Salesforce.com (CRM) is a massive company that just keeps growing.

Let us give you some perspective.

In 2012, Salesforce posted annual revenues of $2.2 billion.

This year, they hit $22.35 billion.

Their average annual growth consistently runs over 25%.

But what caught our attention was a surge in interest amongst institutional players.

This crowd searched for CRM 1392% more in the last two days than the previous five and 489% more in the last week compared to the one before.

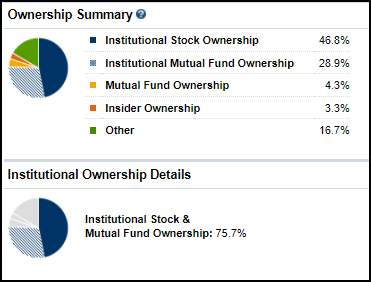

That’s pretty interesting for a stock that already has a massive amount of institutional ownership.

We decided to take a look into the stock to see what all the fuss was about.

What we found may surprise you.

CRM in a nutshell

Salesforce.com has been around since 1999. Their HQ in San Francisco is ridiculous if you’ve never seen it.

The company is the leading provider of on-demand customer relationship management (CRM) software.

If you’ve never dealt with this type of platform, it enables organizations to manage the sales, marketing, and service operations within one integrated package.

Salesforce.com expanded their offerings to include everything from data analytics to acquiring business communications tool Slack.

By market share, they own 20% of the global pie with SAP in second at just 8%.

90% of Fortune 100 companies use at least one of Salesforce’s products.

Revenues come from two main streams: subscription and support, which accounts for 94% of their revenue, and professional services and other.

What makes Salesforce particularly well positioned is its on-demand Software-as-a-Service (SaaS) cloud-based platform.

Traditionally, you had to install software throughout a business, possibly setting up servers and infrastructure.

Cloud-based technology allows businesses to scale quickly by accessing the software online. This allows businesses from small companies to giant conglomerates to pick and choose what works for them.

