Gizzards have never looked so good.

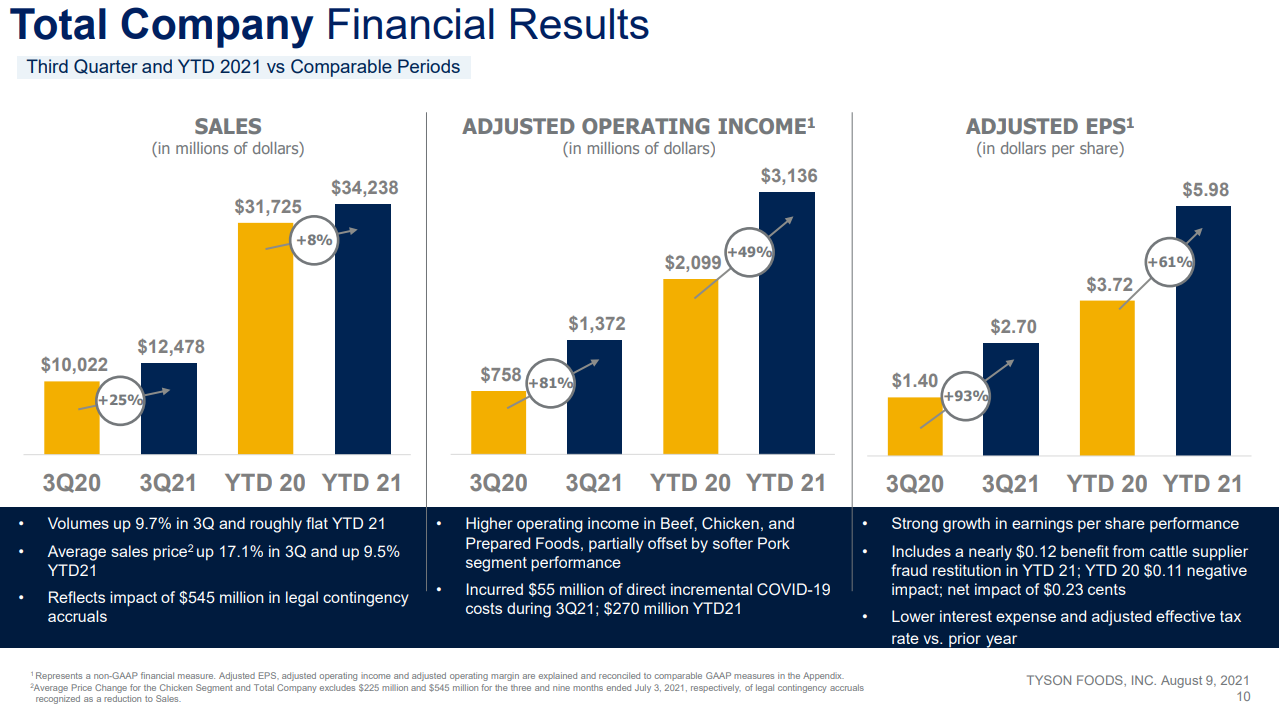

Tyson Foods (TSN) reported quarterly results Monday.

The market’s reaction…

Giddy is an understatement.

Earnings smoked estimates by more than 60% sending shares up 8.69% the following day.

And everyone was watching.

But guess what?

There’s still a ton of value here!

Even after a serious run of more than 10%, the long-run outlook is stellar, despite vegetarians and Corey Booker vegans.

More than chicken

Tyson’s business isn’t hard to understand.

They produce, market, and distribute chicken, beef, and pork as well as prepared foods.

Here’s a quick breakdown of their revenue streams:

- Chicken – 30.6% of revenue

- Beef – 36.5% of revenue

- Pork – 12% of revenue

- Prepared Foods – 19.8% of revenue

- International/Other – 4% of revenue

Growth isn’t massive in this industry.

Over a 3-Year period, their revenue growth runs around 4%.

That’s what makes their 3rd quarter results so impressive.

While sales and operating income improved, operating margins actually shrank from 11.11% last year to 8.51% this year.

However, that’s an improvement from 7.2% last quarter.

What drove this impressive growth?

Beef…lots of beef.

Pork did add a healthy amount of sales as well. But it was half of what Beef did.

An important point from this slide – exports were up $500 million year-to-date despite all the trade spats.

Most of that came in the most recent quarter.

China’s been a major importer of meats since they were forced to cull huge amounts of pig farms due to an outbreak.

Being one of the top pork consumers in the world, they leaned on U.S. exporters like Tyson to fill the demand.

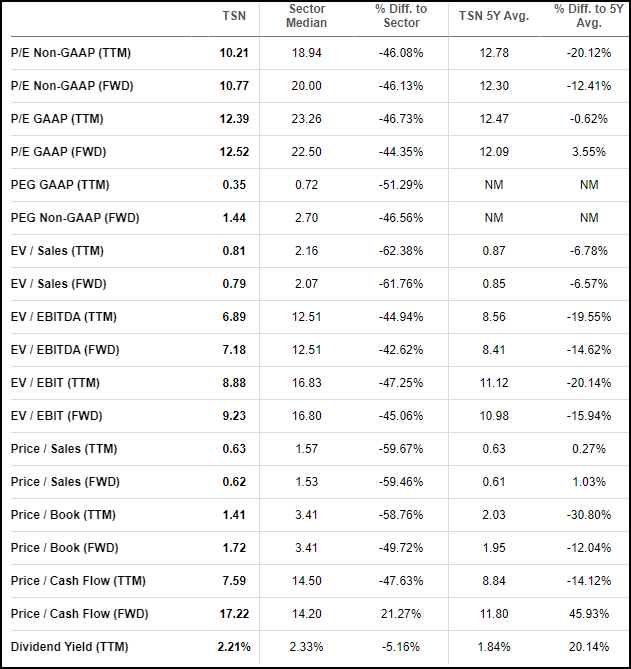

Lots of lovely value

Tyson is dirt cheap by nearly any valuation metric.

Take a look:

The meat mammoth has a trailing and forward P/E ratio of 12.

Put bluntly, it will take Tyson 12 years to earn its entire market cap.

For context, the S&P 500 during its best years runs around 15x-18x.

Right now it’s at 34x.

None of its peers, Hormel (HRL) Kellogg (K), or General Mills (GIS) come anywhere close to this cheap.

But let’s make this even easier.

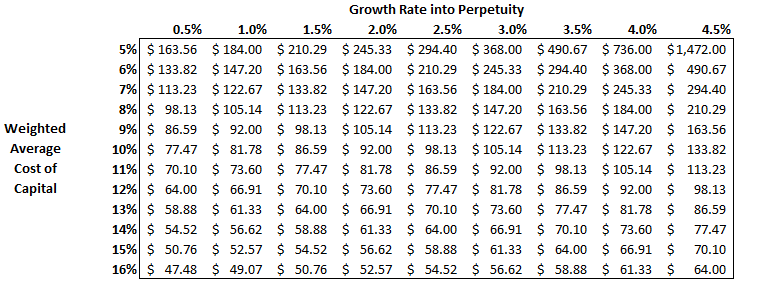

The free cash flow per share runs stands at $7.36.

Using a discounted cash flow model, we modeled what different growth rates into perpetuity would look like against different discount rates (weighted average cost of capital).

What you’ll notice is that the current share price of $80 can still mean a lot of upside potential.

Our hot take

This isn’t a stock that’s going to triple in value in the next year.

What we have is a good ‘ol fashioned value play that even Benjamin Graham (Warren Buffett’s teacher) would love.