Finding value in this market seems impossible.

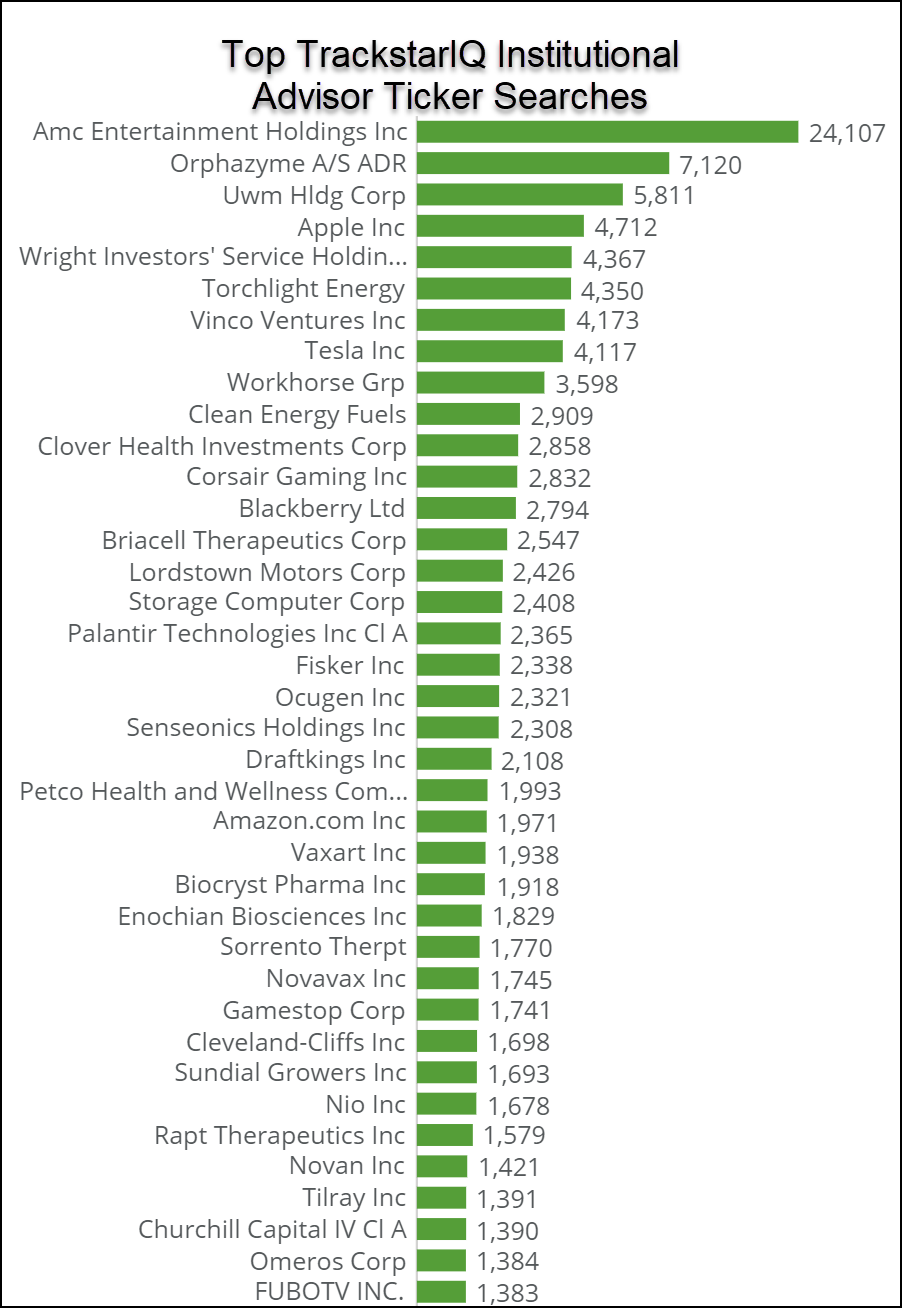

