There are a lot of odd things to invest in these days.

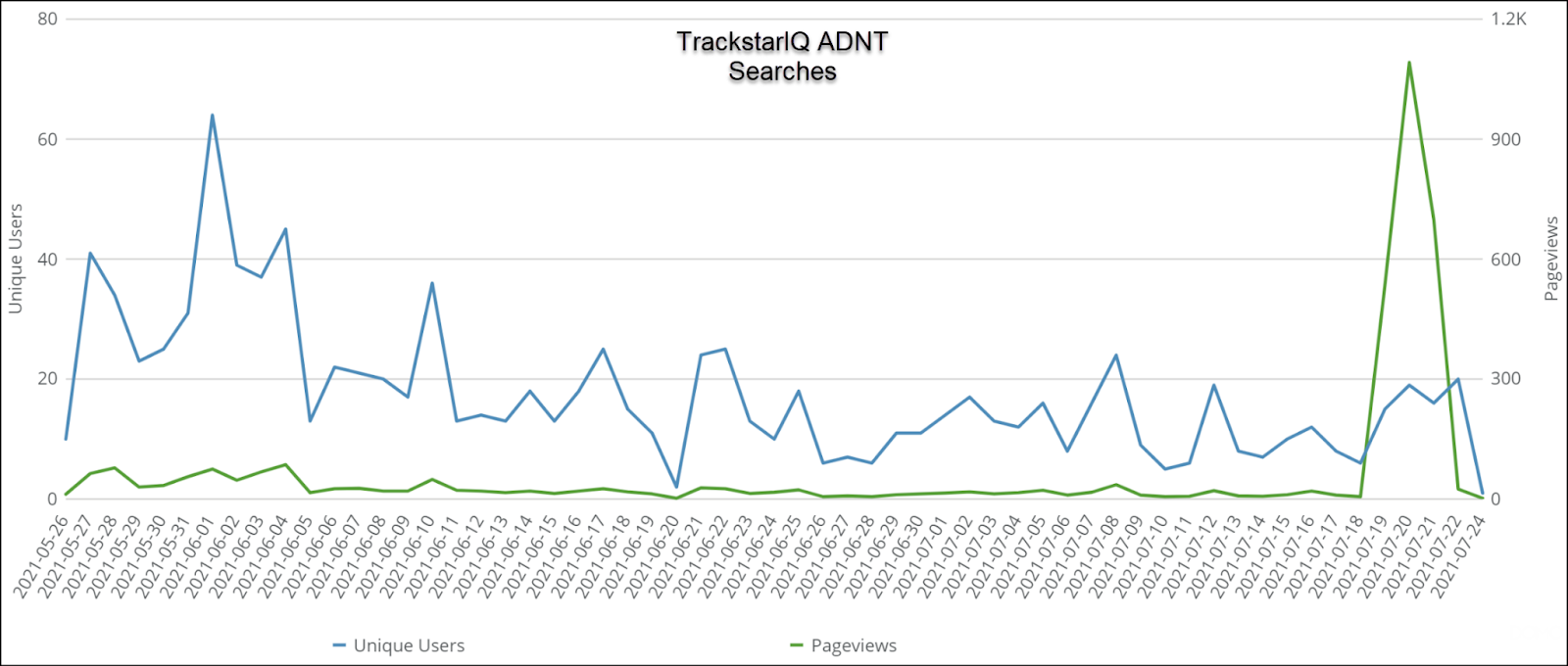

But it took us by surprise when car seats topped our TrackstarIQ data.

Specifically, the number of searches for Adient PLC (ADNT) spiked last week out of the blue.

Earnings aren’t until August 5th and there was no major news surrounding the company.

So we decided to dig in a little and see if big money knew something we didn’t.

The life and times of Adient

One of the world’s largest automotive seating suppliers, Adient PLC was born out of Johnson Controls’ (JCI) separation of its automotive seating and interiors business.

Adient designs, manufactures, and markets seating systems and components for retail and commercial vehicles as well as motorsports.

The company is a major original equipment manufacturer (OEM) for seating. Essentially, they provide the seats to a company like Ford (F) who then drops them into a car, and sells it under Ford’s brand.

And this is a massive company.

We’re talking 85,000 employees worldwide, 238 manufacturing or assembly facilities, and operations in 38 countries, with their main headquarters in Dublin, Ireland.

Since they produce a limited range of products, the company reports through three geographic segments:

- Americas – 49.9% of revenues

- Europe, Middle East, and Africa – 38.8% of revenues

- Asia – 12.7% of revenues

Asia represents their largest growth segment, hitting 32.4% in the latest quarter vs. the same time last year compared to less than 1% in the U.S. and 10% in Europe.

Not a lot of profits

On an annual basis, ADNT hasn’t generated positive earnings since 2017.

However, they did manage to do it the last two quarters.

If you added those together and assumed similar performance in the back half, the current price to earnings ratio (P/E) would stand at 8.62x – extremely cheap by market standards.

However, the company and analysis expect the second half to perform worse.

Looking forward, the company trades at 13.1x their 2021 EPS forecasts and 8.5x their 2022 forecast.

What’s causing the shortfall in 2H?

Same thing as other automotive companies – semiconductor shortages.

With fewer cars manufactured, fewer seats are needed.

The biggest drawback is the balance sheet.

Right now, ADNT has $3.6 billion in debt compared to $984 million in cash.

To shore up its balance sheet, ADNT is exiting a joint venture in China that’s expected to raise $1.4 billion in 2021. That money will help pay down the remainder of ADNT’s 7% debt notes.

By the end of the year, the company hopes to reduce net leverage, which stood at 3.89x in 2020, down to 1.5x-2.0x.

Our hot take

ADNT is a cheap company for a reason.

Their growth is lackluster and their vision is aimless.

They don’t offer a dividend and carry a heavy amount of debt.

Frankly, there isn’t much reason to jump the gun on this stock before they show they can execute on their short-term strategy.

Top-trending tickers, market-moving news alerts: Straight in your inbox!

See the pulse of the market as researched by Wall Street Elites and receive top-trending tickers and other market intelligence to inform your trades.Sign up for Wall Street Connected – our free daily newsletter that leverages our TrackstarIQ Data.

Click here to learn more