Recent performance

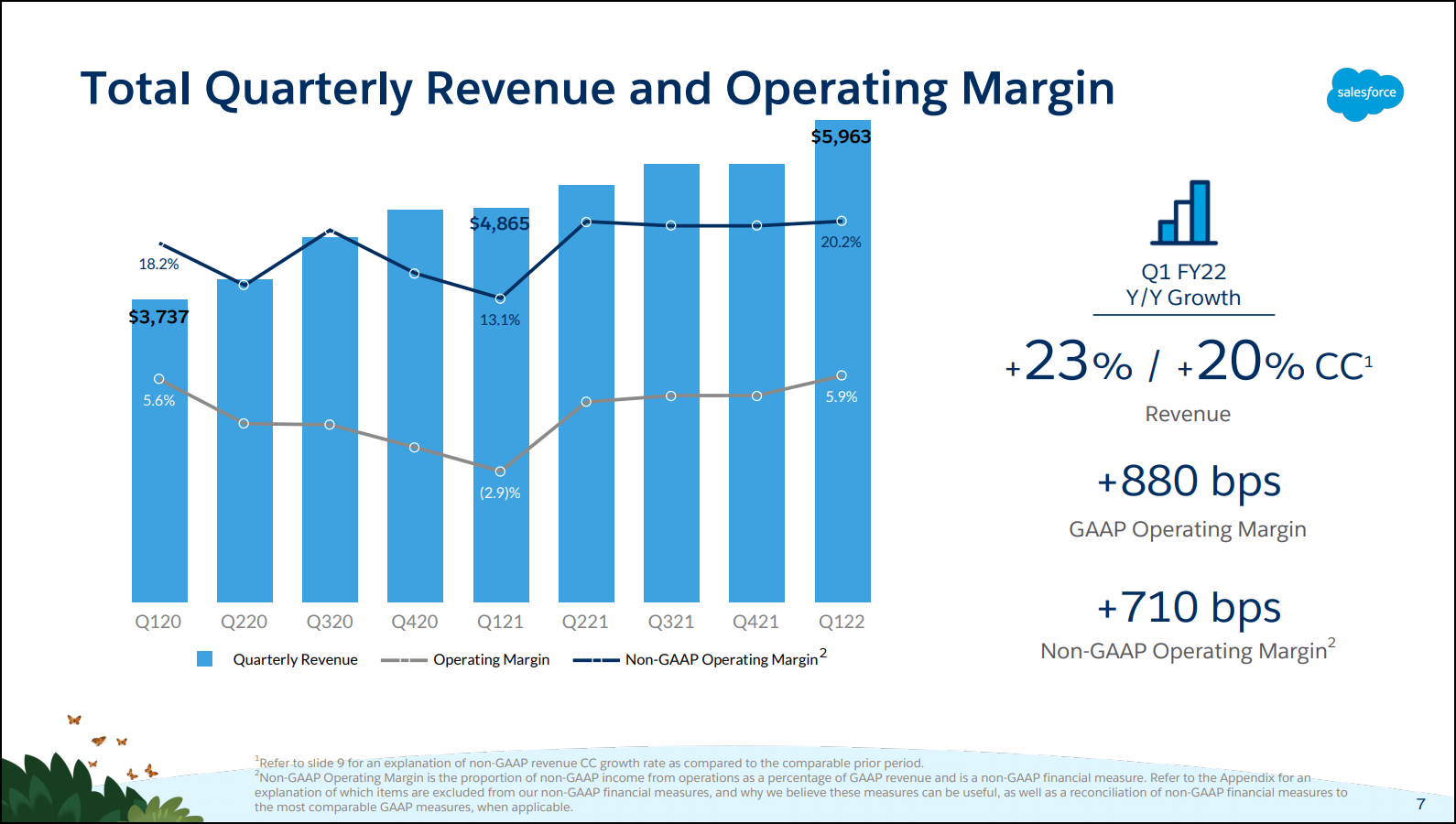

Last quarter (Q1 of FY22) saw Salesforce continue powerful growth.

Growth did stall in the two quarters prior. However, they more than made up for it in the latest quarter.

Impressively, they pushed operating margin over 20% and kept it there for the last four quarters.

The company also boosted its balance shee,t growing cash on hand by 53% year-over-year (YOY).

Where we find pause

Salesforce is an expensive stock.

At $250, it trades at a price-to-earnings ratio of 44x non-GAAP and 63x forward non-GAAP.

Part of the lower future earnings is due to the acquisition of Slack which will hit their Q2 earnings coming up.

What we can do is consider what a discounted cash flow (DCF) model might suggest based on cash flows.

Right now, cash is growing at a ridiculous clip of 22.3% per year on average.

Salesforce believes they can hit $50 billion by 2026, or around 17.5% annually.

Free cash flow runs at around 6% of revenues.

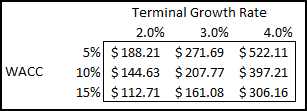

So let’s see what the value of their 17.5% growth on their free cash flow might look like if:

- We change the discount rate (WACC) – higher rates lower the value of future cash flows and the calculated share price

- Different terminal rates at the end of five years – You can assume a company grows into perpetuity or simply stops at a point in time. We modeled a perpetual growth at 2%-4%.

With shares currently trading at $250, we could say that a terminal growth rate of 3% would support the current share price if we use a discount rate of 5%.

The key point with this formula to understand is the impact the terminal value has on share price calculation.

To give you an idea, the top left calculated share price of $188.21 would drop to $21.26 without that terminal value calculation.

Our hot take

A lot of growth is built into Salesforce’s share price.

But, they have a history of meeting those expectations.

There is no reason to believe they won’t hit serious growth for the foreseeable future.

A lot of it just comes down to the assumptions you make on growth and discount rates.

Top-trending tickers, market-moving news alerts: Straight in your inbox!

See the pulse of the market as researched by Wall Street Elites and receive top-trending tickers and other market intelligence to inform your trades.Sign up for Wall Street Connected – our free daily newsletter that leverages our TrackstarIQ Data.