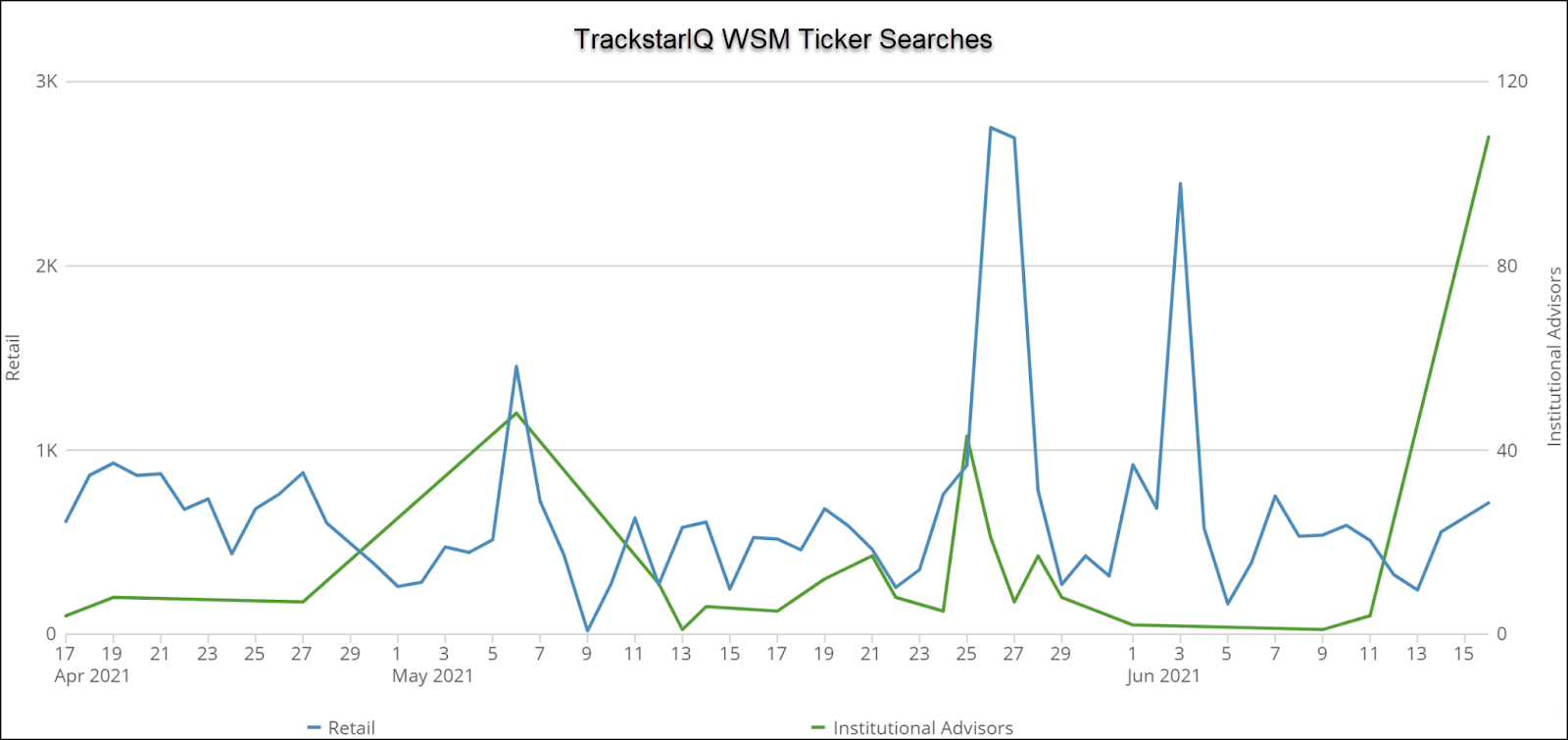

Yet, our TrackstarIQ data might have found a hidden gem.

