9 | 141.8 | 41.709 | 20 | 256.409 |

The above from IESEG School of management on the Exposure of European Countries to Greece

Exposure of European Banks

The exposure of European banks to Greek public and private debt is most interesting.

Nearly all the liabilities have been shifted from banks to the public. For example the exposure of German banks to the Greek public sector is now limited to $181 million.

German Bank Claims on Greek Public Sector

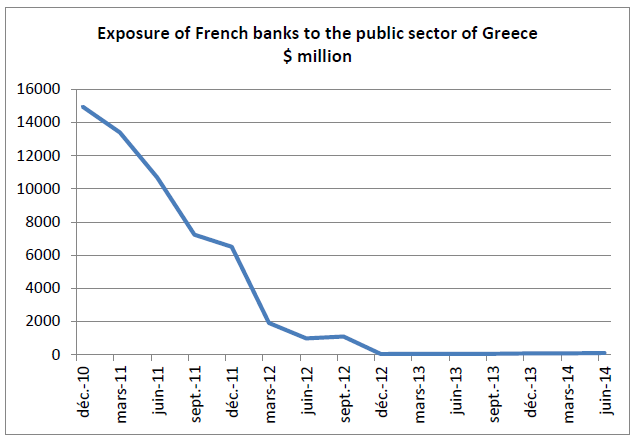

The exposure of French banks to the public sector of Greece is now limited to $102 million.

French Bank Claims on Greek Public Sector

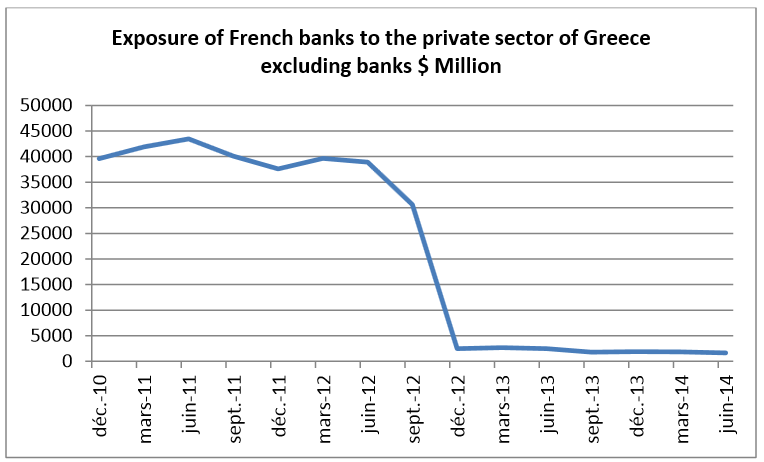

The exposition of European banks to the private sector of Greece excluding banks is also very limited, even if it recently increased for German banks, for which it amounts to $7.885 billion.

The exposure of German banks to Greek banks amounts to $5.702 billion. Their other potential exposure to Greece amounts to $2.912 billion in the form of derivatives, guarantees extended and credit commitments.

German Bank Claims on Greek Private Sector

The exposure of the French banks to the private sector of Greece excluding banks is limited to $1.646 billion.

French and German banks dumped their exposure to Greece on to the public by dumping assets and also via the EFSF.

- German taxpayers are responsible for $41.3 billion via the EFSF, with Target2 liabilities of another $11 billion.

- German taxpayers are responsible for $31 billion via the EFSF, with Target2 liabilities of another $8.7 billion.

Bluff of the Day Revisited

Taxpayers in general, not banks are the ones at risk if Greece defaults. This explains the Bluff of the Day: Germany Warns “Greece is No Longer of Systemic Importance For the Euro”.

It’s pretty clear Greece is still of systemic importance. What Merkel really meant is this: “German banks now have limited concerns if Greece defaults. Instead, it’s German taxpayers who are at risk.”

As Steen Jakobsen chief economist of Saxo Bank in Denmark explains “Euro is Not a Good Idea and ECB About to Make Biggest Mistake in History” .

Steen’s rationale is supported by Michael Pettis at China Financial Markets and Lacy Hunt at Hoisington Management. For details, please see Grand Experiment Failure; Bankers Prefer Bubbles; Europe is not USA; Final Epitaph.

Gold the Place to Be

Today, ECB president Mario Draghi put taxpayers still more at risk with QE policies that cannot possibly work as noted in “QE already Working” Says IMF Lagarde; Ho-Hum Details Announced; Gold the Place to Be.

Mike “Mish” Shedlock

http://globaleconomicanalysis.blogspot.com