Steel is hot.

Like, scorching.

In the past year, we’ve seen the Producer Price Index for steel more than double.

Supply shortages coupled with strong demand have and continue to keep prices elevated.

That’s helped companies like Steel Dynamics (STLD) pad their bottom line.

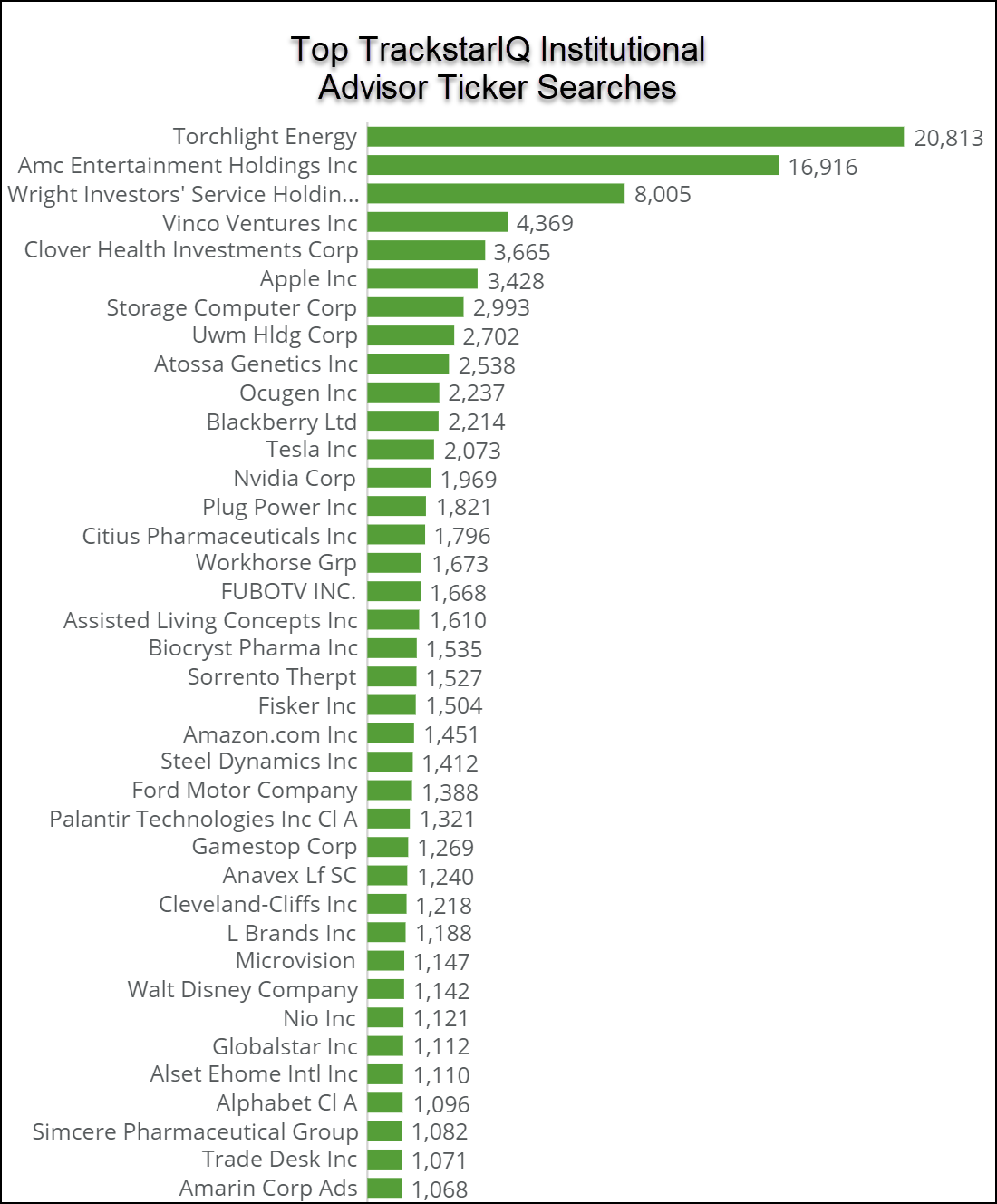

This top search for institutional advisors from our TrackstarIQ data stood out not just because of the company’s size, but its +63% run since the start of the year.

Yet, with a price to earnings ratio (P/E) of 16x, shares look pretty darn cheap.

So is this stock worth a look way up here?

Heavy metal

Based in Fort Wayne, Indiana, Steel Dynamics is one of the largest steel producers and metal recyclers in the U.S, with capacity to make over 11 million tons.

They operate in three key segments:

- Steel operations (74% of revenues with an ~12% operating margin)

- Metal recycling operations (11% of revenues with an ~1.4% operating margin)

- Steel fabrication operations (9% of revenues with an ~13.3% operating margin)

Revenue grew at a healthy 4.8% over the last five years, albeit from a major jump in 2018 due to an acquisition.