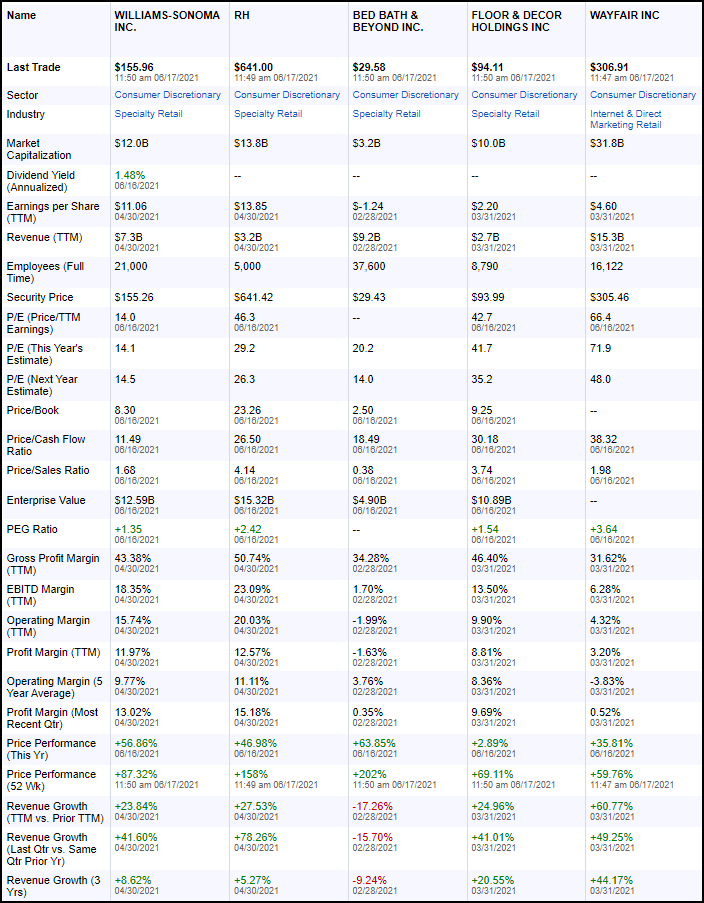

Recent searches amongst institutional advisors highlighted Williams Sonoma (WSM).

At first glance, the company looked fantastic with a price-to-earnings ratio of 14.44x compared to a sector average of 23.08x.

And as shares recently began to sell off, we think there might be a buying opportunity.

Williams Sonoma in a nutshell

Known for their high-end home goods, Williams-Sonoma Inc operates four divisions:

- Pottery Barn (34.8% of revenue) sells premium furniture and accessories

- West Elm (22.3% of revenue) produces personalized products designed by the company’s artists and designers

- Williams-Sonoma (23.5% of revenue) sells cookware, tools, cutlery, electrics, tabletop and bar, outdoor, furniture, and cookbooks through brick and mortar stores as well as online.

- Pottery Barn Kids and Teen (14.8% of revenues) sells products for nurseries, bedrooms, and playspaces.

- Other (4.5% of revenue) consists of international franchise operations.

Started back in 1973, the San Francisco based company saw sales and earnings increase every year but one since 2012.

Their 5-year average growth runs a bit over 6%. A large part of that has been driven by their aggressive push into e-commerce, which accounts for 70% of their sales.

The company carries very little debt and scores incredibly well on many financial health metrics.

The real value

Take a look at the profitability metrics for the company.

There are few companies out there that boast such strong and consistent results across everything from ROA to ROI, not to mention improving margins.

Even the price-to-earnings growth ratio (PEG) sits at 1.35x while the industry comes in at 1.62x.

Put up against its competitors, it destroys them on nearly every metric out there.

So what’s the catch?

For starters, 2/3rds of their merchandise comes from outside the U.S., mainly Asia and Europe.

Given the supply chain issues, that puts enormous pressure on their margins, which we’re already seeing in shipping costs and raw materials. The company already faces massive backorders.

Many analysts also wonder if their best year is behind them. Customers splurging during Covid as they stayed indoors.

Yet, as the number one pure-play digital retailer in home furnishings, it’s tough to think this hurts their ongoing results.

And initiatives underway are expected to more than offset cost increases, allowing the company to further expand margins in the coming year.

Our hot take

A pullback in this stock might be a gift.

The company displays a clear strategy, strong balance sheet, and consistent return for shareholders.

Top-trending tickers, market-moving news alerts: Straight in your inbox!

See the pulse of the market as researched by Wall Street Elites and receive top-trending tickers and other market intelligence to inform your trades.Sign up for Wall Street Connected – our free daily newsletter that leverages our TrackstarIQ Data.

Click here to learn more