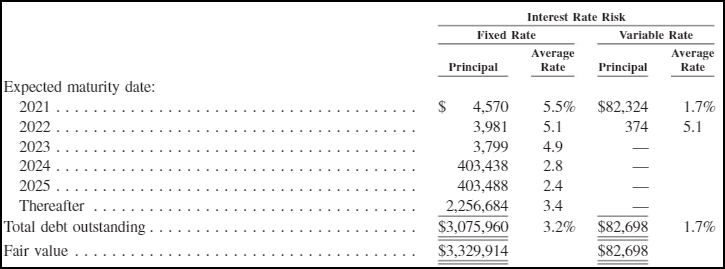

Debt is pretty high with $3 billion on their balance sheet. However, little is due before 2024, with most due well after 2025.

Demand for steel fell globally by 0.2% in 2020. For 2021, The World Steel Association (WSA) expects that to flip to +5.8%.

However, the majority of that is driven by China.

Excluding China, the WSA expects demand in 2022 to fall short of 2019 levels in developed countries.

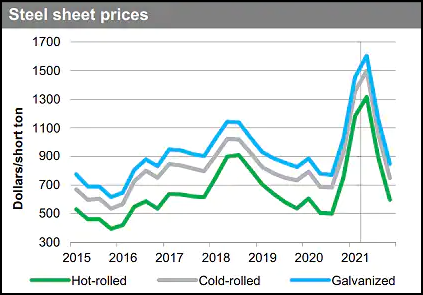

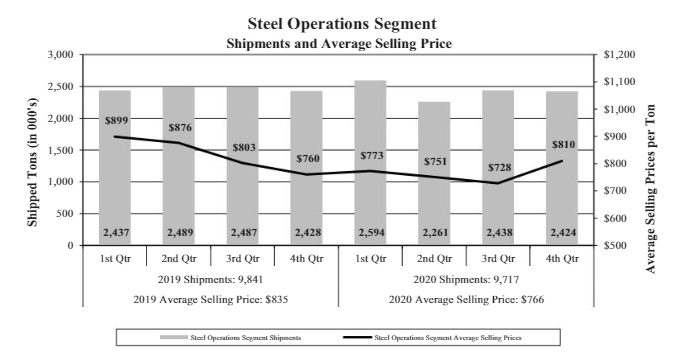

Steel Dynamics saw prices plunge through 2020 on an oversupply hangover. Since then, inventories dropped substantially, helping drive up the cost per ton as average prices increased 35%.

With the infrastructure package waiting in the wings, overall steel demand should remain high in the U.S.

In the last few years, Steel Dynamics invested in increased capacity, acquiring Heartland Steel Processing in 2018 for $400 million as well as building a flat roll steel mill in Sinton, Texas.

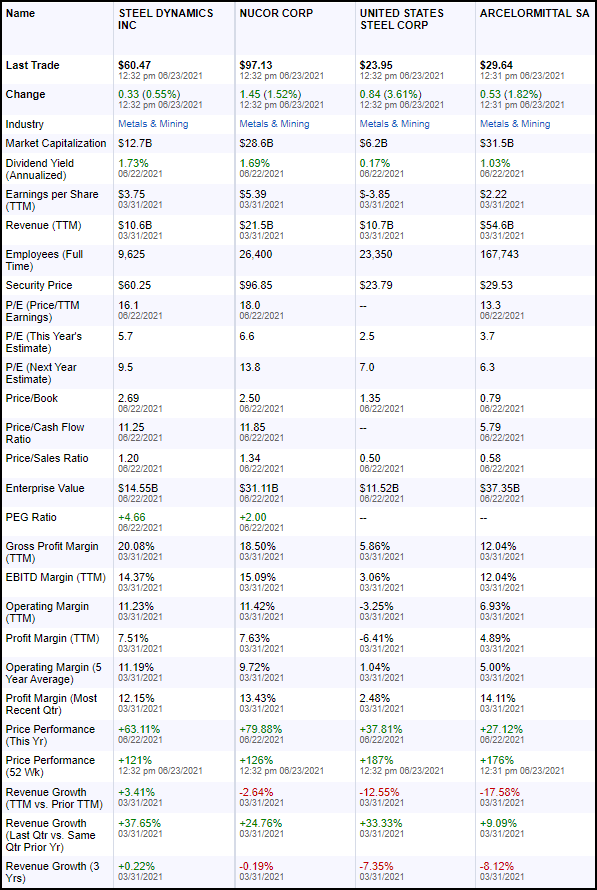

Competitor comparison

In one of our recent articles, we covered Arcelor Mittal, another steel company.

However, we did not use Steel Dynamics as a comparison.

So, let’s see how they look against one another.

Overall, Steel Dynamics performs better across all categories with the exception of current and next year P/E ratios.

However, if we toss U.S. Steel due to its poor margins, the resulting selections between STLD, NUE, and MT give a pretty nice selection of companies.

Our hot take

Of the steel companies listed, Nucor looks better for a few reasons.

First, it wins out in the margins category for the most recent quarters.

Second, it’s a bit cheaper on the price-to-earnings growth (PEG) ratio.

Third, and probably most importantly, they have a better balance sheet.

You’ll notice that Nucor has a better liquidity position with less debt relative to its peers, with the exception of Arcelor Mittal.

The slightly better 1.72% dividend yield isn’t too shabby either.

Top-trending tickers, market-moving news alerts: Straight in your inbox!

See the pulse of the market as researched by Wall Street Elites and receive top-trending tickers and other market intelligence to inform your trades.Sign up for Wall Street Connected – our free daily newsletter that leverages our TrackstarIQ Data.

Click here to learn more